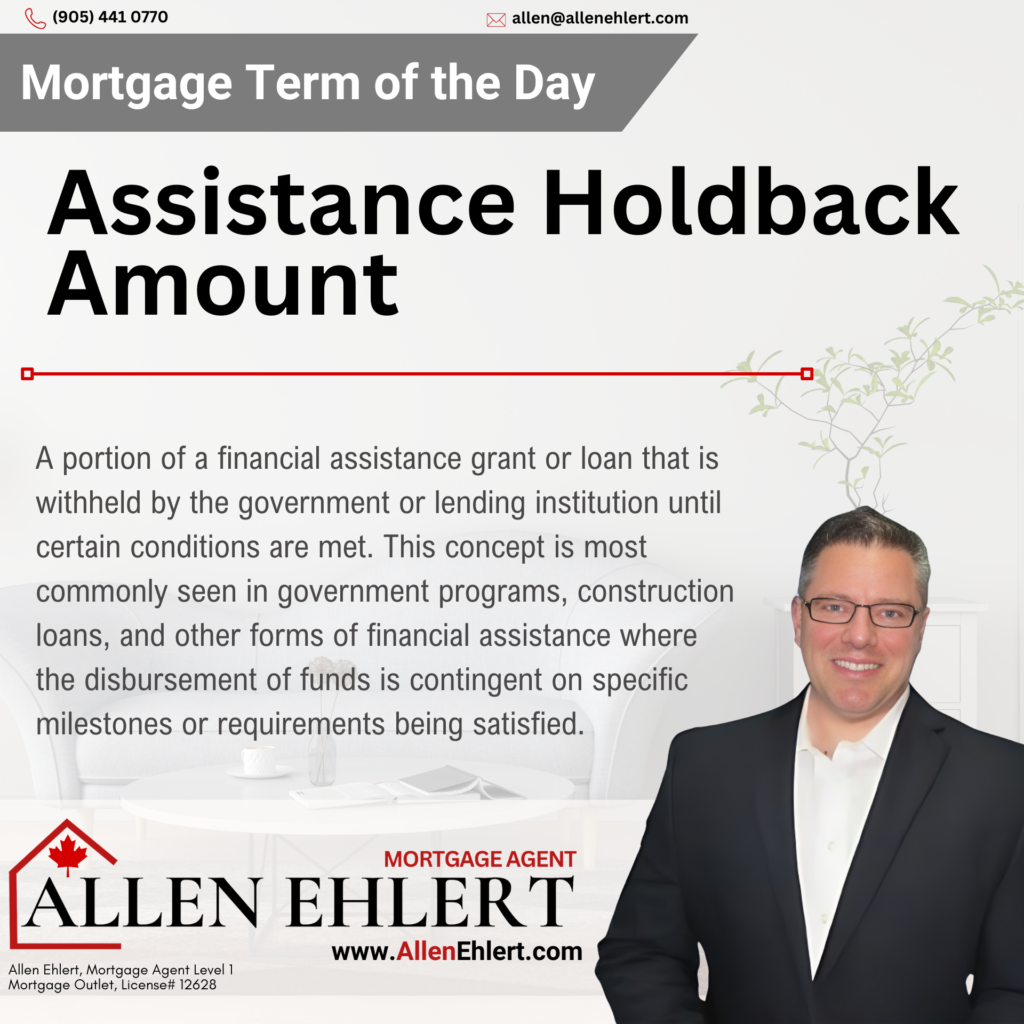

In Canada, the Assistance Holdback Amount typically refers to a portion of a financial assistance grant or loan that is withheld by the government or lending institution until certain conditions are met. This concept is most commonly seen in government programs, construction loans, and other forms of financial assistance where the disbursement of funds is contingent on specific milestones or requirements being satisfied.

Key Features of the Assistance Holdback Amount

Key Features of the Assistance Holdback Amount

Conditional Disbursement

The Assistance Holdback Amount is only released when the recipient meets certain predefined conditions. These conditions could include the completion of certain stages of a project, compliance with specific regulations, or the submission of required documentation.

Purpose of the Holdback

The holdback is intended to ensure that the funds are used appropriately and that the project or initiative for which the funds were allocated is progressing as planned. It acts as a safeguard for the entity providing the assistance.

Final Payment

Once the conditions are met, the holdback amount is released to the recipient. In the context of construction loans or similar scenarios, this often occurs after final inspections or the successful completion of the project.

Relation to Mortgages

The concept of an Assistance Holdback Amount can be related to mortgages in several ways, particularly in construction mortgages, home improvement loans, and government-assisted mortgage programs

Construction Mortgages

When building a home, lenders often provide a construction mortgage that is disbursed in stages as the project progresses. A portion of each disbursement may be held back as an Assistance Holdback Amount until specific construction milestones are completed and verified by an inspector. This ensures that the construction proceeds according to the agreed-upon plans and protects the lender’s investment.

Home Renovation Loans

Similar to construction mortgages, home renovation loans may involve an Assistance Holdback Amount. The lender might withhold a portion of the loan until the renovations are completed and meet certain standards or until all necessary permits and inspections have been approved. This prevents the borrower from receiving all funds upfront and ensures that the loan is used for its intended purpose.

Government Housing Assistance Programs

In government housing programs, such as those offering down payment assistance or grants for first-time homebuyers, an Assistance Holdback Amount might be applied. The government could withhold a portion of the assistance until the borrower fulfills all program requirements, such as completing a homebuyer education course or providing proof of occupancy. This ensures that the assistance is used to help qualified individuals achieve homeownership responsibly.

Impact on Cash Flow and Planning

For borrowers, understanding the terms of an Assistance Holdback Amount is crucial for cash flow management and planning. If a portion of the funds is withheld until specific conditions are met, the borrower needs to ensure they have sufficient resources to cover expenses during the interim period. This is especially important in construction projects, where delays in meeting conditions could affect the overall timeline and costs.

Ensuring Compliance

The Assistance Holdback Amount encourages compliance with the terms of the mortgage or assistance program. Borrowers and builders are incentivized to adhere to deadlines, regulations, and quality standards to ensure the timely release of the holdback funds.

Summary

The Assistance Holdback Amount in Canada refers to a portion of financial assistance or loan funds that are withheld until certain conditions are met. This concept is relevant in construction mortgages, home renovation loans, and government housing assistance programs, where funds are disbursed in stages to ensure that projects progress according to plan and that all requirements are fulfilled. Understanding the implications of an Assistance Holdback Amount is crucial for borrowers, as it affects cash flow, project timelines, and compliance with the terms of the loan or assistance program. In the context of mortgages, the holdback serves as a protective measure for lenders and ensures that the funds are used responsibly and effectively.