… When One Mortgage Can Do the Work of Five:

Debt consolidation isn’t about fixing a mistake—it’s about fixing structure. For many Canadians, debt builds quietly: a credit card used during a tight year, a car loan layered on top, maybe a line of credit that never quite comes back down. Eventually, the real strain shows up in cash flow, stress, and affordability—not because someone was reckless, but because the cost of carrying debt got louder than their income.

Switching lenders mid-term to consolidate debt is one of the most misunderstood strategies in Canadian mortgage planning. People hear “penalty” and stop thinking. But penalties are just one variable in a much bigger equation that includes lender policy, credit realities, urgency, and timing. In many cases, switching lenders mid-term isn’t the flashy option—it’s the necessary one.

This article walks you through why.

Topics Covered in This Guide

Why is debt consolidation increasing?

How to consolidate your debt by switching lenders mid-term

Why you might switch lenders mid-term instead of using other consolidation strategies

When should you consolidate debt through switching lenders mid-term

Why does switching lenders mid-term require you to break your mortgage?

What are the limits of consolidating debt through switching lenders mid-term?

How credit rating influences the decision to switch lenders mid-term

Using the Debt Consolidation Calculator to consolidate debt

What is debt consolidation

Debt consolidation is the process of replacing multiple debts with a single, more efficient structure. Instead of juggling credit cards, personal loans, car loans, and lines of credit—each with its own interest rate and minimum payment—you combine them into one obligation.

When done through a mortgage, unsecured debts are replaced with secured mortgage debt, which typically carries a lower interest rate and a clearer repayment structure. The goal isn’t just simplicity. It’s reducing interest drag and stabilizing cash flow.

Why is debt consolidation increasing?

Debt consolidation is increasing because the financial environment has changed.

Cost-of-living increases outpaced income growth. Interest rates exposed just how expensive unsecured debt really is. And many Canadians built equity in their homes—but not liquidity in their bank accounts.

People aren’t consolidating because they failed. They’re consolidating because the math stopped working.

How to consolidate your debt by switching lenders mid-term

Switching lenders mid-term means moving your mortgage to a new lender before your current term ends and increasing the mortgage amount to include other debts.

In practice, it looks like this:

First, equity is assessed to determine how much can be accessed based on value and lender limits.

Second, unsecured debts are identified and totaled.

Third, a new lender pays out the existing mortgage and advances a larger one that includes those debts.

Fourth, unsecured balances are cleared, leaving one structured mortgage payment instead of many high-interest obligations.

The appeal isn’t just a lower rate—it’s regaining control of cash flow.

Why you might switch lenders mid-term instead of using other consolidation strategies

This is the real decision point—and it’s where many Canadians get stuck.

Why not just refinance with your current lender?

Often, people try—and are told no.

Your current lender may refuse to:

- Increase the mortgage balance enough to consolidate all debts

- Refinance mid-term at all

- Reset amortization to make payments workable

- Combine equity take-out with debt consolidation

This usually isn’t personal. It’s policy. From the lender’s perspective, they already have a performing loan. Allowing a mid-term refinance can increase risk and reduce expected interest income. So they say:

“Wait until renewal.”

“We’ll only offer a HELOC.”

“We’ll approve less than you need.”

That’s often where switching lenders becomes necessary.

Why not just wait until renewal?

Waiting only works if the unsecured debt isn’t actively doing damage. But high-interest debt compounds quickly. In many cases, the interest paid over the next year exceeds the mortgage penalty to exit early. Waiting can be more expensive than acting.

Why not add a HELOC?

HELOCs are flexible, but they:

- Often carry higher rates than first mortgages

- Are usually interest-only

- Require discipline many households don’t realistically have during financial stress

If the goal is elimination—not rearrangement—a HELOC may delay the problem rather than solve it.

Why not add a second mortgage?

Second mortgages can work, but they:

- Carry higher rates

- Add complexity and risk

- Create an additional payment instead of simplification

Switching lenders mid-term collapses everything into one payment, one lender, one strategy.

Why not use private lending?

Private lending is a restructuring tool, not a destination. It’s expensive and short-term. If a prime or near-prime lender will consolidate the debt—even with a penalty—it’s often the lower-risk long-term move.

