Condotels, or condo/hotel hybrids, have piqued the interest of many Canadians, particularly those seeking a flexible investment opportunity. These unique properties offer the ability to enjoy personal use while generating short-term rental income. Whether you’re a real estate investor, a realtor advising clients, or someone exploring adaptable living solutions, the allure of owning a property that can double as a vacation home and a rental unit is undeniable.

However, there’s a catch. Canadian lenders generally shy away from financing condotels, making it challenging for potential buyers to secure a mortgage on these properties. This hesitancy raises critical questions about the viability of condotels as an investment and how to navigate the financing landscape.

Why Condotels Are an Attractive Investment

Why Lenders Hesitate to Provide Mortgages on Condotels

Examples of Condotel Financing Challenges

How to Secure Mortgage Financing for a Condotel

Next Steps: Your Guide to Condotel Investment

What is a Condotel?

A condo/hotel hybrid, often called a condotel, is a building that combines features of both residential condominiums and hotels. It allows individual buyers to purchase units in a building that is operated and managed like a hotel.

Some examples of condotels include

- One King West Hotel & Residences (Toronto)

- Residences of Yorkville Plaza (Toronto)

- Tall Ships Landing Coastal Resort (Brockville)

- Victoria Regent Waterfront Hotel & Suites (Victoria)

- Royal Dalhousie (Quebec City)

Condotel Key Features

Some key features of condo/hotel hybrids include

- Dual Purpose

- Hotel-Like Amenities

- Management and Rental Program

- Ownership Restrictions

Dual Purpose

Condotel units are sold as individual condominiums, but the building operates as a hotel, offering short-term rentals to guests when units are not in use by the owners.

Owners can use the units as vacation properties for personal use and generate rental income by allowing the hotel management to rent them out.

Such dual-purpose arrangements can be particularly attractive to corporations that have executives travelling regularly and need to provide regular short-term housing. For example, some consulting firms may even have office space in such buildings so their professionals can work and live in the same building as their business is national or global in nature. Such dual-purpose arrangements can be very cost-effective.

Hotel-Like Amenities

Condotels typically offer amenities found in hotels, such as

- Housekeeping services

- Room service

- Business services

- Concierge service

- Restaurants, spas, and pools

These amenities make them attractive as short-term rental properties and increase the potential for rental income.

Management and Rental Program

The building is typically managed by a hotel operator or management company, which handles bookings, maintenance, and guest services. This outsources a lot of the tasks and makes owning such a unit turnkey and convenient.

Owners often have the option to enrol their units in a rental program, where the management company rents out the units when not in use by the owners. The cost of the rental program is a tax write-off against the rental income.

Rental income is usually split between the unit owner and the management company, with percentages varying based on the contract.

Ownership Restrictions

Some condotels impose restrictions on how often owners can stay in their units each year to prioritize short-term rentals.

Others may have restrictions on how the units can be rented out (e.g., minimum stay requirements).

Why Condotels Are an Attractive Investment

Before diving into the financing challenges, let’s first understand why condotels are a popular investment choice

- Adaptable Living

- Premium Rental Locations

- Low Maintenance

Adaptable Living

Owners can enjoy the unit for personal use when desired and rent it out when not in residence, offering maximum flexibility.

Condotels allow owners to generate short-term rental income without the hassles often associated with long-term tenants and the Landlord and Tenant Board (LTB).

Premium Rental Locations

Condotels are typically located in high-demand areas, such as downtown cores, resort destinations, and tourist hotspots, making them attractive for short-term renters looking for convenience and amenities.

The managed services offered by condotels (e.g., housekeeping, concierge) enhance the guest experience, justifying higher rental rates.

Low Maintenance

Most condotels offer hotel-like services, such as property management, cleaning, and maintenance, making them ideal for owners who prefer a more hands-off approach.

