As your trusted and experienced mortgage agent, my role is not just to secure you a mortgage, but to carefully match you with the right lender — one who truly fits your financial situation, your goals, and your future plans. Today, I want to introduce you to a lending partner you might not yet know by name: EQ Bank, a division of Equitable Bank.

Choosing a lender you haven’t heard of before might feel daunting at first. But when you understand who EQ Bank is, the kind of lender they are, and the advantages they offer, you’ll quickly see why they have become an essential choice for many Canadians seeking flexible, competitive real estate financing.

What Kind of Lender is EQ Bank, and What Does That Mean for You?

Three Powerful Reasons to Choose EQ Bank for Your Mortgage

Who is the Ideal Client for EQ Bank?

Who is EQ Bank?

EQ Bank is the digital arm of Equitable Bank, Canada’s 7th largest Schedule I bank. Founded over 50 years ago, Equitable Bank has built a reputation on innovation, reliability, and customer-focused lending. They are a publicly traded institution on the TSX (symbol: EQB), subject to the same federal regulations and oversight as any of Canada’s “Big Five” banks.

What sets EQ Bank apart is their modern approach: they offer online, streamlined banking experiences with a strong emphasis on mortgage solutions for clients with unique needs — whether it’s self-employed income, investment properties, or credit challenges. Their backing by Equitable Bank means they have the strength and stability of a major financial institution, combined with the flexibility and responsiveness of a specialized lender.

In short: EQ Bank is a fully regulated, well-capitalized, innovative bank — and a strategic advantage for borrowers who value smart, adaptive lending.

What Kind of Lender is EQ Bank, and What Does That Mean for You?

EQ Bank operates in both the prime and alternative (“B”) lending spaces. This means they serve two types of borrowers:

- Prime borrowers: Clients who have strong income, credit, and straightforward borrowing needs.

- Alternative borrowers: Clients who may be self-employed, new to Canada, experiencing temporary credit setbacks, or purchasing investment properties.

Because they understand that “life happens” — and that not every excellent borrower fits into a traditional bank’s narrow box — EQ Bank looks beyond just credit scores. They use a common-sense approach, evaluating the whole story behind each application.

What this means for you: You have access to a lender that offers real solutions when traditional banks may say no, while still providing highly competitive rates and terms.

Three Powerful Reasons to Choose EQ Bank for Your Mortgage

Here’s why I confidently recommend EQ Bank for many of my clients:

- Exceptional Flexibility for Self-Employed Borrowers and Investors

- Competitive Rates and Specialized Products

- Human Service in a Digital World

Exceptional Flexibility for Self-Employed Borrowers and Investors

EQ Bank specializes in working with business owners, contractors, consultants, and real estate investors. They allow:

- 12 months of bank statements to verify income.

- Business financials and T4/T4A addbacks to maximize qualifying income.

- Up to 10 rental properties financed with simplified rental income calculations (95% offset and add-back options).

This flexibility is a game changer for entrepreneurs and investors who are often misunderstood by traditional banks.

Competitive Rates and Specialized Products

Whether it’s their:

- Adjustable Rate Mortgages (ARM) with low penalties,

- Home Equity Lines of Credit (HELOCs) at prime + competitive spreads,

- Reverse mortgages up to 59% loan-to-value,

- Extended ratios programs (up to 60% Total Debt Service for qualifying clients),

- Or net worth-based lending programs —

EQ Bank provides highly attractive financing options that are specifically built to give borrowers more options at better pricing.

Human Service in a Digital World

Despite being a modern digital bank, EQ Bank offers dedicated underwriting teams, rapid turnaround times (often 24-hour commitments), and personalized deal structuring. I work directly with their senior mortgage officers and underwriters to make sure your application is handled with priority and care.

In a world where many lenders treat clients like just another file number, EQ Bank stands out for its collaborative, people-first approach.

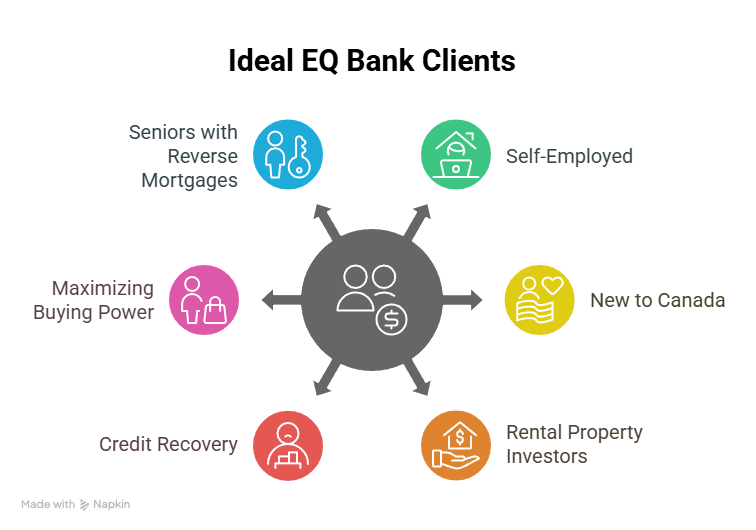

Who is the Ideal Client for EQ Bank?

You might be a perfect match for EQ Bank if you are:

- Self-employed or running your own business, even without traditional T4 income.

- New to Canada with strong employment but limited Canadian credit history.

- An investor managing multiple rental properties needing streamlined qualification.

- Recovering from credit setbacks, such as past consumer proposals or bankruptcies.

- Looking to maximize buying power with extended debt service ratios.

- Seniors considering reverse mortgage solutions to unlock the equity in your home.

EQ Bank particularly shines for financially responsible clients who simply don’t fit the old-fashioned checklists of traditional banks.

Why EQ Bank Stands Apart

While many lenders claim to be “flexible,” EQ Bank consistently delivers real solutions. They are willing to listen to the full story behind a client’s situation and craft lending options accordingly. Their ability to blend common sense underwriting, competitive pricing, and modern service delivery is rare — even among Canada’s most innovative lenders.

Their success is not just about offering different products; it’s about understanding today’s borrowers are diverse, dynamic, and deserving of better, faster, smarter financing.

Final Thoughts

As your mortgage agent, my job is to act as your advocate and strategist. I only recommend lenders I trust — and EQ Bank has earned that trust by helping my clients succeed where others might not even listen.

If you’d like to explore how EQ Bank could be a fit for your mortgage needs, whether you’re buying, refinancing, investing, or planning for retirement, I would be honored to guide you through every step of the process.

Let’s unlock the best mortgage solutions together.