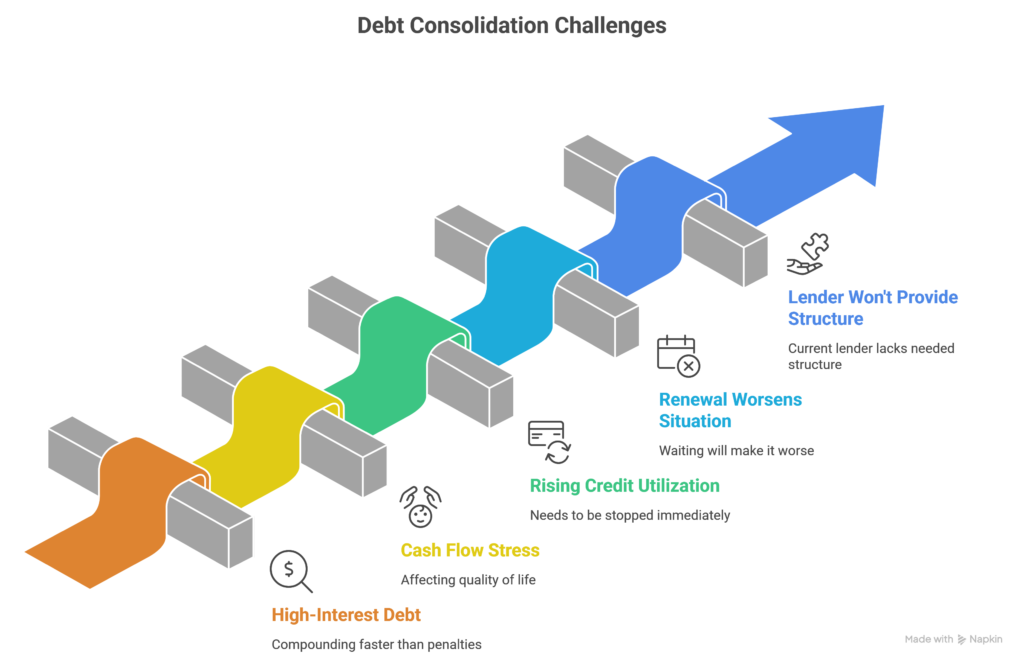

When should you consolidate debt through switching lenders mid-term

This strategy tends to make sense when:

- High-interest debt is compounding faster than penalties

- Cash flow stress is affecting quality of life

- Credit utilization is rising and needs to be stopped

- Waiting until renewal would worsen the situation

- Your current lender won’t provide the structure you need

It’s less effective when penalties are excessive or when consolidation simply stretches debt without improving affordability.

Why does switching lenders mid-term require you to break your mortgage?

A mortgage is a contract. Switching lenders before the term ends changes its core terms—lender, balance, and structure. Your original lender priced the mortgage assuming you’d keep it for the full term. Leaving early usually triggers a mortgage penalty to compensate for lost interest.

The penalty isn’t a punishment. It’s a pricing mechanism. And like any cost, it needs to be weighed against the benefit of fixing the underlying problem.

What are the limits of consolidating debt through switching lenders mid-term?

Most traditional lenders cap refinances and switches at 80% of the home’s value. Income stability, credit profile, and property type also matter.

There’s also a behavioural limit. Consolidation works only if it’s paired with discipline. Eliminating debt without changing habits simply creates room for it to return.

How credit rating influences the decision to switch lenders mid-term

This is one of the most under-discussed reasons switching lenders mid-term becomes necessary.

Debt stress often shows up in credit before it shows up anywhere else:

- Credit cards creep toward their limits

- Utilization ratios rise above 70–80%

- Minimum payments increase

- One late payment sneaks in

Even with strong income, credit scores soften. And banks often underwrite refinances more conservatively than purchases.

Your current lender may say no because:

- Scores dipped below internal thresholds

- Revolving balances are maxed

- Debt ratios look stretched

Another lender may look at the same file and see something different: a borrower whose credit stress is caused by structure, not behaviour—and who will improve immediately once high-interest debt is eliminated.

Ironically, HELOCs are often least available when credit is most stressed, which makes switching lenders into a structured mortgage the only way to actually fix the problem.

Done properly, consolidation often helps credit recover by:

- Paying revolving balances to zero

- Reducing utilization ratios

- Simplifying payment management

- Preventing missed payments

In many cases, switching lenders mid-term is credit-protective, not credit-destructive.

