Purchasing a home is one of the biggest financial decisions Canadians make, whether it’s your first property, an investment, or a new place to call home. Yet, many start their journey by looking at listings or visiting open houses before knowing what mortgage they qualify for. To avoid disappointment and discover possibilities, your first priority should be securing a mortgage agent—one who’s knowledgeable, trustworthy, and committed to your long-term success.

Types of Mortgage Professionals

Qualities of a Great Mortgage Agent: What to Look For

Real-World Example: The Long-Term Value of a Quality Mortgage Agent

How to Choose Your Mortgage Agent

Cost of Working with a Mortgage Agent

Securing the Right Agent is Worth the Effort

Types of Mortgage Professionals

Before we delve into choosing the right mortgage agent, it’s essential to understand what a mortgage agent is and how they differ from other types of mortgage advisors, such as mortgage specialists at banks.

- Bank Mortgage Specialists

- Mortgage Agents

- Mortgage Brokers

Bank Mortgage Specialists

Known by many different names, people who sell mortgages at banks are unlicensed salespeople who are not required to have any education or expertise in mortgages or real estate finance, they are commissioned salespeople. They could have been selling shoes in the mall last week. They can only offer you products from their specific bank and cannot give you independent mortgage advice. They may have limited flexibility when it comes to finding the best rate or terms that suit your situation. Their loyalty ultimately lies with their employer.

Mortgage Agents

Mortgage Agents are provincially licensed financial professionals who work independently through a brokerage. They have access to various lenders, including banks, credit unions, and alternative lenders. A mortgage agent can shop the mortgage market for you, finding competitive rates, products, programs, and terms tailored to your needs. They are not limited to one institution, and the best agents prioritize your long-term financial well-being over a quick transaction. Their loyalty is to their clients and this loyalty is re-enforced by provincial statute and brokerage policies.

Mortgage Brokers

Mortgage brokers are provincially licensed financial professionals who provide oversight and ensure mortgage agents comply with industry standards, as well as federal and provincial legislation and regulations. They provide support to mortgage agents by providing back-office support and technological assistance, such as cybersecurity. They may also support agents through underwriting and mortgage fulfilment services. Mortgage brokers may also sell mortgages; when they do, they are acting as mortgage agents, but their primary function is to support mortgage agents.

As a customer needing a mortgage, the mortgage professional you interact with primarily is a mortgage agent.

