The History of Credit Cards: From Retail Tabs to Digital Wallets

Credit is not new. Long before banks, apps, and plastic cards, merchants extended credit to trusted customers based on personal relationships. But the story of how that informal trust evolved into the modern credit card system is a fascinating journey through innovation, regulation, technology—and, of course, trust.

Credit cards are everywhere today—from your digital wallet to your monthly reward points balance—but their origins tell a much broader story about trust, technology, and the evolution of consumer finance. Before plastic cards and payment networks became household staples, credit itself was a deeply personal agreement, often scribbled into a ledger at the local general store.

I’ll try to explain how that simple idea of “buy now, pay later” evolved over centuries—from the earliest forms of retail credit to the emergence of giants like VISA—and how credit cards now impact not just our daily purchases but major financial milestones like qualifying for a mortgage. Understanding this evolution gives us deeper insight into how we use credit today and where it might take us tomorrow.

Early Retail Credit: The Birth of the “Tab”

The First Charge Cards: The Diners Club Revolution

BankAmericard and the Birth of VISA

Credit Cards Today: More Than Just Plastic

Credit Cards and Mortgages: The Double-Edged Sword

Credit Cards and Debt Servicing Ratios

Credit Cards and Credit Building

Early Retail Credit: The Birth of the “Tab”

The roots of consumer credit can be traced to ancient times. In Mesopotamia, clay tablets were used to track loans of grain or silver. But fast forward to the late 19th and early 20th centuries in North America, and you’ll find the first seeds of modern consumer credit taking shape in the form of retail credit accounts.

General stores, department stores, and oil companies began issuing credit tokens, metal coins or celluloid cards to loyal customers. These tokens weren’t accepted anywhere else—they were store-specific, functioning much like private currency. The trust was local. The tab you kept at your neighbourhood store was a reflection of your character, not your credit score.

The First Charge Cards: The Diners Club Revolution

The post-war boom of the 1950s brought more than just economic prosperity—it brought mobility, consumerism, and the birth of the modern credit card.

In 1950, Diners Club introduced the first general-purpose charge card in the United States. The origin story is legendary: co-founder Frank McNamara forgot his wallet during a business lunch in New York. Embarrassed, he vowed never to face that situation again. The solution? A card that could be used across multiple restaurants.

The Diners Club card was not a credit card in today’s sense—it was a charge card. You had to pay the full balance at the end of the month. But the concept—universal acceptability, portable payment, deferred billing—had taken root.

BankAmericard and the Birth of VISA

While Diners Club pioneered the multi-merchant model, it was Bank of America that introduced revolving credit to the mainstream.

In 1958, Bank of America launched BankAmericard, a product that allowed customers to carry a balance from month to month. The original rollout was in Fresno, California, with 60,000 unsolicited cards mailed to local residents—a marketing tactic unheard of at the time.

The response was overwhelming—sometimes disastrously so, as fraud and non-payment plagued early adopters. But the concept proved viable. Soon, other banks wanted in.

To facilitate national and international use, BankAmericard evolved into a network. In 1970, it was spun off into a consortium of issuing banks. In 1976, the brand was officially renamed VISA—a name chosen to be easily recognizable and pronounceable in any language.

VISA Goes Public

For decades, VISA operated as a membership-owned association of banks, facilitating payments without itself issuing cards. But as financial markets evolved and competition intensified, VISA undertook a massive structural transformation.

In 2008, VISA Inc. went public, raising nearly $18 billion in what was then one of the largest IPOs in American history. This transition marked a new era: VISA was no longer just a back-end network for banks. It became a global payments technology company, with revenue driven not from interest rates or late fees but from transaction processing and network services.

Is VISA an Acronym for Something?

VISA is not actually an acronym.

When BankAmericard was looking to go global in the mid-1970s, the name “BankAmericard” posed a problem. It was too closely tied to one bank—Bank of America—and sounded too American for a product aiming to reach international markets.

In 1976, the decision was made to rebrand. The name VISA was chosen because:

- It was short, memorable, and easy to pronounce in multiple languages.

- It evoked the idea of global travel—like a travel “visa” in a passport—suggesting worldwide acceptance and mobility.

- It carried no specific cultural or linguistic baggage, making it ideal for branding across different countries.

Although many people assume “VISA” must stand for something (e.g., Virtual International Service Association or similar), those are just backronyms—made-up explanations after the fact. The truth is that VISA was chosen purely for their international appeal and marketability.

So, while it looks like an acronym, it’s really just one of the most successful brand names ever created in the financial world.

Credit Cards Today: More Than Just Plastic

Today, credit cards are ubiquitous. In Canada alone, there are over 76 million credit cards in circulation—more than two per adult. Worldwide, credit cards underpin trillions of dollars in annual spending, supported by complex fraud detection systems, tokenized security, and AI-powered analytics.

Key features of modern credit cards include:

- Rewards programs: Points, cash back, travel miles

- Digital wallets: Apple Pay, Google Wallet, and other NFC solutions

- Buy now, Pay Later (BNPL) alternatives, reshaping short-term lending

- Real-time alerts and virtual cards for fraud protection

- Access to credit scores, budgeting tools, and financial education

Credit cards have also become a gateway to financial inclusion in many countries, helping individuals build credit histories and gain access to other financial services.

What Comes Next?

