…What You Need to Know

Did you know that the current prime rate in Canada is 6.45%? The prime rate is a key benchmark used by Canadian banks to price many variable-interest financial products, including variable-rate mortgages, lines of credit, and certain loans.

While the prime rate closely follows decisions made by the Bank of Canada, it is not set by the central bank itself. Instead, each financial institution sets its own prime rate — though in practice, Canada’s major banks almost always move in lockstep.

Understanding how the prime rate works, how it differs from the Bank of Canada’s overnight rate, and how it affects borrowing and saving decisions is essential in today’s interest-rate environment.

Key Takeaways

- The Canadian prime rate is currently 6.45%.

- The prime rate is a benchmark, not a minimum — borrowing rates can be priced below or above prime.

- Prime closely tracks changes to the Bank of Canada’s overnight rate, but is set by individual banks.

- Changes in prime directly affect variable-rate borrowing costs.

- Savers are affected more indirectly, and often with a delay.

Understanding the Prime Rate

The prime rate (often called the prime lending rate) is the benchmark rate Canadian banks use to price variable-interest products, including:

- Variable-rate mortgages

- Home equity lines of credit (HELOCs)

- Personal and business lines of credit

- Certain variable-rate loans

The actual rate a borrower receives is expressed as prime plus or minus a spread, based on risk, product type, and market competition.

Contrary to common belief, customer rates can absolutely be lower than prime. In fact, most competitive variable-rate mortgages are priced at prime minus a discount.