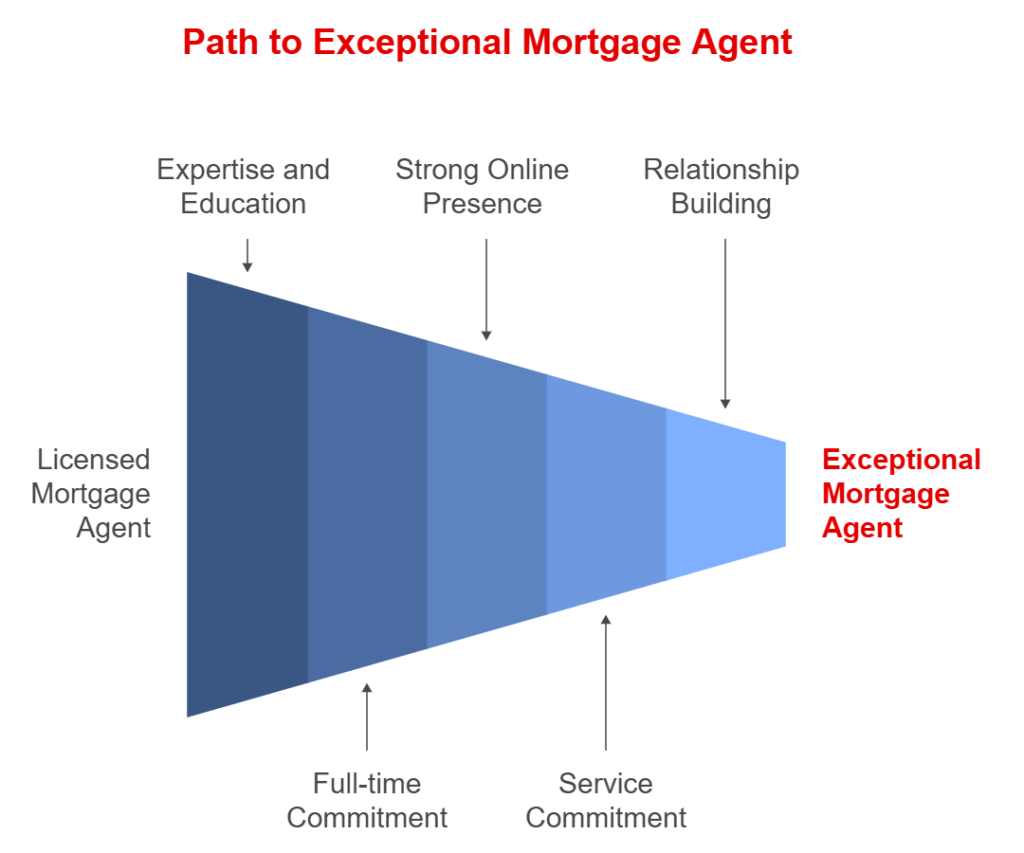

Qualities of a Great Mortgage Agent: What to Look For

The Canadian mortgage industry is highly regulated, but there is still a significant range in the quality of service mortgage agents provide. Here’s what sets an exceptional mortgage agent apart from the rest:

- Expertise and Education

- Full-time Mortgage Agent

- Strong Online Presence

- Commitment to Advice and Service

- Long-term Relationship Building

- Transparency, Confidentiality and Privacy

Expertise and Education

The truth is that it is not too difficult to become licensed as a mortgage agent. Anyone can sign up for the mortgage agent course, do it online, get hired by a mortgage brokerage, and in a few short weeks become a licensed mortgage agent. There is no requirement to have any post-secondary education, not even grade 8.

The problem is that while it is easy to get licensed as a mortgage agent, there is a vast chasm between someone who is just licensed and the top mortgage agents who have multiple university degrees, often with master’s degrees, and deep experience in the real estate industry, often with backgrounds that include residential improvement, home inspection, and home construction. Such backgrounds enable savvy mortgage agents to have the knowledge to provide financial advice around lending on all aspects of real estate.

Full-time Mortgage Agent

Further, most people who get licensed only try to sell mortgages as a side hustle, it is not their main occupation. Professional full-time mortgage agents watch ‘the screens’ all day, watching rates the way a stockbroker watches stock prices. They are talking to lenders, speaking with real estate, legal, and financial professionals, attending lender presentations, doing analytics and research, and servicing their clients throughout the day. The mortgage business is a 24/7 type of business; it is not something you can do part-time.

Strong Online Presence

A strong online presence is ‘the proof’ that defines top mortgage agents. Finding a mortgage agent with a strong online presence is important for several reasons, especially in today’s digital world where clients often begin their search for services online. A strong online presence is the indicator of a mortgage agent’s credibility, expertise, and client-centered approach:

- Transparency and trustworthiness

- Access to valuable educational content

- Availability of digital tools and resources

- Professionalism and industry knowledge

- Easy communication and responsiveness

- Verification of professional credentials

- Demonstrates client-centred approach

- Proof of success and industry reputation

- Proof they are on the leading edge of the industry

Commitment to Advice and Service

The best mortgage agents don’t just process paperwork; they take the time to educate you on every step of the mortgage process. They explain terms like “fixed vs. variable rates,” “amortization periods,” and “prepayment options.” They know it is important to empower you with knowledge to enable you to make informed decisions. Look for an agent who emphasizes guidance and education, not just securing your mortgage.

Top mortgage agents are there for you when you need them and respond quickly when you call or text. Real estate finance and the mortgage business is a fast-paced business, things can’t wait, so it is imperative to work with a mortgage agent who responds immediately, including on weekends and evenings; money never sleeps.

Long-term Relationship Building

An exceptional mortgage agent is there not just for your first mortgage but as a long-term financial partner. As your needs change, I can offer insights on refinancing, home equity options, and other mortgage-related decisions. For example, if interest rates drop significantly, as a proactive mortgage agent I will alert you to potential savings by refinancing. I keep you informed of what is going on in the market so you can stay informed and build your future in a way that is right for you.

Transparency, Confidentiality, and Privacy

Trustworthiness is a cornerstone of a good mortgage agent. Seek out agents who are transparent about fees, commissions, and lender kickbacks. Agents who are upfront about potential challenges or costs that could arise down the road and help you feel secure in your decision.

When applying for a mortgage, you are required to provide a large amount of personal and financial information to be approved and receive financing. As our world has become increasingly complex and the loan amounts have increased substantially, the amount of documentation required to be submitted has grown accordingly, reflecting the growing complexity of the mortgage approval process.

It’s paramount that you work with a mortgage agent who protects your confidentiality and your privacy. You need to know your personal and financial information is being protected and your information is secure. Ultimately it comes down to one, single question, “Can I trust you and your organization to protect me and keep me safe?”

