John and Mary Canuck have aspirations of improving their financial position, enhancing their future financial security, and generating wealth by using the existing equity in their home to purchase a new home to live in and rent out the home they presently live in.

John and Mary contacted a professional appraiser who appraised their existing home at $800,000. They have a fixed 5-year mortgage that is set to renew in 3 months with a balance of $300,000 and an attached HELOC that has no balance. They also have several lines of credit with other lenders that have no balance but are available in case of a rainy day. John and Mary believe their new house, which they will move into, will cost about $700,000. John is an electrician, and Mary is a nurse. Both have been in their permanent jobs for more than three years. Together, they make about $175,000 a year and have a good credit score.

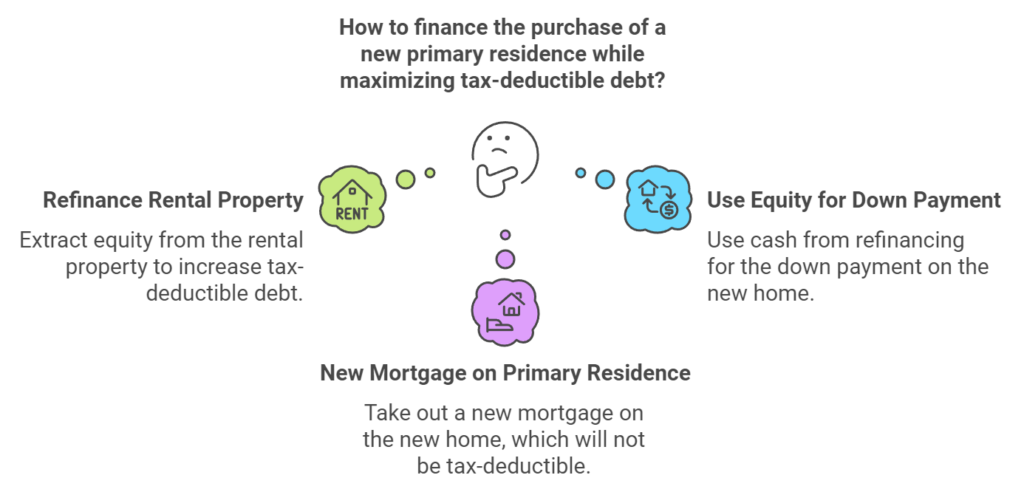

How can John and Mary, working with their Mortgage Agent, Allen Ehlert, to best structure their holdings in such a manner that the structure maximizes their tax deductions from interest expense from renting out my $800,000 residence and minimizes my taxes?

Key Goals:

- Maximize tax-deductible interest: Interest on money borrowed for income-producing properties (i.e., your rental property) is tax-deductible in Canada.

- Minimize personal non-deductible debt: The mortgage and any loans used to buy your new primary residence will not be tax-deductible, so minimizing non-deductible debt is crucial.

How to Maximize Tax-Deductible Interest for the Rental Property

Allen Ehlert advises John and Marry to restructure the financing of their current home (soon to be the rental property) to move as much debt as possible to that property, making the interest on that debt tax-deductible.

Step-by-Step Approach:

Step 1: Refinance the Current Property (Rental Property)

Since the Canuck’s current home will become a rental property, they want to refinance it to extract as much equity as possible, increasing the loan balance on this property. This allows them to convert a large portion of the mortgage into tax-deductible debt because the property will now generate rental income.

Current Situation:

- Appraised value: $800,000

- Mortgage balance: $300,000

- Available equity: Up to $640,000 (based on an 80% Loan-to-Value ratio).

Action: Refinance the mortgage up to 80% of the property’s value, which would be $640,000 (80% of $800,000). After paying off the existing $300,000 mortgage, the Canuck’s will have $340,000 in cash.

- Tax Deduction: The interest on the entire $640,000 mortgage (including the $300,000 original mortgage and the additional $340,000) becomes tax-deductible, as it’s associated with a rental property. This maximizes the interest deduction.

Step 2: Use the Equity for the Down Payment on the New Home

The $340,000 cash from the refinance of the rental property can be used toward the down payment on your new primary residence.

