…Knowing that Can Save You Thousands

When you signed your mortgage, you were probably laser-focused on one number: your interest rate. What most Canadians don’t realize is that buried inside their chartered bank’s mortgage contract is another number — the original posted rate — and if you ever need to break your mortgage early, that number is going to matter a lot!

Breaking a mortgage before the term is up isn’t unusual. People sell homes, refinance to access equity, take advantage of lower rates, or go through a separation. Whatever the reason, when you break a fixed-rate mortgage with one of Canada’s Big 6 banks, you’re almost certainly going to pay a prepayment penalty — and that penalty is calculated using a formula called the Interest Rate Differential (IRD). The IRD hinges on the original posted rate, and if you don’t know how to find it, you’re flying blind.

So let’s now talk about posted rates, and why it matters when calculating a bank’s mortgage penalties:

What Is a Posted Rate and Why It Matters

How the IRD penalty is calculated

Where to find today’s current posted rates

Where to Find Historical Posted Rates

What Is a Posted Rate and Why It Matters

Your bank’s mortgage has a discounted rate — the rate you actually pay — and a posted rate, which is the higher, non-discounted rate the bank advertises publicly. When you signed, your bank may have offered you a “special” rate. But their posted 5-year rate at the time might will have been substantially higher. That difference is your discount, and it’s not just a marketing number — it’s baked into their penalty formula.

The banks use posted rates in IRD calculations because it’s how their contracts are written. It’s perfectly legal, and it’s been the standard practice for decades. It also tends to produce significantly higher penalties than you’d get with a monoline lender or credit union, which is something every borrower at a Big 6 bank should understand before they sign.

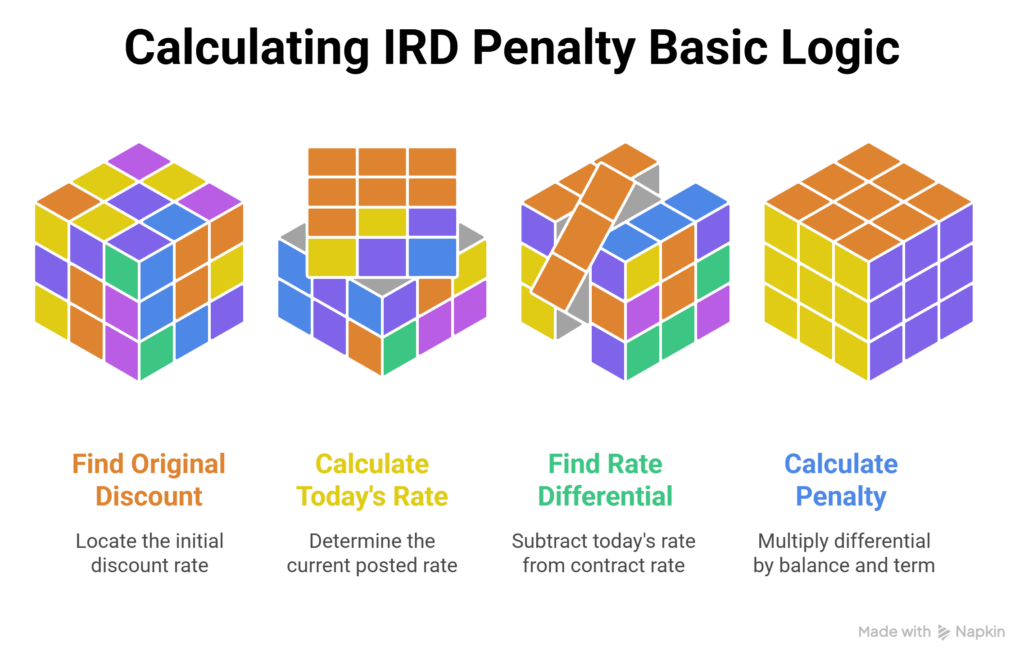

How the IRD Penalty Is Calculated (kind of)

For variable-rate mortgages, the penalty is simple: three months’ interest. But for fixed-rate mortgages at the Big 6, the bank charges you the greater of three months’ interest or the IRD. And the IRD is almost always the bigger number when rates have dropped since you signed.

You should also know that each bank calculates their bank’s mortgage penalties a little bit differently, which makes it really hard to make direct comparisons.

Here’s the basic logic of the IRD for most Big 6 banks (except CIBC, which uses a slightly different variation):

Step 1: Find your original discount. This is the difference between the posted rate when you signed and your actual contract rate.

Step 2: Take today’s posted rate for a term closest to your remaining term, and subtract that same original discount.

Step 3: Subtract that result from your contract rate to get the rate differential.

Step 4: Multiply that differential by your mortgage balance and your remaining term in years.

