A letter of employment is a fundamental document required during mortgage applications in Canada. It provides lenders with critical information about a borrower’s income stability, employment status, and financial reliability. Mortgage providers use this letter to assess the applicant’s ability to sustain mortgage payments, reducing their lending risk. Understanding its role and ensuring its accuracy can significantly impact the approval process.

A letter of employment serves as a formal verification of an individual’s job status and income. It is issued by an employer and outlines pertinent employment details such as salary, job position, and length of tenure. Unlike tax documents or pay stubs, this letter offers an up-to-date snapshot of an employee’s working conditions, confirming stability for mortgage purposes.

Why Lenders Require a Letter of Employment

Self-Employed Applicants and Employment Letters

Requesting a Letter of Employment

Why Lenders Require a Letter of Employment

Lenders mandate this document to verify an applicant’s income stream and job security. The stability of an individual’s employment directly correlates with their ability to make consistent mortgage payments. A strong employment history indicates financial reliability, while frequent job changes or temporary positions may raise concerns for lenders.

Lenders scrutinize employment letters carefully, cross-referencing them with other income documents. Any discrepancies, such as different salary figures between a pay stub and the letter, can trigger additional inquiries. You should expect lenders to contact employers to confirm the authenticity of the document and the accuracy of the information.

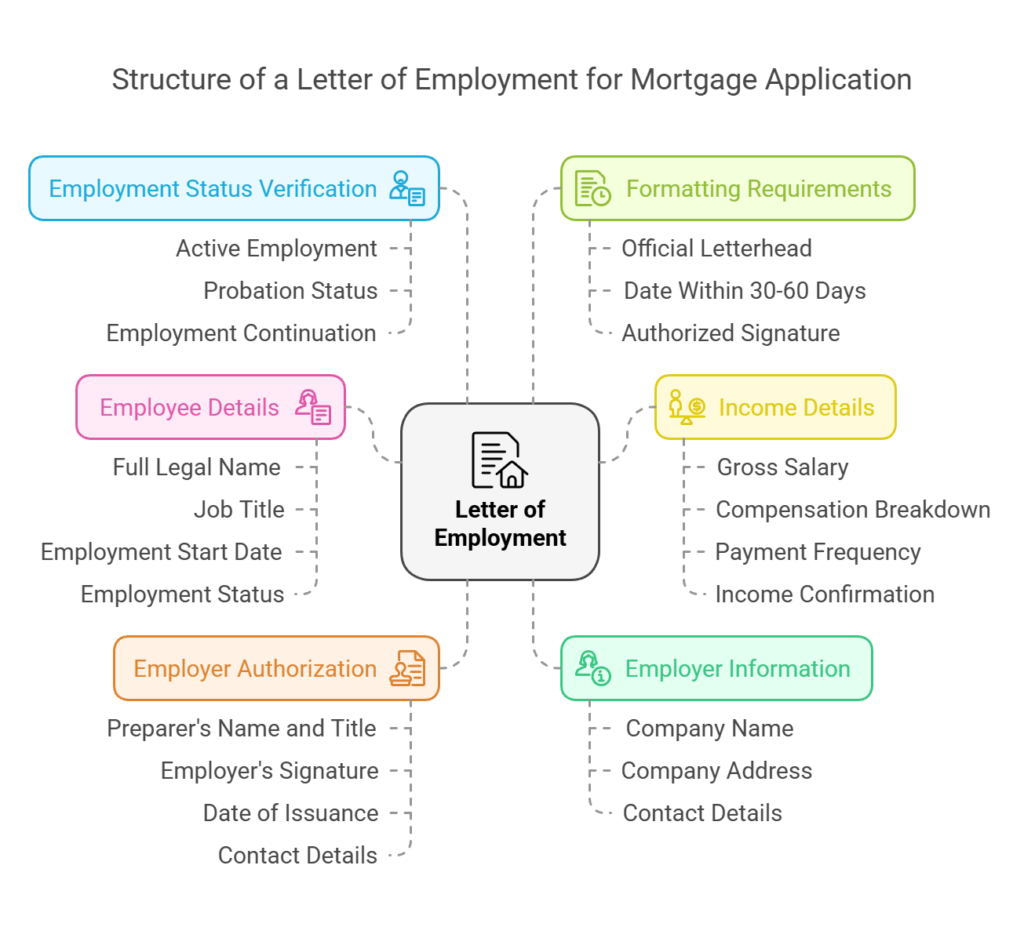

Letter of Employment Elements

A Letter of Employment for a mortgage application in Canada should contain the following elements:

1. Employer Information

- Company name

- Company address

- Company contact details (phone number and email)

- Official company letterhead

2. Employee Details

- Full legal name of the employee

- Job title/position

- Employment start date

- Employment status (full-time, part-time, contract, seasonal)

3. Income Details

- Gross annual or hourly salary

- Breakdown of compensation (base salary, bonuses, commissions, overtime, allowances)

- Payment frequency (weekly, bi-weekly, monthly)

- Confirmation of guaranteed or fluctuating income

4. Employment Status Verification

- Confirmation of active employment

- Whether the employee is on probation (if applicable)

- Expected continuation of employment (if applicable)

5. Employer Authorization

- Name and title of the person preparing the letter

- Employer’s signature

- Date of issuance

- Contact details of the signing authority (phone and email)

6. Formatting Requirements

- Printed on official company letterhead

- Dated within 30-60 days of mortgage application

- Signed by an authorized representative (HR manager, supervisor, business owner)

This letter provides lenders with the assurance that the applicant has stable and verifiable employment, making it a key component in the mortgage approval process.

Common Challenges

Many borrowers face difficulties when requesting this document. Some employers may be slow in processing requests, while others may refuse to provide certain details due to company policy. Additionally, inaccuracies or missing information can result in lender pushback, delaying the mortgage process.

An Offer of Employment letter is not a Letter of Employment. An Offer of Employment letter is not acceptable for a mortgage application.

Common errors include missing employer signatures or outdated salary information. Often times the information on a Letter of Employment(LOE) doesn’t match up with pay stubs, such as when the LOE says an employee is guaranteed a certain number of hours, but the employee cannot produce a current pay stub that reflects this. Incongruities are problematic for lenders.

Errors in employment letters can create unnecessary delays. Common mistakes include:

- Incorrect job titles

- Misstated salary figures

- Missing employer contact details

- Lack of an official company letterhead or signature

Probationary Periods

Applicants in probationary periods may face challenges as lenders perceive higher risk. Some lenders require applicants to complete the probationary term before mortgage approval. Providing additional proof of future employment stability, such as an offer letter, can help mitigate concerns.

Self-Employed Applicants and Employment Letters

Self-employed individuals typically do not receive employment letters. Instead, lenders require:

- Notices of Assessment (NOAs) for the past two years

- Business financial statements

- Bank statements showing consistent income deposits

- Accountant-prepared income verification letters

Requesting a Letter of Employment

When requesting a letter, employees should:

- Ask the HR department or direct supervisor

- Clearly state the required details for mortgage purposes

- Follow up persistently if delays occur

- Review the letter for accuracy before submission

Summary

A letter of employment is a pivotal document in Canadian mortgage applications, serving as a primary means of verifying income and job stability. Ensuring it is professionally drafted, accurate, and comprehensive can significantly enhance mortgage approval chances. By understanding lender expectations and preparing supporting documents in advance, applicants can streamline the mortgage process and secure their financing with confidence.