When a person in Canada wishes to purchase a condominium, they put in their offer to purchase a condition to enable themselves, their lawyer, their realtor, and their mortgage agent and lender the opportunity to review detailed information about the financial and legal health of the condominium corporation. As real estate is a provincial jurisdiction in Canada, the name of this condition differs depending on which province you are in:

- British Columbia: Form B: Information Certificate (governed by the Strata Property Act)

- Alberta: Estoppel Certificate (governed by the Condominium Property Act)

- Quebe: Syndicate of Co-Ownership Documents (governed by the Civil Code of Quebec)

- Manitoba: Disclosure Certificate (governed by the Condominium Act of Manitoba)

- Saskatchewan: Information Statement (governed by Condominium Property Act)

- Nova Scotia: Certificate of Financial Standing (governed by the Condominium Act of Nova Scotia)

- Ontario: Status Certificate (governed by Condominium Act of 1998)

However, to a greater or lesser extent, these documents support the condition that a buyer needs to know the condition and status of a condominium corporation before making a firm offer on the purchase of a condominium. I’ll assume you are in Ontario.

What is a Condominium Status Certificate?

Sample: Condition of Status Certificate

Why Is the Condominium Status Certificate Important?

Key Elements of the Condition of Status Certificate

What is a Condominium?

A condominium is a type of property ownership governed by the different condominium acts of the province (see list above). It combines individual ownership of a specific unit (e.g., an apartment or townhouse) with shared ownership of common elements (e.g., hallways, elevators, recreational facilities).

Here’s a breakdown of the key aspects of condominiums in Ontario:

Key Features of a Condominium

Unit Ownership: The buyer owns their specific unit outright. For example, an apartment in a high-rise building or a townhouse in a row of similar homes.

Ownership includes exclusive rights to use and live in the unit.

Common Elements: Owners share ownership of the building’s common elements, such as:

- Hallways, lobbies, and elevators.

- Parking lots and driveways.

- Recreational facilities (e.g., gyms, pools, gardens).

- Mechanical and structural systems (e.g., HVAC, roofs, plumbing).

These areas are maintained collectively through monthly condo fees.

Condo Fees: Owners pay monthly maintenance fees to cover:

- Regular upkeep of common elements.

- Contributions to a reserve fund for major repairs or replacements.

- Utilities or amenities, if included in the condo’s budget.

Condo Corporation: Each condominium is managed by a condominium corporation, a legal entity responsible for:

- Managing the property’s operations.

- Enforcing rules and bylaws.

- Collecting fees and maintaining the reserve fund (See: Understanding Reserve Funds)

The corporation is overseen by a board of directors, elected by unit owners.

Rules and Bylaws: Condo owners are subject to rules and bylaws set by the condo corporation. These rules govern how units and common elements can be used (e.g., restrictions on pets, noise levels, and short-term rentals).

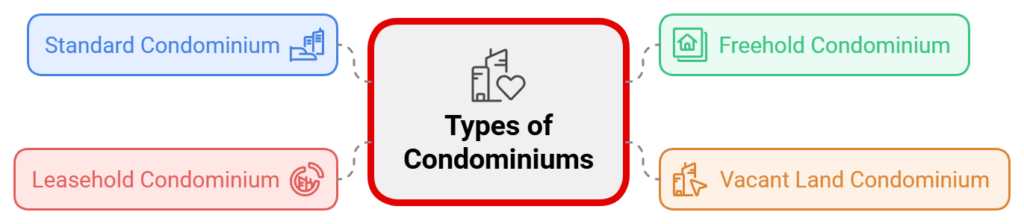

Types of Condominiums:

Standard Condominium: The most common type, where owners hold full ownership of their unit and shared ownership of common elements.

Freehold Condominium: Owners own the unit and the land it’s on (common in townhouse developments).

Vacant Land Condominium: Owners purchase a lot of land within a condo corporation and may build their own home.

Leasehold Condominium: Units are owned, but the land is leased from a third party (e.g., for a fixed term).