For a $700,000 purchase price on their new home, the Canuck’s would need a 20% down payment to avoid mortgage insurance, which is $140,000. The remaining $200,000 from the refinance can be used for other purposes or to pay down non-deductible debt on the new home.

Alternatively, depending on the Canuck’s risk tolerance, they may choose to purchase another rental property for $700,000, putting $140,000 down, and still having $60,000 in reserve. This additional property would provide another source of rental income, capital appreciation, and a vehicle for tax-deductible debt. The Canuck’s had no idea that this was possible!

Step 3: Take Out a New Mortgage on the New Primary Residence

After using the $340,000 (from the refinance) for the down payment, you will need a new mortgage for the remaining balance on the new home:

- New home price: $700,000

- Down payment: $340,000 (from the rental property refinance)

- New mortgage: $360,000

This mortgage on your new primary residence will not be tax-deductible because it’s used to purchase your personal home. However, this approach ensures that you’ve maximized your tax-deductible debt on the rental property and minimized the mortgage on the non-deductible side (your new home).

Alternatively, the Canuck’s could:

- Purchase New home price: $700,000

- Down payment: $140,000 (from the rental property refinance, 80% LTV)

- New mortgage: $560,000

- Purchase a second rental property price: $700,000

- Down payment: $140,000 (from the rental property refinance, 80% LTV)

- New mortgage: $360,000

Handling the HELOC

Since the Canuck’s have a HELOC attached to their current home with no balance, you have additional flexibility if needed.

After refinancing the mortgage, the HELOC remains available, and you could use it for future renovations or repairs on the rental property. Any interest in the HELOC used for rental-related expenses (e.g., renovations, upgrades, or repairs) would also be tax-deductible.

Allen Ehlert instructs the Canuck’s to be careful not to use the HELOC for personal expenses, as the interest on those funds would not be deductible. Allen Ehlert suggests the Canuck’s open a separate bank account to separate their personal expenses from their rental expenses.

Handling Other Lines of Credit

The Canucks have several lines of credit with no balance. If any of these lines of credit are used for personal expenses, the interest on them will not be deductible. If they are used for expenses related to the rental property, the interest may be deductible. It’s best to keep rental-related and personal expenses separate for clarity and proper tax reporting.

Tax Deduction Optimization

Once the Canuck’s current home becomes a rental property, Allen Ehlert suggests the Canuck’s:

- Keep all receipts and documents for expenses related to the rental property (e.g., maintenance, property management, and repairs).

- Track the interest expense on the mortgage and HELOC related to the rental property.

- Deduct all eligible expenses from the rental income to reduce your taxable income from the rental.

Potential Risks and Considerations

Beware of over-leveraging: Ensure that you’re comfortable with the increased debt load, as refinancing to the maximum 80% LTV will increase your overall liabilities. Make sure you can handle the mortgage payments, especially on the rental property, if it experiences vacancies.

Beware of interest rate changes: Be aware of potential increases in interest rates, especially if you’re refinancing or using a HELOC, which usually comes with a variable rate. Rising rates could increase your carrying costs.

Summary of the Strategy

John and Mary Canuck want to improve their financial security and generate wealth by leveraging the equity in their current home. They plan to move into a new home valued at approximately $700,000 and rent out their existing home, which was appraised at $800,000. They have a $300,000 mortgage balance on their current home, with an attached HELOC that has no balance, and several unused lines of credit for emergencies. Both John, an electrician, and Mary, a nurse, have stable jobs and a combined annual income of $175,000, with good credit scores.

Allen Ehlert, their mortgage agent, advised them to structure their real estate holdings to maximize tax deductions on interest expenses related to renting out their current home while minimizing taxes. Allen suggests two possible strategies:

- Using 80% Equity from the Primary Residence: John and Mary could take 80% of the equity out of their $800,000 home (about $640,000), keeping $140,000 to use as a down payment for a new $700,000 home where they would live, and use another $140,000 as a down payment on an investment property (also valued at $700,000), which they would rent out.