Real-World Example: The Long-Term Value of a Quality Mortgage Agent

Consider Sarah, a first-time homebuyer in Ontario. Sarah initially considered going to her local bank for a mortgage but was referred to a licensed mortgage agent by a friend. Her agent not only secured a better interest rate by comparing offers from multiple lenders but also provided her with information on first-time homebuyer programs that reduced her upfront costs.

A few years later, Sarah’s agent noticed that interest rates were dropping and proactively reached out to suggest refinancing, which saved Sarah thousands over the life of her mortgage. Today, Sarah continues to consult her mortgage agent for advice on real estate investments, and they work together on a strategy for her family’s financial future.

How to Choose Your Mortgage Agent

Finding a mortgage agent in Canada who aligns with your financial goals and needs can set you up for success on your real estate journey. Here’s a step-by-step guide on how to find a mortgage agent who will be a strong, trusted advisor.

- Mortgage Agent Website and Media Platforms

- Check License Status

- Check Education and Other Credentials

- Ensure the mortgage agent is full-time; and not a side hustle

- Ask for Recommendations and Referrals

- Interview Multiple Agents

Mortgage Agent Website and Media Platforms

While the internet offers many tools and directories of mortgage agents to help you find a mortgage agent, their evaluation of mortgage agents is extremely poor, especially in the areas of expertise and education.

To really get to know a mortgage agent, their knowledge, expertise, and background, seek out their website. You’ll quickly discover most agents don’t have a website and the few that do just have templated sites provided by their brokerage or a simple site they paid someone else to create.

If a mortgage agent is truly dedicated to your empowerment, you’ll find hundreds of current articles they have written to educate you and demonstrate their knowledge in this fast-moving business.

You can’t write about what you don’t know.

Check Licensing Status

In Canada, mortgage agents must be licensed by their provincial regulatory authority. Ensuring your mortgage agent is licensed is vital for a few reasons:

- Professional Standards: Licensed agents adhere to industry regulations and standards, protecting your interests.

- Accountability: Licensed agents are held accountable by provincial authorities and are required to meet educational and ethical standards.

- Certification: Some agents have certifications, like Certified Mortgage Professional (CMP), which can indicate advanced knowledge and expertise.

You can verify a mortgage agent’s license by checking with your province’s financial regulatory body. Here’s a quick reference for the most popular provinces:

- Ontario: Financial Services Regulatory Authority of Ontario (FSRA)

- British Columbia: BC Financial Services Authority (BCFSA)

- Alberta: Real Estate Council of Alberta (RECA)

- Quebec: Organisme d’autoréglementation du courtage immobilier du Québec (OACIQ)

Check Education and Other Credentials

There are many different aspects to real estate financing. Education and broader experience matter. Getting your mortgage agent license is not very difficult, just takes a few weeks of online studying. You need much more out of your mortgage agent.

Does the mortgage agent have a degree or even a master’s degree? A degree will help define the level of professionalism you can expect.

Does your mortgage agent understand residential real estate; have they taken courses in real estate or even been a former realtor themselves or are they putting a mortgage on something they have limited understanding of.

Does your mortgage agent understand home renovations? Difficult to finance something you don’t understand.

Does your mortgage agent know home inspection and have the ability to evaluate the quality of a home, especially since most mortgages require an appraisal that evaluates the quality of the structure and the surrounding property?

Education, experience, and credentials matter. The more your mortgage agent knows, they more they will be able to get you the financing you need and illustrate possibilities you were not aware of.

Ensure the Mortgage Agent is Full-time

It is critically important that a mortgage agent works as a mortgage agent full-time and is not trying to get away with doing mortgages as a side hustle. This happens because it is too easy to get licensed as a mortgage agent. Most people who try to sell mortgages part-time are just in it to try to make a quick buck. It’s estimated that 90% of people who get licensed don’t stay in the business. They have not made the necessary commitment to the industry or their clients.

Being a professional mortgage agent is just not something you can do part-time and provide professional service to a client. Beyond the need for much more education than just taking an online mortgage agent course, I can tell you that being a mortgage agent is something I do all day and all night and still feel like I haven’t got everything done. You can’t know what’s going on or be on top of all the changes by regulators, be on top of industry technology, know the thousands of lenders’ products, watch the markets, or be properly servicing customers with the biggest financial commitment they will ever make in their lives if a mortgage agent is trying to get away with doing the business part-time.

Ask for Recommendations and Referrals

Referrals from trusted sources can be one of the best ways to find a reliable mortgage agent. Consider asking:

- Friends, Family, and Colleagues: If someone close to you had a good experience with a mortgage agent, it’s worth considering the same agent. Ask about their experience, how helpful the agent was, and if they’d use them again.