What is a Condominium Status Certificate?

A status certificate is a document that provides detailed information about the financial and legal health of the condominium corporation. It includes:

- The unit’s financial obligations (e.g., monthly maintenance fees, special assessments).

- Information about the reserve fund (used for major repairs and replacements).

- Current legal issues or claims involving the condo corporation.

- Rules, bylaws, and restrictions affecting unit owners.

Why Is the Condominium Status Certificate Important?

The status certificate is important as it reveals:

- The financial health of the condominium

- Any legal disputes or ongoing litigation

- Rules and restrictions

- Reg flags

Transparency on Financial Health

The certificate reveals if the condominium corporation has sufficient funds in the reserve fund or if there are potential liabilities requiring special assessments, which would increase monthly costs for the buyer.

Legal Standing

It discloses ongoing legal disputes that could pose risks to the buyer or increase costs for the condominium corporation.

Rules and Restrictions

The buyer can learn about restrictions (e.g., pet rules, rental policies) that might affect their use of the property.

Red Flags

The condition allows the buyer’s lawyer and/or real estate agent to review the document for potential red flags. If significant issues are found, the buyer can negotiate terms, request repairs, or walk away from the deal without penalty.

Sample: Condition of Status Certificate

Here’s an example of how a Status Certificate Condition might be written in an Agreement of Purchase and Sale (APS) for a condominium in Ontario:

“This Agreement is conditional upon the Buyer’s solicitor reviewing the status certificate, including the accompanying declaration, by-laws, budget, rules, and reserve fund study, and being satisfied with its terms and the financial condition of the condominium corporation. The Seller agrees to request, at the Seller’s expense, a current status certificate from the condominium corporation and deliver it, along with all accompanying documents, to the Buyer or the Buyer’s solicitor within 10 business days from the acceptance of this Agreement.

The Buyer shall have a further 3 business days from receipt of the status certificate and accompanying documents to waive this condition by providing written notice to the Seller or the Seller’s representative. If such written notice is not provided within the time specified, this Agreement shall become null and void, and all deposit monies shall be returned to the Buyer without deduction or interest.

This condition is included for the sole benefit of the Buyer and may be waived at the Buyer’s discretion by written notice.”

Key Elements of the Condition of Status Certificate

- Buyer’s Solicitor Review: Explicitly states that the condition depends on the lawyer’s satisfaction with the certificate and documents.

- Seller’s Obligation: Requires the seller to request and pay for the status certificate.

- Timeline: Provides clear deadlines for obtaining the certificate and for the buyer’s review and decision.

- Null and Void: Protects the buyer by allowing them to walk away if the condition is not fulfilled or waived.

- Sole Benefit of the Buyer: Ensures the condition cannot be overridden without the buyer’s consent.

This condition ensures that the buyer is protected and has ample opportunity to verify the condominium’s financial and legal health before finalizing the purchase.

