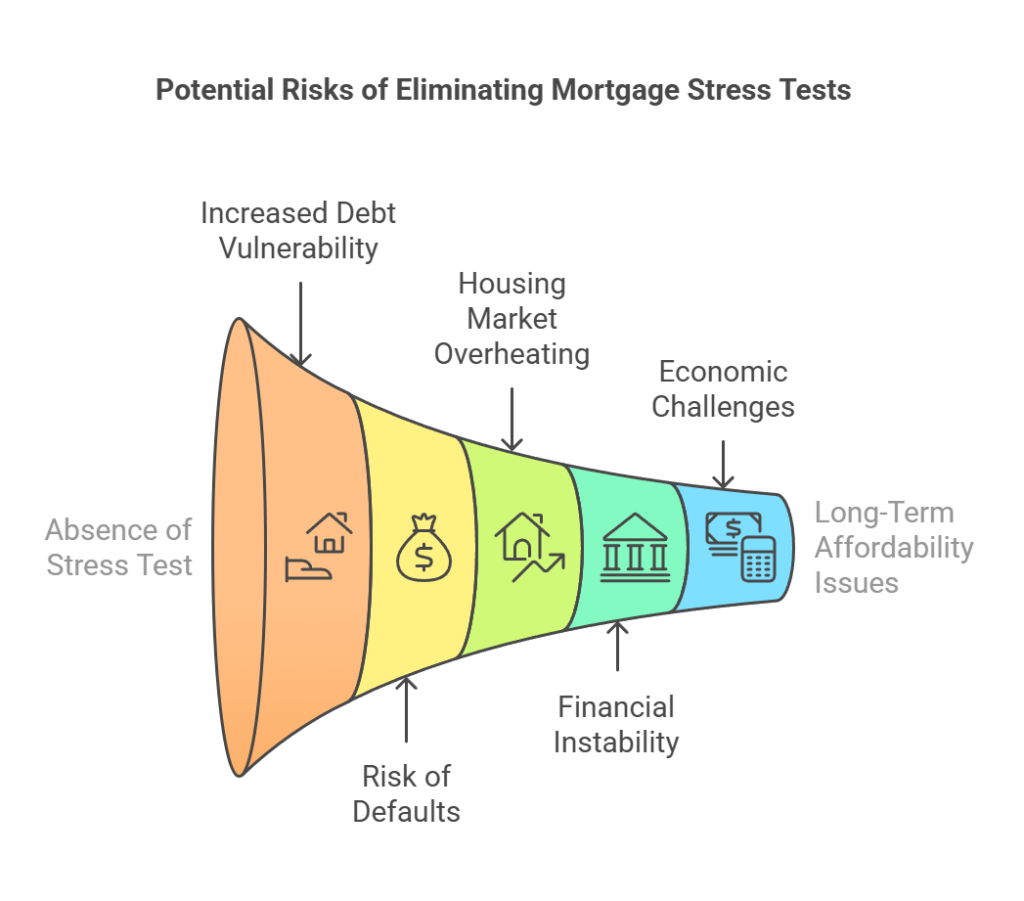

What could happen OSFI did not mandate the implementation of the stress test?

If the Office of the Superintendent of Financial Institutions (OSFI) had not mandated the implementation of the mortgage stress test in Canada, several potential risks and consequences could have arisen, affecting individual borrowers, the housing market, financial institutions, and the broader economy. These include:

Increased Household Debt Vulnerability

Heightened Risk of Mortgage Defaults

Overheating of the Housing Market

Long-Term Affordability Challenges

Increased Household Debt Vulnerability

Without the stress test, more borrowers might have qualified for larger mortgages based on lower interest rates. This could have led to higher levels of household debt, making individuals more vulnerable to financial strain in the event of economic downturns, job losses, or interest rate hikes.

Heightened Risk of Mortgage Defaults

In the absence of the stress test, borrowers who stretched their financial limits to obtain larger mortgages might have faced difficulties making payments if interest rates rose or if their financial circumstances changed. This could have resulted in an increase in mortgage defaults.

Overheating of the Housing Market

The stress test helps moderate housing demand by ensuring that borrowers do not take on more debt than they can afford. Without it, there could have been a continued escalation in housing prices, particularly in hot markets, potentially leading to a housing bubble and unsustainable price growth.

Financial System Instability

A lack of stress testing could have exposed banks and other lenders to greater risks, as their mortgage portfolios would include more loans to highly leveraged borrowers. This could have implications for the stability of the financial system, especially in the face of economic shocks.

Reduced Lending Standards

The stress test serves as a regulatory tool to maintain prudent lending standards. Without it, there might have been a relaxation of lending criteria, increasing the likelihood of riskier lending practices.

Impact on Economic Stability

The broader economy could be impacted by the absence of the stress test. A housing market correction or a wave of defaults could have significant repercussions on consumer spending, economic growth, and financial stability.

Long-Term Affordability Challenges

While the stress test may make it more difficult for some to purchase homes, it also aims to ensure long-term affordability and sustainability. Without it, more borrowers might find themselves in homes they cannot afford in the long run.

It’s important to note that while the stress test aims to mitigate these risks, it is also subject to criticism and debate, particularly regarding its impact on housing accessibility and affordability for certain groups of borrowers. The balance between financial prudence and housing market accessibility remains a key consideration in the ongoing evaluation and adjustment of mortgage lending policies in Canada.