- Tax Considerations: By doing so, they can maximize their tax-deductible interest expenses related to the rental property (the current residence they will rent out and/or the additional investment property). Structuring the mortgage and HELOC effectively could allow them to deduct the interest on the portion of the loans tied to the rental properties, reducing their taxable income.

This strategy, if executed correctly, could help John and Mary achieve their goal of building wealth through real estate while minimizing their tax burden. Allen will help them work through the financing and tax implications to create the most advantageous structure for their situation.

Does the Alternative Structure Support Debt Service Ratios?

Let’s calculate whether the Canuck’s $175,000 income would support the debt service ratios (GDS and TDS) required by lenders, based on the proposed mortgages for the new primary residence and the two rental properties.

Key Lender Ratios

Gross Debt Service (GDS) Ratio: This is the percentage of their gross income that goes toward housing costs (mortgage payments, property taxes, heating, and 50% of condo fees, if applicable) for their primary residence. Lenders typically want to see a GDS ratio below 32-39%, depending on the lender.

Total Debt Service (TDS) Ratio: This includes all housing costs plus other debt obligations (such as mortgages for rental properties, credit card payments, car loans, and other liabilities). The TDS ratio should generally be below 40-44%, though some lenders might be flexible if you have strong financials or rental income.

Assumptions for the Scenario

- Mortgage amount for the new primary residence: $560,000

- Mortgage amount for the two rental properties: $1,200,000 ($640,000 for the existing home + $560,000 for the investment property)

- Interest rate: Assume a 5% interest rate for calculation purposes (present rates are lower, 5% chosen to simplify the math)

- Amortization period: 25 years (could be stretched to 30)

- Property taxes and utilities: Estimate $8,000 annually for their new primary residence

- Rental income: Assume $3,500/month for their existing home rental and $3,500/month for the new rental property (reasonable rental rates in the current market)

Calculating Mortgage Payments

- Monthly mortgage payment for the new primary residence: $3,273.70

- Monthly mortgage payment for rental property 1 (current home): $3,741.38

- Monthly mortgage payment for rental property 2 (new investment): $3,273.70

- Total monthly mortgage payments (all properties): $10,288.78

- Monthly rental income from both properties: $7,000

- Monthly property taxes and utilities for the new primary residence: $666.67

Debt Service Ratios

After calculations, the following are the GDS and TDS ratios:

- Gross Debt Service (GDS) Ratio: 27.02%

- Total Debt Service (TDS) Ratio: 22.55%

Conclusion

- GDS ratio: 27.02% (well below the 32-39% limit).

- TDS ratio: 22.55% (below the 40-44% limit).

Based on this calculation, the Canuck’s $175,000 income should comfortably support the required debt service ratios, even after taking on the additional mortgages for the second rental property and the new primary residence. They are well within the acceptable range for most lenders.

Wealth Appreciation

Over the past 20 years, the average house in Canada has appreciated 6.1%. Before refinancing, the Canucks wealth was growing by $48,800 (6.1% X $800,000) a year. Under Allen Ehlert’s structure, the Canucks may see their wealth grow by $134,200 a year. This clearly demonstrates the power of owning real estate in Canada.

Increased Income

After refinancing, the Canucks with 2 rental properties can generate $84,000 in income. Before refinancing, the Canucks earned no income from owning a house.

Tax Reduction

The Canucks can deduct the following interest expenses from their taxes:

- Interest expense on the first rental property (existing home): $32,000

- Interest expense on the second rental property (new investment): $28,000

- Total annual interest expense deduction: $60,000

This amount can be deducted from their rental income or other taxable income, reducing their overall tax liability. It’s important that they maintain proper documentation and records of these expenses to support the tax deduction.

Summary

By working with Allen Ehlert, John and Mary can achieve their aspirations of improving their financial position, enhancing their future financial security, and generating wealth in a way they never knew was possible. By using the existing equity in their home, the Canucks can purchase not just a new home to live in and another to rent out but two homes to rent out, substantially increasing their rental income, maximizing their deductions, reducing their taxes payable, and doubling their capital appreciation.