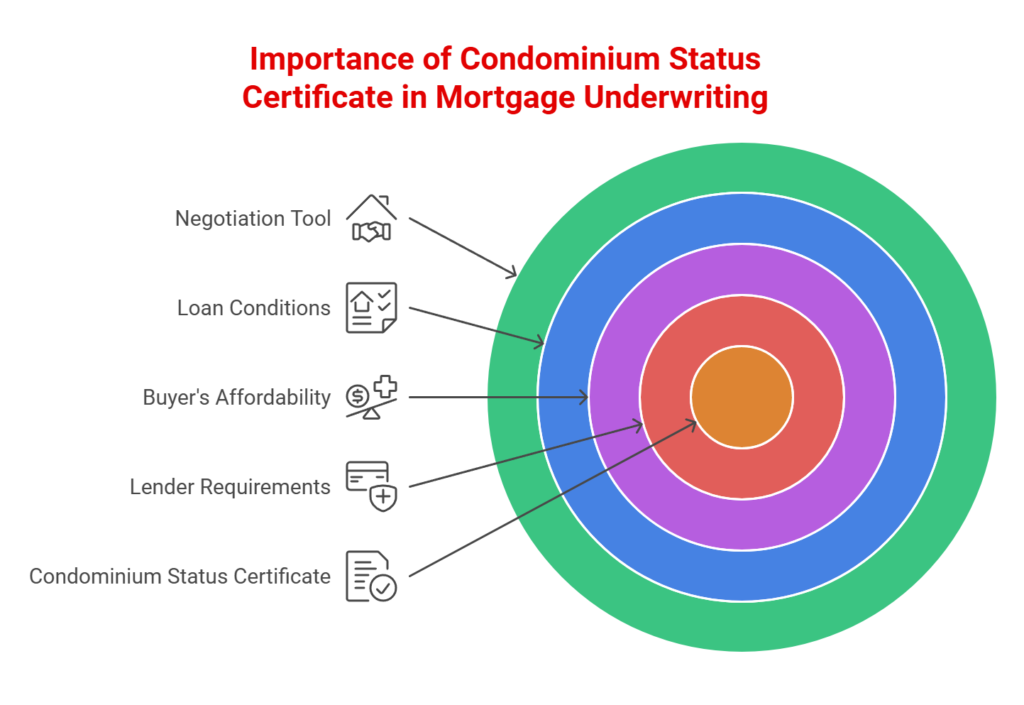

Mortgage Agent Perspective

From a mortgage agent’s perspective, a condominium status certificate is a critical document required to underwrite a mortgage on a condominium for the following reasons:

- Lender requirements

- Buyer’s Affordability

- Loan Conditions

- Negotiation Tool

Lender Requirements

Mortgage lenders often require the status certificate to ensure the condominium corporation is financially stable. A poorly managed condominium could reduce the property’s value or make it harder to resell, increasing the lender’s risk.

If the status certificate reveals financial instability (e.g., underfunded reserve fund or pending litigation), the lender might decline the mortgage or impose stricter terms.

Buyer’s Affordability

If the status certificate highlights potential increases in maintenance fees or special assessments, the buyer’s debt service ratios may change, affecting their mortgage qualification.

Loan Conditions

Some lenders might add conditions to the mortgage approval requiring a review of the status certificate before fully committing to financing.

Negotiation Tool

Buyers can use findings from the status certificate to renegotiate the purchase price or ask the seller to address certain issues before closing.

Best Practices

- Include the Condition: Always include a status certificate condition in your offer to purchase a condo.

- Professional Review: Have a real estate lawyer review the status certificate.

- Timeframe: Ensure you have sufficient time (typically 10 days) to review the certificate before the condition expires.

By understanding the importance of the Status Certificate Condition and ensuring it is handled correctly, buyers can protect their financial interests and make informed decisions. For mortgage agents, it is essential to educate clients about the implications of financing to ensure a smooth transaction.

Black Listed Condos

A blacklisted condo is a condominium that certain mortgage lenders have categorized as high-risk and are unwilling to finance. Lenders maintain these lists to protect themselves from potential financial losses, as blacklisted condos typically face issues that could affect their value or marketability. While lenders’ lists are private and vary, the reasons for blacklisting tend to be consistent.

Key Reasons for a Condo to Be Blacklisted

Understanding why a condo may end up on a blacklist is crucial, as it can affect your decision to buy or sell. Here are the primary reasons:

- Financial Instability of the Condo Corporation

- Structural or Maintenance Problems

- Pending Legal Disputes

- Insurance Challenges

- High Proportion of Investor-Owned Units

Financial Instability of the Condo Corporation

Lenders are wary of condo corporations with insufficient reserve funds, high debt, or poor financial management.

Read More

- Appraisal Nightmare

- Condominium Conditions

- Understanding Condo Reserve Funds

- Avoid Blacklisted Condos

- Lenders Don’t Like Condotels

- Do You Need Title Insurance for a Condo?

- Understanding Condominium Fees

If the condo’s reserve fund—a pool of money set aside for major repairs and maintenance—is low, lenders perceive it as a red flag.