The future of credit cards lies at the intersection of technology, transparency, and trust. Here’s where we may be headed:

- Biometric authentication: Fingerprints and facial recognition replacing PINs

- Decentralized finance (DeFi): Credit models built on blockchain technology

- AI-driven underwriting: Personalizing credit limits and interest rates in real time

- Sustainability-linked cards: Tied to carbon tracking or ESG spending profiles

- Reduced physical presence: Cards themselves may become obsolete, with virtual wallets and wearables taking over

Perhaps most importantly, the philosophy of credit is shifting. Once seen as a tool of consumerism and debt, the modern credit card is increasingly a platform for personal finance management, smart rewards, and security.

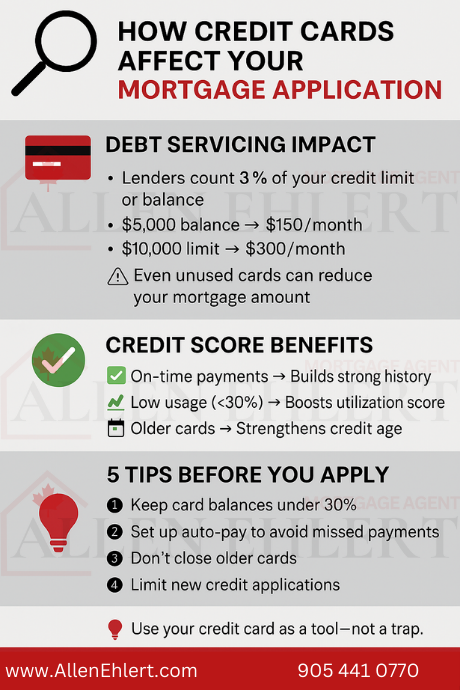

Credit Cards and Mortgages: The Double-Edged Sword

For most Canadians, a mortgage is the largest financial commitment they’ll ever make. Whether you’re a first-time buyer or a seasoned investor, your mortgage application will be scrutinized through the lens of creditworthiness and affordability. Credit cards, surprisingly simple as they may seem, play a pivotal role in that analysis.

Credit Cards and Debt Servicing Ratios

When applying for a mortgage, lenders evaluate how much of your income is being used to service debt. This is expressed through two primary metrics:

- Gross Debt Service (GDS) Ratio: Housing costs (mortgage payment, property taxes, heating, and half of condo fees) relative to income.

- Total Debt Service (TDS) Ratio: GDS plus all other debt obligations, including car loans, student loans—and yes, credit cards.

Where things get interesting

Lenders don’t just look at what you owe on a credit card. Instead, they assess your potential obligation based on your credit limit.

Standard practice: Lenders calculate a monthly liability of 3% of the outstanding balance on a credit card, or 3% of the credit limit if you’re carrying a high balance or only making minimum payments.

Example:

If you have a credit card with a $10,000 limit and a $5,000 balance, lenders might count $150 (3% of $5,000) toward your monthly debt servicing. If you owe nothing but the limit is high, they may still count $300 (3% of $10,000) as a monthly obligation.

Why it matters

That phantom monthly expense can squeeze your TDS ratio and reduce how much mortgage you qualify for—even if you’re not actively using the card.

Credit Cards and Credit Building

On the other hand, responsible use of credit cards can significantly strengthen a mortgage application by boosting your credit score.

A strong credit score:

- Opens access to the best mortgage rates

- Reduces risk perception for the lender

- May allow you to qualify with lower down payments, especially with insured mortgages

Key factors credit cards influence in your credit score:

- Payment history (largest factor): Paying your credit card bill on time, every time, is vital.

- Credit utilization: Using only a small portion of your credit limit (ideally <30%) shows good financial management.

- Length of credit history: Keeping a card open for years helps build stability.

- Credit mix: Having different types of credit (credit cards, loans, lines of credit) reflects well.

In short, a well-managed credit card helps prove you’re mortgage-ready.

The Balancing Act

It’s important to strike the right balance. Here’s what mortgage professionals often advise:

- Keep your utilization low (under 30%, even better if under 10%)

- Pay on time—every time. Set up auto-pay if needed.

- Avoid excessive limits unless you’re very disciplined

- Do not cancel old cards before applying for a mortgage—it can reduce your credit history and hurt your score

- Disclose all credit products during pre-approval. Transparency prevents surprises during underwriting.

Credit cards, when used responsibly, are not enemies of homeownership—they’re allies. They’re a record of trust, a measure of discipline, and a signal to lenders that you can handle long-term financial obligations.

From a debt-servicing perspective, they need to be managed wisely. But from a credit-building standpoint, they’re one of the most accessible and powerful tools available to Canadians preparing to enter the housing market.

So whether you’re guiding a client or reviewing your own finances, treat your credit card not as a convenience but as a strategic lever in your overall mortgage readiness plan.

Summary

From hand-written tabs in corner stores to smart chips, digital wallets, and algorithm-driven credit decisions, credit cards have transformed the way we engage with money. Their impact extends beyond convenience—they shape credit scores, influence mortgage approvals, and increasingly serve as tools for financial empowerment. Yet, as powerful as credit cards have become, they remain rooted in a simple premise: trust. For mortgage seekers in particular, credit cards can either open the door to homeownership or quietly undermine it, depending on how they’re managed. As we look ahead to a future of biometric payments and AI underwriting, one thing remains clear: Credit cards are no longer just pieces of plastic—they’re dynamic instruments of financial strategy and personal opportunity.