- Real Estate Agents: Many realtors have preferred mortgage agents they work with regularly. A real estate agent can point you toward mortgage agents they trust and have seen achieve great results for their clients.

- Financial Planners and Advisors: These professionals often work closely with mortgage agents and may know of agents who align well with your financial goals.

Interview Multiple Agents

Once you’ve gathered a few options, it’s essential to speak with at least two or three mortgage agents before making a decision. This will give you a sense of their communication style, experience, and approach. Here are some key questions to ask:

- What is your website? – The quality and depth of your mortgage agent’s website is a huge tell about who they are, their professionalism, and what kind of service you can expect.

- What lenders do you work with? – A good mortgage agent should have access to a wide variety of lenders, from major banks to credit unions to alternative lenders.

- What is your experience with clients like me? – Agents who’ve worked with people in similar financial situations will likely be better equipped to help you.

- How do you stay informed about market changes? – Mortgage agents who actively follow trends can alert you to new opportunities for refinancing, home equity options, or advantageous interest rates.

- What is your fee structure? – Most mortgage agents don’t charge fees directly to clients, as they’re compensated by the lender upon closing. However, in unique situations (such as when working with alternative or private lenders), fees may apply, so it’s best to clarify upfront.

You can also ask to see client testimonials or, in some cases, data points they can share anonymously. This will give you confidence that the agent has a track record of achieving good outcomes for their clients.

Cost Of Working with A Mortgage Agent

Working with a mortgage agent is typically free for most clients.

For most clients, there is no cost to work with a mortgage agent for a standard residential mortgage, as lenders cover the commission. In special cases (such as private, commercial, or complex credit situations), a fee might be charged, but it will be disclosed upfront. Always confirm any potential fees during the initial consultation to understand the full cost before proceeding.

- No direct fees for most standard mortgages

- When fees may apply

- Fee Disclosure and Transparency

- Are There Benefits to Paying a Fee?

No Direct Fees for Most Standard Mortgages

For most conventional residential mortgages, there is no cost to the client to work with a mortgage agent. Here’s why:

- Commission-Based Compensation: Mortgage agents are generally compensated by the lender upon successful mortgage closing. This commission varies by lender but typically ranges from 0.5% to 1% of the total mortgage amount.

- Lender-Paid Compensation: The lender pays the mortgage agent’s commission directly, so the client doesn’t incur any direct fees. This arrangement is standard for mortgage agents working with traditional lenders (like banks and credit unions) and major alternative lenders.

When Fees May Apply

There are situations where fees may be charged to the client, usually in more complex or high-risk mortgage cases. These fees cover the additional work involved in securing financing in these situations:

- Private or Alternative Lending: For clients who require private financing or work with non-traditional lenders, a fee may apply. This is because these lenders often work with more specialized funding sources that may not offer commission structures. Fees in these cases typically range from 1% to 4% of the mortgage amount, depending on the complexity and risk.

- Commercial or Investment Properties: Mortgages for commercial or multi-unit investment properties can sometimes incur fees since these types of loans involve more complex underwriting and a smaller pool of available lenders.

- Challenging Credit or Income Situations: If a client has credit issues, is self-employed, or lacks traditional proof of income, finding a suitable lender may require more time and effort.

Fee Disclosure and Transparency

Mortgage agents are required to disclose all fees upfront if they apply. You should receive a clear explanation of any fees involved when they’re due and whether they’re refundable if the mortgage doesn’t go through. Most reputable mortgage agents will walk you through the fee structure (if any) during your initial discussions.

Are There Benefits to Paying a Fee?

In cases where fees apply, it’s often because the agent is working with specialized or high-risk lenders, which can benefit clients with unique needs. Many such lenders do not pay any compensation to the mortgage agent for the work they perform in securing the mortgage; consequently, the mortgage agent must charge the client a transparently disclosed, reasonable fee for the work they perform. Unreasonable fees are likely to be reviewed by the provincial regulator. Paying a fee may allow the agent to access a broader range of lending options, providing financing solutions that may not be available through traditional routes.

Securing the Right Agent is Worth the Effort

Finding the right mortgage agent may require a bit of research, but the results are well worth it. A good mortgage agent does more than get you the best rate; they become a partner in your financial journey, offering insights, advice, and support throughout your homeownership years. Whether it’s your first property, an investment, or a new place to call home, start your journey by building a relationship with a professional mortgage agent. By following these steps, you’ll increase your chances of finding an agent who not only helps you secure your mortgage but also guides you toward a prosperous financial future.