… Where Deals Are Won, Lost, or Quietly Saved

Buying a home isn’t just about price — it’s about timing, certainty, and risk management. And nowhere is that more obvious than when you’re staring down a condition of financing. On paper, it sounds simple: get a mortgage commitment by a certain date or walk away. In practice, it’s one of the most stressful pressure points in the entire transaction, especially when markets are competitive and timelines are tight.

There is a lot that isn’t well understood by both realtors and clients because my world of real estate financing is a black box and poorly understand.

I’ve seen deals glide through calmly — and I’ve seen others unravel at the eleventh hour. The difference usually isn’t the lender. It’s preparation, documentation, and how well everyone understands what that financing condition actually means.

Topics I’ll cover in this article:

What is the condition of financing

Why the financing condition creates so much pressure

What happens if you miss the financing deadline

How long different lenders really take to issue a commitment

Why documentation is the true bottleneck in underwriting

How buyers often become the biggest challenge

How realtors and buyers can use this information strategically

What is the condition of financing

A condition of financing is a contractual safety net. It gives the buyer a defined period — usually 5 to 7 business days, but often longer and many times 5 days is too tight — to secure a written mortgage commitment that allows them to confidently move forward with the purchase.

Notice I said mortgage commitment and not pre-approval or, god forbid, pre-qualification (which is absolutely nothing at all). A mortgage commitment is a formal, written approval from a lender confirming that they are prepared to lend a specific amount of money to a buyer on defined terms, subject to stated conditions (see my 10 Commandments for more information).

When you get a mortgage commitment, you have to sign it:

- Acknowledging the terms offered (rate, term, amortization, payment)

- Acknowledging the conditions still outstanding

- Confirming they intend to proceed with that lender, subject to those conditions

- Allowing the lender to continue toward funding (because they haven’t underwritten anything yet)

It is the document that allows a buyer to confidently waive the condition of financing.

Until that condition of financing is waived:

- The deal is conditional

- The buyer is not fully locked in

- The seller is exposed to uncertainty

- Everyone is watching the calendar

Waiving the condition is the buyer saying, “Financing is in place. I’m all in.” And once it’s waived, there’s no rewind button. You are committed.

Why the financing condition creates so much pressure

The pressure comes from the collision of real estate timelines and mortgage underwriting realities.

Realtors work in days.

Lenders work in documentation cycles.

Buyers work… well, between their jobs, families, and everything else.

Now add:

- Competing offers

- Shortened conditions

- Appraisals

- Insurer rules

- Underwriter questions

Suddenly, a 5 to 7-day condition doesn’t feel like 5-7 days at all. It feels like a ticking clock, or a ticking time bomb.

What happens if the financing deadline is missed

This part is critical — and often misunderstood.

If the buyer fails to waive or extend the financing condition by the deadline, one of three things happens:

- First, the deal dies cleanly if the condition isn’t waived and the buyer elects to walk away properly.

- Second, the seller may agree to an extension, but that’s a negotiation — not a right.

- Third, and most dangerous, the buyer misses the deadline and remains silent. At that point, legal risk creeps in fast. The seller may treat the deal as firm, or claim breach, depending on the wording and actions taken.

Financing conditions are not casual. Deadlines matter.

How different lenders really compare on speed

Not all lenders underwrite at the same pace, and this directly affects how safe — or risky — a financing condition becomes.

Big banks typically take 5 to 7 business days. They’re reliable, but layered approvals, branch involvement, and appraisal timing can slow things down. 5 to 7 days is a rule of thumb, it can sometimes be done in 3 and can take 10 or longer… it depends!