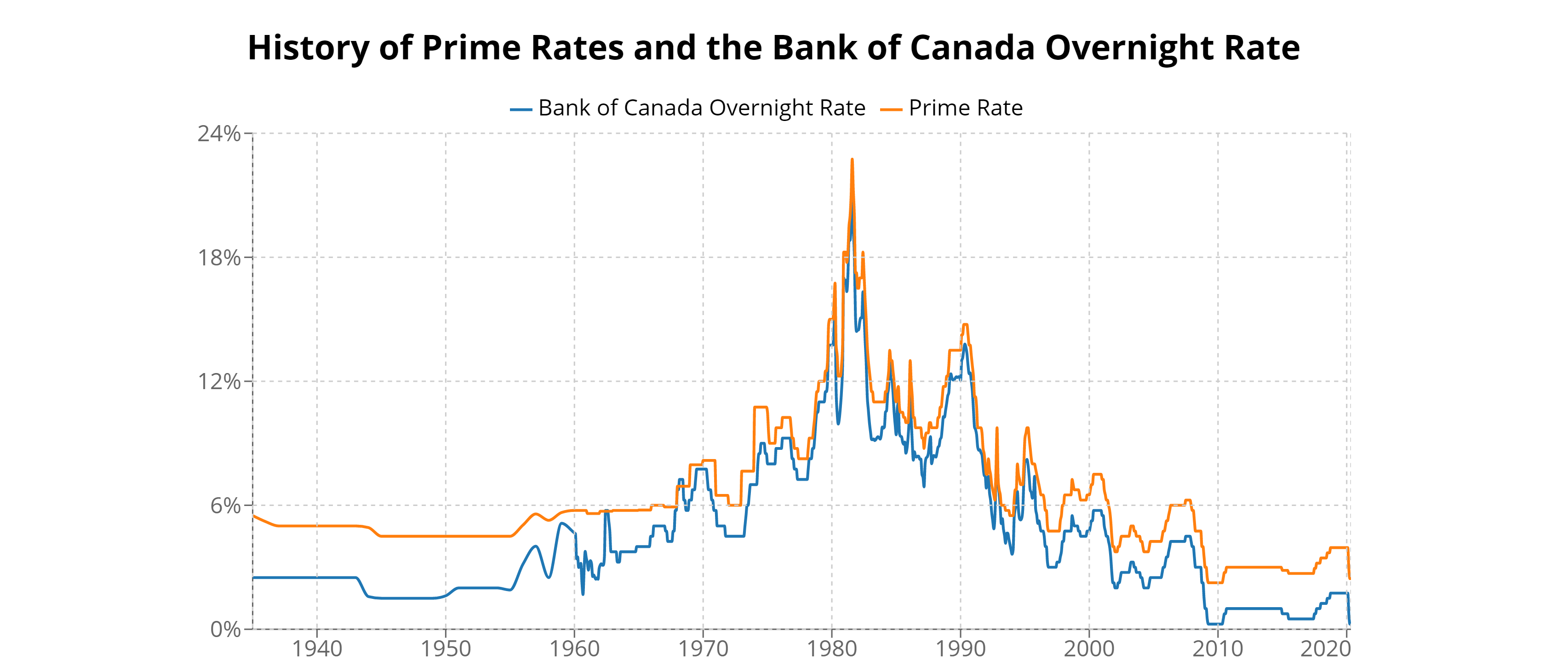

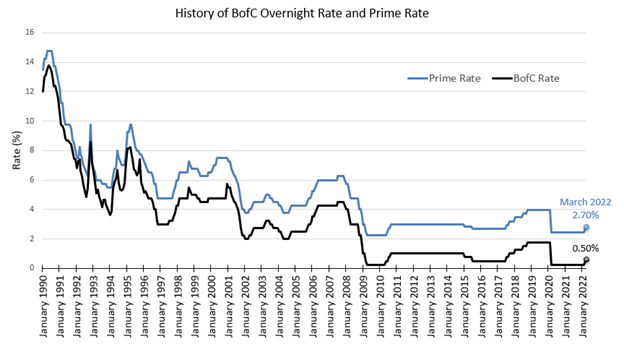

Prime Rate vs. Overnight Rate — What’s the Difference?

The overnight rate is the policy interest rate set by the Bank of Canada. It represents the rate at which major financial institutions lend to one another overnight and is the primary tool used to control inflation and economic activity.

The prime rate is a commercial lending benchmark set by banks, typically calculated as:

Prime ≈ Overnight Rate + ~2.20%

When the Bank of Canada raises or lowers the overnight rate, banks almost always adjust their prime rate by the same amount, usually on the same day.