High delinquency rates among unit owners (e.g., unpaid maintenance fees) can also indicate financial instability and make a condo more likely to be blacklisted.

Read more: Avoid Blacklisted Condos

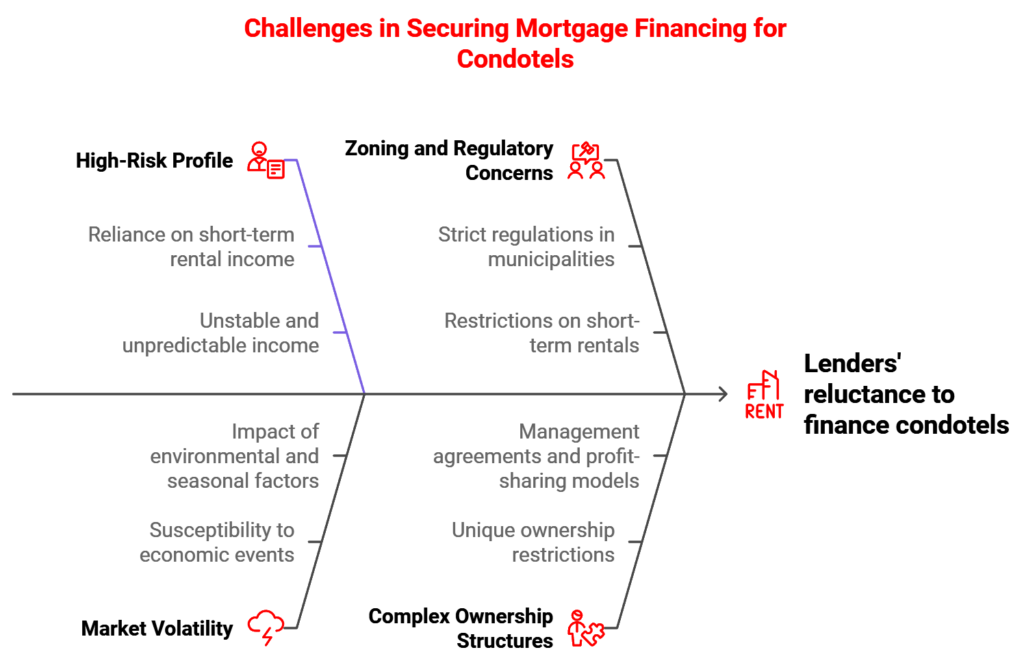

Lenders Don’t Like Condotels

Condotels, or condo/hotel hybrids, have piqued the interest of many Canadians, particularly those seeking a flexible investment opportunity. These unique properties offer the ability to enjoy personal use while generating short-term rental income. Whether you’re a real estate investor, a realtor advising clients, or someone exploring adaptable living solutions, the allure of owning a property that can double as a vacation home and a rental unit is undeniable.

However, there’s a catch. Canadian lenders generally shy away from financing condotels, making it challenging for potential buyers to secure a mortgage on these properties. This hesitancy raises critical questions about the viability of condotels as an investment and how to navigate the financing landscape.

Read more: Lenders Don’t Like Condotels

Read More:

- Real Estate Conditions

- Financing Condition

- Home Inspection Condition

- Sale of Current Property Condition

- Status Certificate Condition

- Appraisal Condition

Summary

Understanding condominium conditions and the role of a condominium status certificate is essential, particularly from a mortgage financing perspective. These documents provide critical insights into the financial and legal health of a condominium corporation, which directly impacts a lender’s willingness to approve financing. Issues such as insufficient reserve funds, pending legal disputes, or high delinquency rates among unit owners can pose significant risks to both buyers and lenders, potentially leading to higher financing conditions or outright loan denials. By including a status certificate condition in the purchase offer and ensuring a thorough review by legal and mortgage professionals, buyers can mitigate risks and safeguard their financing options. For mortgage agents, the status certificate is a valuable tool to educate clients and ensure the condominium meets lender requirements, creating a smoother path to securing financing and completing the transaction.