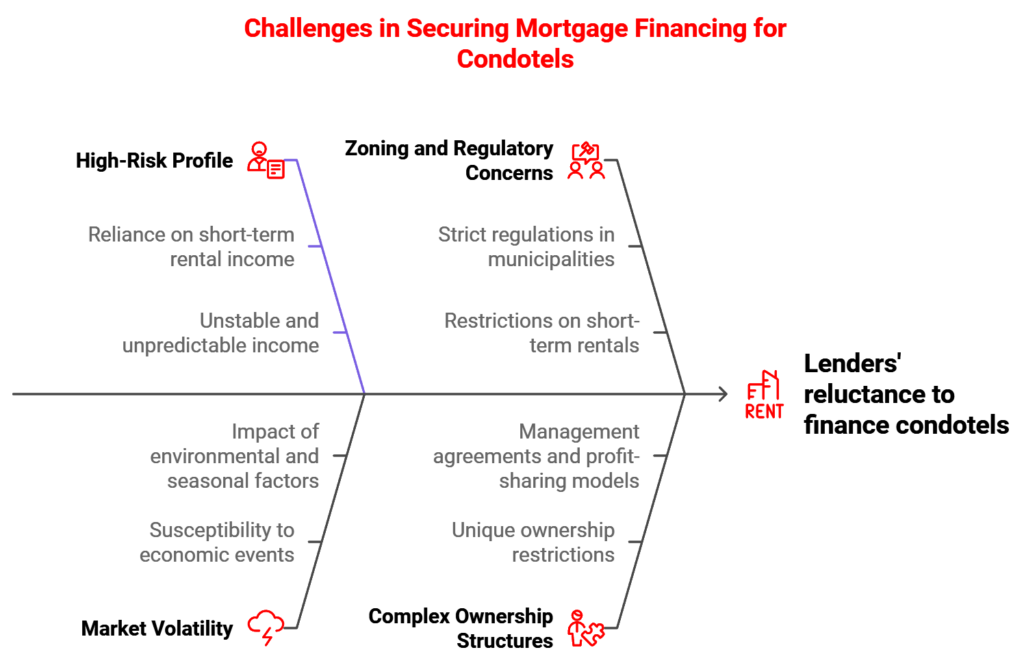

Why Lenders Hesitate to Provide Mortgages on Condotels

Despite their appeal, condotels face significant barriers when it comes to securing mortgage financing in Canada. Here’s why lenders are hesitant

- High Risk Profile

- Market Volatility

- Zoning and Regulatory Concerns

- Complex Ownership Structures

High-Risk Profile

Lenders view condotels as high-risk investments. Their reliance on short-term rental income makes them vulnerable to fluctuations in the tourism market, economic downturns, and seasonal variations.

The income from condotels is often unstable and unpredictable, posing a greater risk to lenders compared to traditional residential mortgages that rely on consistent, longer-term rental income.

Market Volatility

Condotels are often located in areas with significant tourism dependency, making them susceptible to market volatility.

Economic events, like the COVID-19 pandemic, environmental events, and even bad weather (like a warm winter near a ski area), can drastically reduce short-term rental demand, making it difficult for owners to generate income and cover mortgage payments.

Zoning and Regulatory Concerns

Some municipalities have strict regulations on short-term rentals, further complicating the financial risk assessment for lenders.

For example, cities like Toronto and Vancouver have implemented regulations that restrict or limit short-term rentals, potentially affecting an owner’s ability to generate consistent income from a condotel.

Complex Ownership Structures

Condotels often have unique ownership structures, with restrictions on usage, management agreements, and potential profit-sharing models with the hotel operator.

These complexities make it harder for lenders to assess the property’s value and potential for appreciation, further increasing their reluctance to lend on condotels.

Examples of Condotel Financing Challenges

The following are some examples of developments that have provided some challenges to buyers regarding obtaining mortgage financing

Example 1 Toronto’s One King West

Known for its prime downtown location, One King West operates as both a hotel and a condominium. While the building offers luxurious units and high rental potential, many buyers have struggled to secure traditional financing due to the building’s condotel status.

Some buyers had to turn to alternative lenders or rely on cash purchases, facing higher interest rates and fees.

Example 2 Whistler’s Legends Condotel

Located in the heart of Whistler, Legends offers a ski-in/ski-out experience. However, financing challenges have deterred many potential investors from purchasing units, as major banks and A lenders are reluctant to finance properties primarily driven by seasonal tourism.

How to Secure Mortgage Financing for a Condotel

If you’re still interested in pursuing a condotel purchase, here are actionable steps to improve your chances of securing financing

Explore Alternative Lenders

Consider B lenders, mortgage investment corporations (MICs), or private lenders who have more flexible criteria and are willing to finance condotels.

Be prepared for higher interest rates, shorter loan terms, and larger down payment requirements (often 25% or more).

Build a Stronger Financial Profile

Boost your credit score and reduce debt-to-income ratios to improve your attractiveness as a borrower.

Prepare detailed documentation of potential rental income, projected expenses, and contingency plans to present to lenders.

Negotiate Rental Agreements Carefully

Review any existing agreements with the hotel management company and ensure they don’t restrict your ability to rent out the unit as needed.

Consider Cash Purchases or Leveraging Home Equity

If feasible, purchasing with cash or leveraging a home equity line of credit (HELOC) on another property can help bypass the need for a traditional mortgage.

Consult Real Estate and Mortgage Professionals

Work with experienced realtors, mortgage agents, and legal experts familiar with condotels to navigate the complexities of purchasing and financing these properties.

Read More

- Appraisal Nightmare

- Condominium Conditions

- Understanding Condo Reserve Funds

- Avoid Blacklisted Condos

- Lenders Don’t Like Condotels

- Do You Need Title Insurance for a Condo?

- Understanding Condominium Fees

Final Analysis: Pros and Cons

Pros

- Adaptable living for personal use and rental income.

- Prime locations and attractive amenities.

- Hands-off management compared to traditional rental properties.

Cons

- Higher financing hurdles and potential for higher interest rates.

- Income volatility is tied to tourism trends and regulatory changes.

- Restrictions on personal use and rental agreements.

Next Steps: Your Guide to Condotel Investment

If you’re considering a condotel purchase, here’s what to do next

- Assess your financial readiness and be realistic about potential rental income.

- Research local regulations and ensure the condotel aligns with your investment goals.

- Contact Allen Ehlert who specializes in financing alternative properties and can connect you with realtors experienced in condotels.

Summary

While condotels offer unique advantages, their financing challenges can be daunting. It’s crucial to weigh the pros and cons, explore alternative lenders, and be prepared for potential risks. By understanding the nuances of condotel financing, you’ll be better equipped to make informed investment decisions in this dynamic segment of the Canadian real estate market.