Financial planners generally advise spending no more than 28% to 30% of your gross monthly income on housing. This guideline is known as the “front-end ratio” and primarily covers housing expenses like mortgage payments, property taxes, homeowner’s insurance, and repairs and maintenance. Staying within this range helps ensure you have enough budget for other monthly expenses, savings, and investments.

However, the overall recommendation is to keep total debt payments, including housing and other debts like car loans and credit cards (known as the “back-end ratio”), under 36% of your gross income. These are just guidelines, and individual financial circumstances can influence these percentages. Financial planners often tailor advice based on factors such as financial goals, job stability, and other personal financial obligations.

Spending more than Recommended

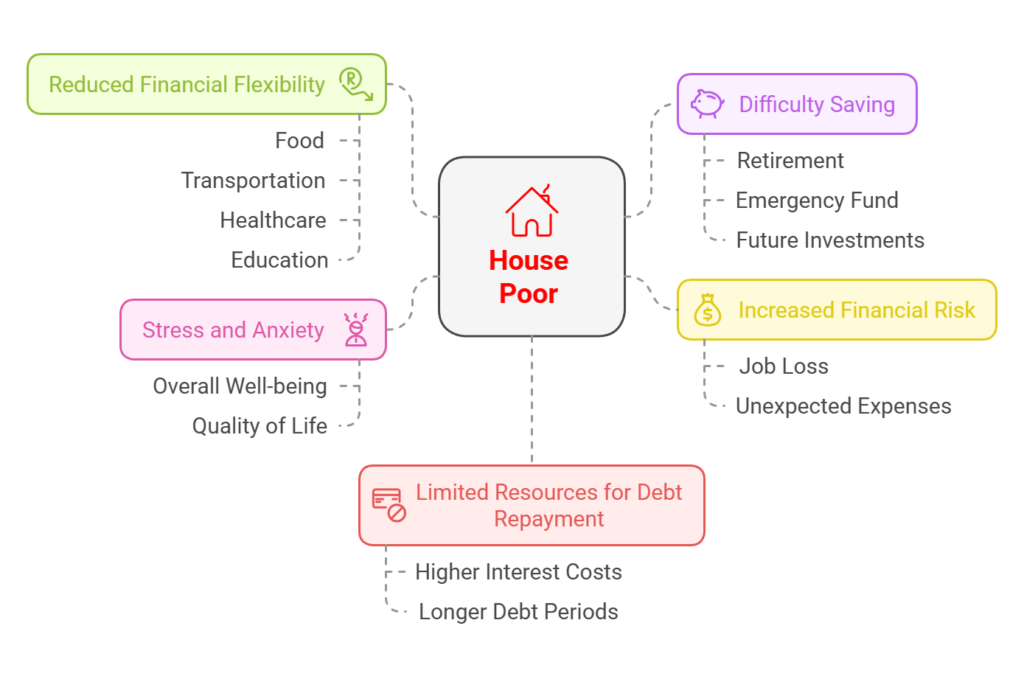

Spending more than 30% of your gross income on housing is often referred to as being “house poor,” and it can lead to several financial challenges:

- Reduced Financial Flexibility: Overspending on housing costs can limit your ability to cover other necessary expenses, such as food, transportation, healthcare, and education.

- Difficulty Saving: If a large portion of your income is dedicated to housing, it may be harder to save for other goals, such as retirement, an emergency fund, or future investments.

- Increased Financial Risk: Spending a significant amount on housing increases your vulnerability to financial setbacks, such as job loss or unexpected expenses. Without sufficient discretionary income, even minor financial disruptions can lead to serious issues, like debt accumulation or the inability to pay for basic needs.

- Stress and Anxiety: Financial strain caused by high housing costs can lead to increased stress and anxiety, affecting overall well-being and quality of life.

- Limited Resources for Debt Repayment: If too much income goes towards housing, there might be less available to pay down existing debts, potentially leading to higher interest costs and longer debt periods.

Financial planners typically advise maintaining housing costs within a manageable proportion of income to ensure overall financial health and stability. This balance helps safeguard against potential financial stress and allows for better management of total financial obligations.

Calculating Housing Cost as Percentage of Income

Calculating housing cost as a percentage of income is a common method used to assess housing affordability. This calculation helps determine how much of a person’s income is spent on housing-related expenses, and it is often used by financial advisors, economists, and policy makers. Here’s how you can do it:

- Determine Total Monthly Housing Cost: Add up all monthly costs associated with housing. This typically includes:

- Mortgage payments (principle, interest, and protection insurance like MPP)

- Property taxes

- House insurance

- Utilities

- Maintenance and Repairs

- Any other regular monthly fees directly related to the housing (eg. condo fees)

- Calculate Total Monthly Income: Sum up all sources of income you receive in a month. This includes:

- Gross monthly salary (before taxes)

- Business income

- Investment income

- Side hustle

- Any other consistent monthly income (e.g., alimony, child support, government benefits)

- Use the Formula: Divide the total monthly housing cost by the total monthly income and then multiply by 100 to convert the figure into a percentage.

Housing Cost Percentage = (Total Monthly Housing Cost / Total Monthly Income) × 100

Example

Suppose your monthly mortgage payment is $5,500, property taxes are $500, homeowners insurance is $100, and utilities cost $200. Your total monthly housing cost would be:

$2,500 + $500 + $100 + $200 = $3,300

If your gross monthly income is $9,000, then your housing cost as a percentage of income would be:

($3,300 / $9,000) × 100 = 37%

This result means that 37% of your income is spent on housing. Generally, a housing cost percentage of 30% or less is considered affordable, whereas figures higher than that might indicate financial stress related to housing costs. Unfortunately, for most first time home owners, they need to build up equity in their home before they can get their housing costs to drop below 30% of income.