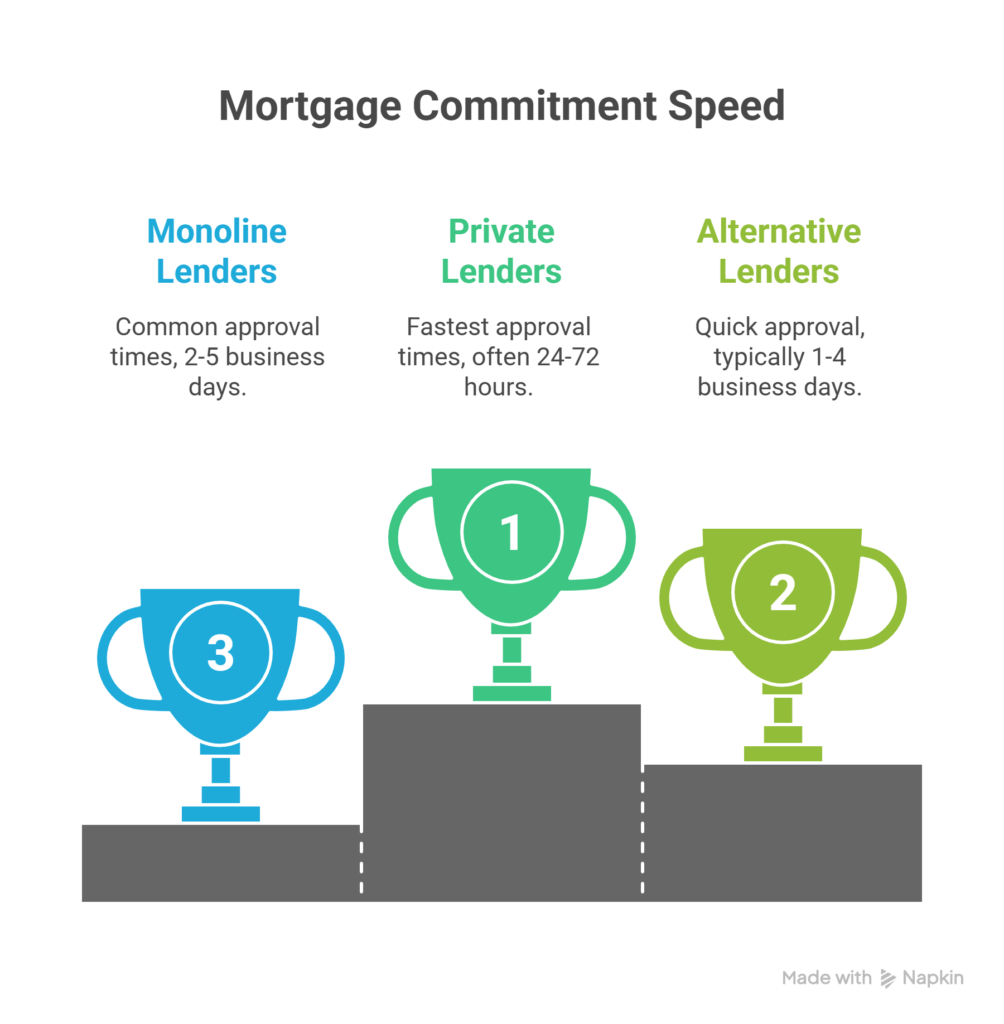

Monoline lenders are often faster, commonly 2 to 5 business days, because their entire business is mortgages. Centralized underwriting and cleaner processes help. When time is of the essence, monolines are my go to play because of their responsiveness; they are great lenders!

Trust companies usually fall in the 3 to 6 business day range, with good consistency and slightly more flexibility than banks, but every trust company is different.

Credit unions are variable, which means, they are on a spectrum, and each one is very different and can be unpredictable. Some are lightning fast (sometimes), others slower (except when they are lightning fast… for some reason???), depending on local underwriting and volume. Expect 3 to 10 business days.

Alternative lenders can often issue commitments in 1 to 4 business days, especially for non-standard income files, because underwriting is manual and direct.

Private lenders are the fastest, sometimes 24 to 72 hours, because decisions are asset-based — but speed comes with higher costs and shorter terms.

The takeaway? Speed isn’t about prestige. It’s about process fit.

Why documentation is the real bottleneck

Here’s the professional truth most people don’t say out loud:

Underwriting doesn’t start until the last document is in.

Lenders don’t underwrite on promises, intentions, or “I’ll send it tonight.” They underwrite on:

- Complete income documents

- Verified down payment sources

- Clear bank statements

- Explained deposits

- Property details they can defend

Every missing page pauses the file. Every unclear item triggers questions. Time doesn’t slow — underwriting does.

Some institutions are very large, like the chartered banks. They are not only dealing with purchases, but renewals, refinances, HELOCs, seconds, power of sales, and so on… purchases are just one aspect of their underwriting. They have an assembly line process for efficiency. They have checklists they work through where everything needs to be there and complete, if not, your mortgage gets sent back to the end of the line until everything is complete. Days turn into weeks.

How buyers often become the biggest challenge

Most delays aren’t caused by lenders. They’re caused by perfectly well-intentioned buyers who are busy, distracted, or unaware of the stakes.

Common issues I see:

- Partial document uploads

- Screenshots instead of full PDFs

- Missing pages of bank statements

- Unexplained transfers

- Delayed responses during a short condition window

Ironically, strong borrowers are often the slowest — because they assume everything will be easy. Meanwhile, self-employed or complex borrowers are usually hyper-organized, because they know documentation matters, despite having the most complex files!

A story from the trenches

Two buyers. Same building. Same lender. Same week.

Buyer A submitted every document within 24 hours of offer acceptance. Appraisal ordered immediately. Underwriter reviewed once. Commitment issued on day three.

Buyer B sent documents “as they found them.” Missing pages. Follow-ups. Delays. Appraisal ordered late. No commitment by day six. Stress everywhere. Extension requested. Seller nervous.

Same lender. Same market. Totally different outcomes.

How realtors and buyers can put this into practice

For buyers:

- Gather documents before offer night

- Respond to requests the same day

- Ask why documents matter — don’t ignore them

- Treat the financing condition as a real deadline

For realtors:

- Encourage a pre-review by me, not just a pre-approval, before the offer presentation

- Avoid over-shortening conditions without preparation

- Don’t be afraid to ask for more than the 5 to 7 days to waive conditions; you don’t know what kind of lender your client will eventually end up using. If you need to go shorter, contact me first… to see if I can get an exception from the lender, or move the file over so it can be done by deadline.

- Loop the me in early — not after the offer is signed. If a document is missing and needs to be ordered from the government, your client may not be in a position to make an offer at all.

Shorter conditions don’t come from optimism. They come from prep. Every battle is won before it is ever fought!

Let’s set our clients up for success!

Allen’s Final Thoughts

Waiving the condition of financing isn’t about luck, speed, or bravado. It’s about certainty.

Different lenders take different amounts of time. Underwriters all think differently. But the single biggest variable in the entire process is still the buyer — their organization, responsiveness, and willingness to treat documentation seriously.

My role as a mortgage agent isn’t just to find a lender. It’s to anticipate underwriting, align the right lender to the right timeline, and make sure buyers don’t accidentally become the biggest risk in their own transaction.

I work with buyers to pre-organize, pre-review, and pre-empt issues. I work with realtors to structure safer offers, cleaner timelines, and fewer surprises. And when pressure is high — which it often is — I’m there to keep the deal calm, defensible, and on track.

That’s how financing conditions get waived with confidence — not crossed fingers.