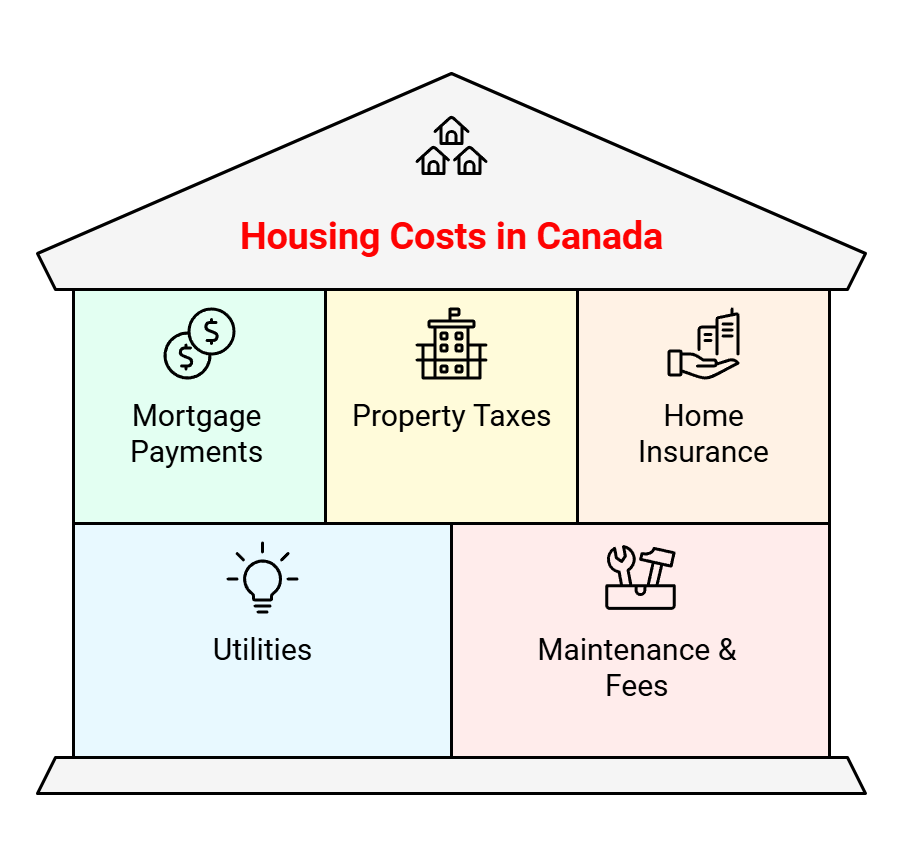

To ensure you do not spend more than 30% of your income on housing costs, it’s important to understand how to calculate your housing expenses. In Canada, housing costs typically include:

- Mortgage Payments: The monthly amount paid towards the mortgage principal, interest, mortgage default insurance (if applicable), and protection.

- Property taxes: Paid to the local municipality, calculated as a percentage of the property’s assessed value (actually, this is not true 😉 )

- Home Insurance: Covers potential damage to the property.

- Utilities: Electricity, gas, water, and other services (rural)

- Maintenance & Repairs: Improvements and repairs to home and housing systems (How to Calculate Maintenance & Repairs)

- Condominium Fees (if applicable): Fees paid by condo owners for building maintenance and services.

How to Calculate Repairs and Maintenance

Step-by-Step Calculation

- Calculate Monthly Income:

To find out what 30% of your income is, you first need to calculate your monthly income from your annual income. If the median family income is $115,000 before taxes, the monthly pre-tax income would be:

Monthly Income = $115,000 / 12 = $9,583.33

- Calculate 30% of Monthly Income:

30% of Monthly Income = 0.30 × $9,583.33 = $2,87530

This figure represents the maximum amount that should be spent on housing costs according to the 30% rule.

- Determine monthly Housing Costs

This step is usually the most difficult because you have to pull together information from multiple sources:

Understanding Mortgage Costs: Principle, Interest, and Protection

When You Need Mortgage Default Insurance

Ensure you annualize costs before determining a monthly average. Feel free to use estimates as values are subject to change and inflation.

- Calculate Total Housing Cost

Housing Percentage of Income = Monthly Housing Costs / Monthly Income

Ideally, you should attempt not spend more than 30% of your income on housing costs. Your housing costs as a percentage of income is what is used to determine your gross debt service ratio (GDS). When mortgage underwriters calculate your GDS, while below 30% is ideal, you still qualify for a mortgage with a prime lender if your GDS is below 39%. If you your GDS is higher, up to 50%, you still can get a mortgage through an alternative lender.

Ensuring You Do Not Exceed 30%:

- Budgeting: Use this figure as a cap for your total housing expenses. Track your expenses monthly to ensure they do not exceed this amount.

- Mortgage Pre-Approval: When looking for a home, getting pre-approved for a mortgage can help ensure that your mortgage payments align with your budget limitations.

- Cost Cutting: If your current housing costs exceed 30%, consider ways to reduce them, such as refinancing your mortgage, appealing property tax assessments, or reducing utility costs.

Example:

Let’s consider an example where a family with a median income of $115,000 is looking to purchase a home. Here’s how they might budget:

- Mortgage Payment: $1,800 per month

- Property Taxes: $500 per month

- Home Insurance: $150 per month

- Utilities: $200 per month

- Maintenance & Repairs: $200 per month, or

- Condominium Fees (if applicable): $200 per month

Total Housing Costs: $2,850

This total is under the $2,875 limit calculated earlier, fitting within the 30% rule. This approach helps ensure that housing costs remain manageable relative to income, reducing the risk of financial stress.

How to Calculate Repairs and Maintenance

It’s commonly recommended that homeowners budget between 1% and 3% of their home’s purchase price annually for repairs and maintenance. Unfortunately, this guideline was started in the 1980s and hasn’t been updated since. A home in Ontario that could be purchased in the 1980s for $64,000 now costs over $1 million dollars. So, to suggest that Canadians should spend 1% to 3% of their home’s purchase price or $10,000 to $30,000 annually for repairs and maintenance is outdated. The average home price in Canada is about $800,000; most Canadians are not setting aside $8,000 to $24,000 for repairs and maintenance. A figure closer to $2,400 per year for the average Canadian home is more reasonable.

The specific amount can depend on several factors, including the age, condition, and location of the home.

Factors Influencing Maintenance Budget:

- Age of the Home: Older homes typically require more maintenance and repair.

- Condition: Homes that have been well-maintained require less immediate upkeep than homes that have deferred maintenance issues.

- Type of Home: Detached homes often require more maintenance than condominiums, where many maintenance responsibilities are handled by the condo association.

- Climate and Location: Homes in areas with harsh weather conditions or increased exposure to natural wear (like coastal areas with salt spray) may need more frequent maintenance.

Budgeting Tips:

- Save Monthly: Setting aside a portion of your monthly budget for home maintenance can help spread out the expenses.

- Prioritize Repairs: Focus on urgent repairs that could lead to more significant problems if ignored.

- Immediacy: Do repairs as soon as possible. Small problems left unaddressed can grow into big problems. A nickel of prevention is worth a pound of cure.

- DIY When Possible: For minor repairs or upkeep, doing it yourself can save money.

- Regular Inspections: Periodic inspections can help catch issues early, potentially reducing repair costs.

Using these guidelines, homeowners can effectively plan for maintenance costs, helping to preserve the value and functionality of their home.