The result can be eye-watering — easily $10,000 to $30,000 or more on a typical mortgage. This is exactly why knowing how to find these posted rates matters so much.

Where to Find Current Posted Rates

If you need today’s posted rates — which you’ll use as the “current posted rate for the matched remaining term” in the IRD formula — your first stop is each bank’s own mortgage rate page. Here’s the thing though: banks don’t make posted rates easy to find. They love to lead with their discounted “special offer” rates, which are the flashy numbers in the ads. You’ll often need to look for a secondary table, a footnote, or a section labelled “posted rate” or “standard rate.”

Head directly to the mortgage section of each bank’s website:

- RBC: rbc.com/mortgages

- TD: td.com/mortgages

- Scotiabank: scotiabank.com/mortgages

- BMO: bmo.com/mortgages

- CIBC: cibc.com/mortgages

- National Bank: nbc.ca/mortgages

If you can’t locate the posted rate on the website, just call. Banks are required to disclose their posted rates. Don’t let a phone call stand between you and a potentially thousands-of-dollars savings decision.

Where to Find Historical Posted Rates

The original posted rate — the one that existed on the day you signed your mortgage — is the linchpin of the whole calculation.

Here’s where to look, in order of reliability:

- Your mortgage commitment letter or disclosure document. This is the single best source. Federally regulated lenders are required to disclose the posted rate at the time of funding. It’s typically on the first page of your commitment, right beside your contract rate and the discount you received. If you’ve got that paperwork, your job is done.

- The Bank of Canada historical rate tables. The Bank of Canada publishes historical chartered bank posted mortgage rates going back decades, updated weekly. This is the most authoritative public source and it’s completely free. Navigate to bankofcanada.ca, then look for “Selected Canadian and U.S. interest rates” and drill into “Chartered bank mortgage rates.” You’ll find posted rates broken out by term — 1-year, 2-year, 3-year, 4-year, 5-year, 7-year, and 10-year — for whatever date your mortgage was signed. Bookmark this page. It’s gold.

- Your bank’s payout statement. When you request a formal payout statement, the bank is legally required to show its full calculation, including the posted rate it’s using for the IRD. This is the definitive number for penalty purposes. The catch is that it can take up to five business days to receive, and posted rates can shift in the meantime — so it’s better for confirming a number than for initial planning.

A Posted Rate Scenario

Meet Sandra and Mike. They bought their home in the fall of 2022 and signed a 5-year fixed mortgage with one of the Big 6 banks at 5.29%. The posted rate at the time was 6.84% — a discount of 1.55%. Life was good, the payments were manageable, and they didn’t give the mortgage much thought.

Fast forward to early 2025. Sandra gets a significant promotion — the kind that comes with a relocation to a different city. They decide to sell. Their realtor, David, is fantastic at finding buyers but isn’t sure how to answer their question: “how much is it going to cost us to get out of this mortgage?” He tells them “something like three months’ interest” — a common misconception.

Sandra googles it. She finds her mortgage balance is around $430,000, with about 31 months remaining on the term. She pulls up her commitment letter, finds the original posted rate of 6.84%, and checks the Bank of Canada table for the current Big 6 posted 2-year rate, which is sitting at 5.79%.

Her original discount was 1.55%, so the comparison rate is 5.79% − 1.55% = 4.24%. The differential between her contract rate (5.29%) and the comparison rate (4.24%) is 1.05%. Applied to a $430,000 balance over 31 months (roughly 2.58 years), the IRD works out to approximately $11,637 — almost four times what “three months’ interest” would have been.

Armed with that number, Sandra and Mike were able to factor the penalty into their sale price negotiations, avoid an unwelcome surprise at closing, and have a much more honest conversation with their realtor about their net proceeds. David, for his part, now asks every listing client about their mortgage terms before setting a sale strategy.

Allen’s Final Thoughts

The posted rate isn’t a bureaucratic footnote. It’s the fulcrum that your entire prepayment penalty balances on, and understanding it puts you in control of one of the biggest financial decisions you’ll make. Whether you’re buying, selling, refinancing, or just doing a gut-check on where you stand, knowing how to find this number — and what to do with it — is genuinely empowering.

Canada’s mortgage market is not always designed to make this easy for you. Rates are advertised in ways that obscure the posted rate, payout statements can take a week to arrive, and the IRD formula — which everyone calculates differently — isn’t exactly spelled out on the back of a napkin either. That’s exactly why having a good mortgage agent in your corner matters.

You shouldn’t have to be a mortgage agent to protect yourself from unexpected costs — but it helps to know one. If you’re thinking about breaking your mortgage, refinancing, selling, or just want to understand what your options are, reach out. A 15-minute conversation could save you a lot more than you’d expect.