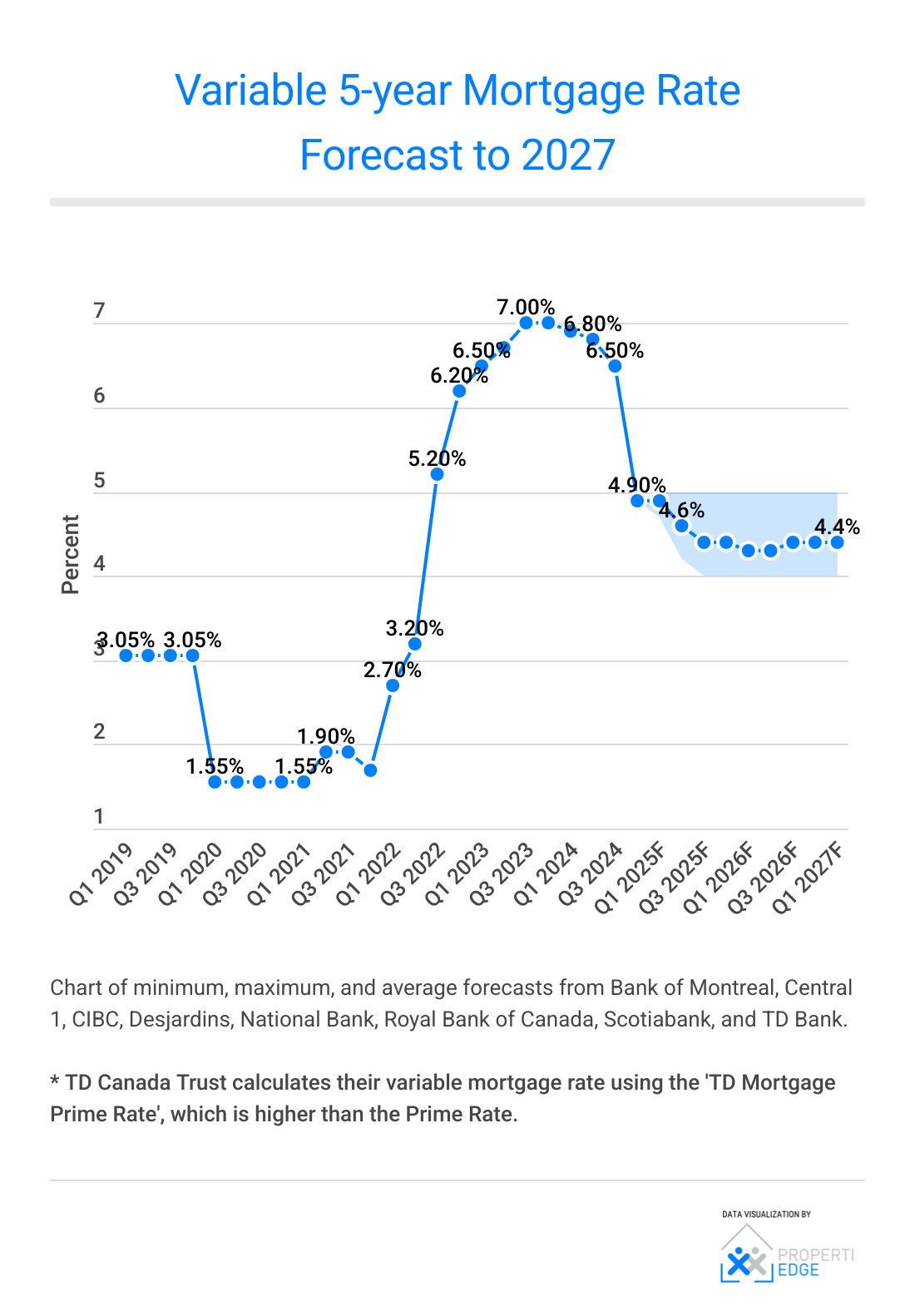

Variable Mortgage Pricing — How Prime Minus Spreads Work

Here’s a simple example of how variable mortgage pricing works in Canada:

- Prime rate: 6.45%

- Borrower’s discount: Prime – 0.75%

- Actual mortgage rate: 5.70%

If the prime rate changes, the borrower’s rate moves in direct proportion, unless the mortgage has a static-payment structure where amortization adjusts instead of payment.

This pricing model is why variable-rate borrowers feel rate changes immediately — for better or worse.

What Influences the Prime Rate?

Bank of Canada Policy

The Bank of Canada adjusts the overnight rate to control inflation and stabilize the economy. Prime follows these decisions closely.

Inflation and Economic Conditions

Higher inflation typically leads to higher policy rates, while slowing economic activity can result in rate cuts.

Bank Funding Costs

While competition affects pricing to prime, it does not meaningfully affect the prime rate itself. Major banks almost always maintain the same prime rate.

Impact of the Prime Rate on Borrowers

Variable-Rate Mortgages

When prime rises or falls, interest costs on variable-rate mortgages change accordingly. Depending on the mortgage structure, this may affect:

- Monthly payments, or

- Amortization length

Lines of Credit and Loans

Most personal and business lines of credit are priced at prime plus a premium, meaning interest costs move immediately with prime.

Credit Cards

Most Canadian credit cards have fixed or discretionary rates, not direct prime-based pricing. Only select low-rate or professional cards use prime-linked formulas.

Impact of the Prime Rate on Savers

The prime rate influences savings indirectly, not mechanically.

When prime rises:

- Borrowing rates usually increase immediately

- Savings rates may rise later, and often by less

Savings products affected include:

- High-interest savings accounts

- Guaranteed Investment Certificates (GICs)

Large banks are often slow to raise savings rates, while online banks and smaller institutions tend to respond more quickly.

Historical Prime Rate Trends in Canada

- Record high: 22.75% (1981)

- Record low: 2.25% (2009)

- 2020–early 2022: 2.45%

- March 2022–July 2023: Rapid increases to 7.20%

- 2024–2025: Gradual decline back to 6.45%

Understanding these cycles helps borrowers and savers plan more strategically rather than reacting emotionally to short-term rate movements.

Conclusion

The prime rate is one of the most important reference points in the Canadian financial system. It directly affects borrowing costs for millions of Canadians and indirectly influences savings returns.

By understanding how prime works, how it differs from the Bank of Canada’s overnight rate, and how variable-rate products are priced using prime-minus spreads, borrowers and savers can make more informed, confident decisions.

Interest-rate cycles are inevitable. Clarity — not prediction — is what allows you to navigate them intelligently.

Frequently Asked Questions

What is the prime rate?

The prime rate is a benchmark interest rate set by Canadian banks and used to price many variable-interest financial products.

Who sets the prime rate in Canada?

Individual banks set their own prime rates, but they typically move together in response to Bank of Canada overnight rate changes.

Can mortgage rates be lower than prime?

Yes. Many variable-rate mortgages are priced at prime minus a discount.

Do savings rates move with prime?

Sometimes — but usually more slowly and less predictably than borrowing rates.

If you’d like, I can next:

- Convert this into a client-facing explainer PDF

- Add interactive calculators (prime change impact, payment sensitivity)

- Turn this into a script or slide deck for realtors or webinars

Just tell me where you want to deploy it.