… The Metric That Separates Amateur Deals from Professional Decisions

In real estate, it’s easy to get caught up in surface-level numbers—cash flow, purchase price, appreciation. But if you really want to operate like a professional investor, and guide your clients like one, you need a metric that answers a deeper question:

“How hard is my money actually working for me over time?”

That’s where IRR—Internal Rate of Return—comes in.

It’s not just a formula. It’s a lens. A decision-making framework. And once you start using it properly, you’ll never look at deals the same way again.

What I’ll Cover

Why IRR is necessary in real estate investing

Who uses IRR—and how professionals apply it

How IRR is used to evaluate deals

A successful deal example (and why it worked)

A failed deal example (and what went wrong)

How IRR fits into your broader real estate and mortgage strategy

How realtors and clients can apply IRR in everyday decisions

A real-world story to bring it all together

What Is IRR

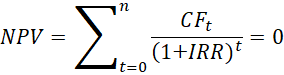

At its core, IRR is the annualized rate of return that an investment generates over time, taking into account the timing of cash flows.

Mathematically, it’s the discount rate that makes the Net Present Value (NPV) equal to zero.

Where:

= cash flow at time

- IRR = the return you’re solving for

In simpler terms, IRR is your true annual return, factoring in:

- When you invest money

- When you receive income

- When you pull equity out

- When you sell

In other words:

It’s not just how much you make.

It’s how fast your money compounds.

Because two deals can make the same profit—but one can take half the time. IRR exposes that difference instantly.

Why IRR Is Necessary in Real Estate

Real estate is not a clean, one-line investment.

You have:

- Upfront capital (down payment, closing costs)

- Uneven cash flow

- Refinance events

- Appreciation over time

- A potential exit

If you are only looking at:

- Cash flow, you are missing appreciation

- Appreciation, you are ignoring time

- ROI, you are ignoring timing

IRR ties it all together. It forces you to think like a capital allocator, not just a property owner.

IRR matters because it answers:

“What is my true annual return considering when I receive money?”

Key Insight: A dollar today is worth more than a dollar 5 years from now. IRR captures that.

Who Uses IRR and How They Use It

This is not just for analysts.

Investors

They use IRR to:

- Compare deals quickly

- Decide whether to hold or sell

- Evaluate BRRRR or flip strategies

Realtors

They use IRR to:

- Help clients understand long-term value

- Position investment properties strategically

- Differentiate themselves from transactional agents

Mortgage Professionals

This is where it becomes especially powerful.

You use IRR to:

- Structure financing strategies (refinance timing, leverage)

- Help clients understand opportunity cost

- Guide decisions beyond just approval

You are no longer just arranging debt. You are advising on wealth creation.

How IRR Is Used to Evaluate Deals

When you look at a deal through an IRR lens, you are asking:

- How quickly do I recover my capital?

- When do major returns occur?

- Is my equity sitting idle?

And most importantly:

“Is this the best use of my money right now?”

A Successful Deal: When IRR Works in Your Favour

Let’s say your client buys a duplex in Oshawa.

- Purchase: $700,000

- Down payment: $140,000

- Renovation: $60,000

- Total invested: $200,000

They execute a strong BRRRR strategy:

- Refinance after 12 months

- Pull out $150,000

- Cash flow: $600 per month

What happens?

Most of their capital comes back quickly, while the property continues generating income.

That creates a very strong IRR, often exceeding 20 percent.

The reason is simple. Their money was not tied up for long.

A Failed Deal: When IRR Exposes the Truth

Now consider a different scenario.

A client buys a condo:

- Purchase: $600,000

- Down payment: $120,000

- Cash flow: $100 per month

- Hold: 5 years

- Sale price: $700,000

On the surface, it looks acceptable. There is $100,000 in appreciation.

But:

- Capital was tied up for 5 years

- Income was minimal

- No refinance or leverage optimization occurred

The IRR might fall around 6 to 7 percent.

That is where IRR reveals what traditional metrics hide.

A Story That Brings It Home

You are sitting with a client—let’s call him Mark.

Mark is deciding between two properties:

- A downtown condo

- A triplex outside the core

He says the condo feels safer.

You walk him through IRR.

You show him:

- The condo delivers a slower return over time

- The triplex requires more effort but returns capital faster

Mark leans back and says:

“So it’s not just about what I make—it’s about how fast I make it.”

That is the turning point.

How Realtors and Clients Can Put This Into Practice

Realtors

You can:

- Present properties with a performance lens

- Compare opportunities clearly

- Help clients make more informed decisions

Clients and Investors

You can:

- Compare multiple deals objectively

- Decide when to refinance or sell

- Avoid tying up capital in underperforming assets

Procedure to Apply IRR Thinking

First, map out all cash flows (investment, income, exit)

Second, estimate timing year by year

Third, calculate or model IRR

Fourth, compare across multiple opportunities

Fifth, select the opportunity that best aligns with your return and timeline objectives

Allen’s Final Thoughts

IRR is one of the key concepts that separates casual investors from serious ones.

It shifts the question from:

“Is this a good deal?”

To:

“Is this the best use of my money right now?”

That shift alone can change your entire trajectory.

You do not need to be highly technical to use IRR effectively. You simply need to start thinking in terms of time, efficiency, and capital movement.

How I Help You Put This Into Action

This is where I come in.

As a mortgage agent, I am not just here to secure financing. I am here to help you structure your deals intelligently.

I can help you:

- Align financing with your investment strategy

- Identify opportunities to improve your IRR through refinancing

- Structure deals for faster capital recovery

- Analyze whether a deal truly makes sense beyond surface numbers

- Collaborate with your realtor to position stronger investment opportunities

Because this is not just about buying real estate.

It is about building momentum, making your capital work efficiently, and ensuring that every dollar you invest is contributing to long-term growth.