As a professional mortgage agent, it’s my duty to guide my clients towards financing solutions that are not only competitive but also aligned with their goals and circumstances. Today, I’m excited to introduce you to RFA Mortgage Corporation—a strong, innovative lender that many Canadians may not yet know by name but absolutely should. Allow me to explain why RFA deserves serious consideration for your next mortgage and why they are emerging as one of the most client-centric lenders in Canada.

Who is an Ideal Client for RFA?

Three Powerful Reasons to Choose RFA

Who is RFA Mortgage Corporation?

RFA stands for Realty Financial Advisors. Founded in 1996, RFA began its journey in the real estate investment world, successfully acquiring and managing commercial properties. Fast forward to today, RFA Mortgage Corporation operates coast-to-coast (excluding Quebec), is fully licensed as a Schedule I Bank, and has become a significant presence in the residential mortgage market. With over $31 billion in prime residential mortgages under management, 185 full-time employees, and a team of highly experienced underwriters, RFA is built for strength, service, and growth.

They have a robust infrastructure that emphasizes personal service, direct access to underwriters, and highly competitive mortgage programs for both prime (“A”) and alternative (“B”) borrowers. With a unique blend of bank stability and boutique service, RFA is positioned to offer the best of both worlds.

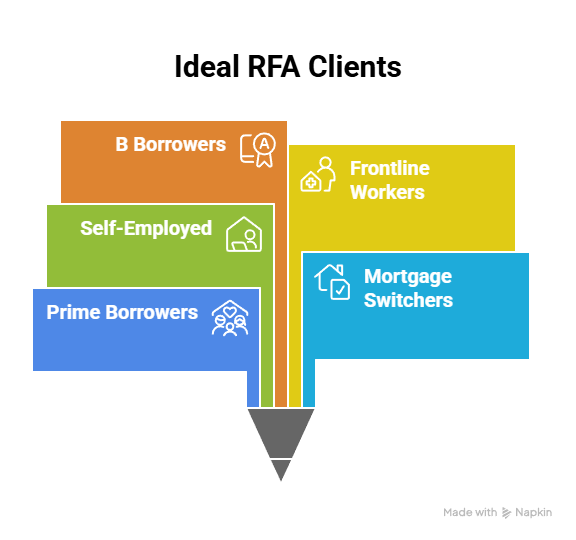

Who is an Ideal Client for RFA?

In the dynamic landscape of Canadian real estate financing, RFA shines as a highly adaptable and client-focused lender. Based on their programs, underwriting flexibility, and service philosophy, an ideal RFA client profile would include:

- Prime Borrowers Seeking Competitive Rates with Full Features

- Borrowers Switching or Transferring Mortgages

- Self-Employed Individuals and BFS Clients

- Frontline Workers Seeking Rewarding Mortgage Incentives

- B Borrowers Ready to Graduate to Prime Lending

Prime Borrowers Seeking Competitive Rates with Full Features

RFA is exceptionally strong for clients who:

- Qualify for insured or insurable mortgage rates (i.e., purchases under $1M at the time of acquisition).

- Want full prepayment privileges (20/20) and favourable penalty structures without the restrictions often hidden in “no-frills” products.

- Appreciate excellent online account access and responsive customer service after funding.

Typical examples:

- First-time homebuyers

- Young families upsizing into a second home

- Conservative investors purchasing rental properties that qualify under insured guidelines

Borrowers Switching or Transferring Mortgages

RFA is a powerhouse for mortgage transfers, including:

- Standard or collateral charge switches (especially where clients want to avoid full refinance costs).

- Clients looking to add or remove a borrower during a transfer without triggering a full refinance.

- Existing homeowners consolidating first mortgages and HELOCs under one loan without the need for new funds.

Ideal candidates:

- Homeowners looking to renew from a big bank without paying fees

- Borrowers locked into collateral mortgages elsewhere but seeking better terms

- Clients seeking smoother title changes (adding/removing spouse, parent, or child)

Self-Employed Individuals and BFS Clients

With dedicated programs for the self-employed, RFA is ideal for:

- Business-for-self clients with over two years of stable income, leveraging stated income programs.

- Newly self-employed individuals under two years using the CMHC BFS Enhanced Program with supportive documentation.

- Clients whose income patterns are legitimate but unconventional, needing human-underwritten flexibility.

Common profiles:

- Entrepreneurs

- Tradespeople

- Consultants and freelancers

Frontline Workers Seeking Rewarding Mortgage Incentives

Thanks to their Frontline Worker Program, RFA uniquely supports essential service providers such as:

- Police officers, paramedics, firefighters

- Nurses, doctors, lab technicians

- Teachers and educational staff

Eligible clients benefit from a 10 bps rate discount and up to $2,000 cash back — an extremely rare ongoing offer in the Canadian mortgage space.