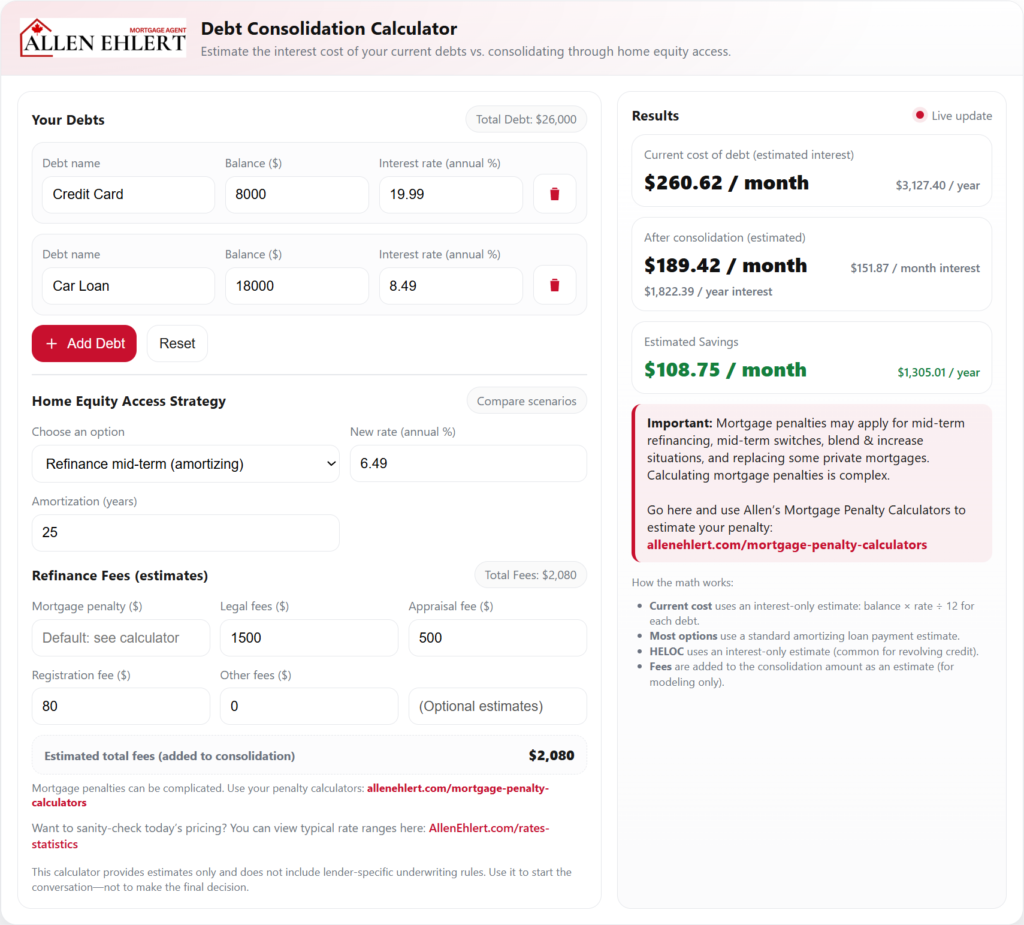

Using the Debt Consolidation Calculator to consolidate debt

This is where clarity replaces guesswork.

The Debt Consolidation Calculator allows you to:

- Model a mid-term lender switch

- Include penalties and all relevant fees

- Compare current interest cost vs. post-consolidation cost

- See clearly whether the move creates savings or extra cost

It doesn’t tell you what to do. It shows you what happens if you do—and what happens if you don’t.

A real-world story: why switching mid-term was the right move

I once worked with a homeowner carrying multiple high-interest balances. His lender refused a refinance and offered only a HELOC. Credit utilization kept rising, and stress followed.

Switching lenders mid-term meant paying a penalty—but it also meant eliminating the revolving debt entirely, restoring cash flow, and stopping the credit slide. The math wasn’t perfect, but the outcome was stabilizing.

Same house. Same borrower. Better structure.

How realtors and clients can put this into practice

Realtors can use this strategy to:

- Help buyers clean up debt before purchasing

- Improve affordability before upsizing

- Prevent failed financing conditions

Clients can use it to:

- Reduce financial stress

- Simplify their financial life

- Make proactive decisions instead of reactive ones

Allen’s Final Thoughts

Switching lenders mid-term to consolidate debt isn’t about chasing a rate. It’s about accessing a refinancing strategy your current lender may not be willing—or able—to offer, at a moment when waiting makes things worse.

Penalties don’t make the strategy wrong. Ignoring credit, policy, and timing does.

As a mortgage agent, my role is to look across lenders, understand your credit story, model the trade-offs properly, and help you decide whether switching mid-term actually improves your affordability and stability. The calculator frames the decision. I help you execute it—or avoid it—confidently and correctly.

That’s real mortgage advice.