B Borrowers Ready to Graduate to Prime Lending

Through their Graduation Program, RFA makes it seamless for:

- Clients coming off private or alternative B lending.

- Borrowers with improved credit profiles looking to access prime insurable rates.

- Clients who originally needed flexibility but are now ready for mainstream terms.

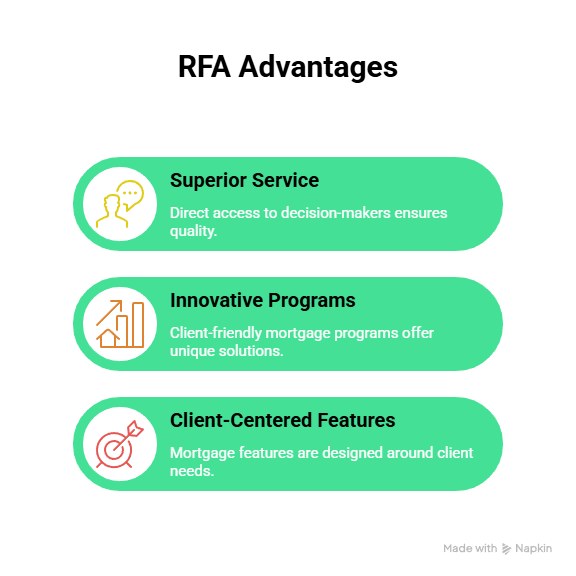

Three Powerful Reasons to Choose RFA

Top lenders differentiate themselves in the mortgage market by providing unique products, special offerings, or tailored solutions to address specific client-situation needs. The following are my 3 powerful reasons to choose RFA:

- Superior Service Model – Direct Access to Decision-Makers

- Innovative and Client-Friendly Mortgage Programs

- Client-Centered Mortgage Features

Superior Service Model – Direct Access to Decision-Makers

One of the key advantages of working with RFA is the direct relationship clients and brokers can build with their assigned underwriters. From application to funding, your file is managed by a dedicated underwriting team, not passed through layers of departments. If you need clarification, mitigation strategies, or special consideration on a file, RFA’s approach allows real-time collaboration. This is a stark contrast to some larger lenders, where brokers are often left communicating through portals or call centres.

Why it matters: Faster answers, smoother transactions, and a significantly reduced risk of last-minute surprises. Your file gets the attention it deserves from start to finish.

Innovative and Client-Friendly Mortgage Programs

RFA stands out for the breadth and flexibility of its mortgage programs. Here are just a few examples:

- Seamless Transfers and Switches – including both standard and collateral charge transfers, often with no legal fees or appraisals required. They even allow title changes (adding/removing family members) during a switch without treating it as a costly refinance.

- Frontline Worker Program – an exclusive offer providing emergency and educational frontline workers (police, paramedics, nurses, doctors, teachers, and more) with a 10-basis point rate discount and up to $2,000 cash back. No other lender in Canada offers this ongoing recognition.

- Graduation Program – for clients moving from alternative lending to prime lending, RFA offers a structured, easy path back to A-side financing without full refinancing costs.

- Flexible BFS Programs – for self-employed individuals, whether operating more than two years or under two years (with CMHC-enhanced programs), RFA has workable stated income solutions.

Why it matters: Whether you are a first-time buyer, a self-employed entrepreneur, a frontline worker, or simply looking for better terms on an existing mortgage, RFA has thoughtfully designed solutions that meet real-world needs.

Client-Centered Mortgage Features

RFA’s mortgage products are deliberately structured with client flexibility and fairness in mind:

- 20/20 prepayment privileges – allowing borrowers to pay down their mortgage faster without penalties.

- Favourable payout penalties – RFA uses an Interest Rate Differential (IRD) calculation that is client-friendly compared to many banks’ punitive methods.

- No “no-frills” traps – Every RFA product comes fully featured; there are no stripped-down products with hidden restrictions like bona fide sale clauses.

- Blended Rate Portability – Clients can move and “blend and extend” their mortgage rate, maintaining flexibility during life transitions.

- Outstanding Client Portal – Clients can make lump sum payments, adjust payment schedules, and access important account information with ease, saving time and hassle.

Why it matters: Today’s mortgage consumers want more control and less red tape. RFA delivers that in a clear, accessible way.

Why RFA Stands Apart

In a landscape crowded with familiar names, RFA differentiates itself with exceptional service, innovative products, and a genuine commitment to client success. They are “big enough to make an impact, but small enough to listen and adapt.” This balance allows RFA to offer faster turnaround times, customized underwriting, and programs that truly respond to the needs of modern Canadian families and investors.

If you are looking for real estate financing and value a lender that treats you as more than just a number, RFA Mortgage Corporation is a partner worth considering. As your mortgage agent, I am proud to connect you to options like RFA that open doors — not just to properties, but to better financial futures.