When shopping for a mortgage, Canadians have a choice between fixed-rate mortgages and variable-rate mortgages without getting into all the different kinds of fixed-rate and variable-rate mortgages. It’s complicated. Most people have no idea, but you have to start at the beginning, which is being able to compare a given fixed-rate mortgage to a variable-rate mortgage, do the math, and see what works best for you; you’ll probably be surprised!

In Canada, the majority of mortgages are fixed rate. As of recent years, approximately 70% to 75% of all mortgages in Canada are fixed-rate mortgages. This preference for fixed-rate mortgages is due to their lower interest rate and the stability and predictability they offer, as borrowers are protected from interest rate fluctuations during the term of the mortgage.

Yet, this wasn’t always so, and there was a time when variable-rate mortgages reigned supreme. Variable-rate mortgages rule the marketplace when interest rates were low and stable, especially during the early 2000s, after the 2008 financial crisis, and again in 2015 when the Bank of Canada maintained a low-interest-rate environment in response to global economic uncertainties and low inflation. This led to a resurgence in the popularity of variable-rate mortgages, as the interest rate savings over fixed-rate mortgages were appealing to many borrowers.

Fixed-Rate vs Variable Rate: Doing the Math

Fixed vs Variable: The Scenario

Variable-Rate Mortgage Penalty

Mortgage Interest Cost: Fixed vs Variable

Fixed Rate vs Variable Rate: Doing the Math

What Canadians don’t consider is that 60% of Canadians will need to refinance their mortgage sometime before the end of the term (link to article(s)). When you refinance, you are essentially replacing your current mortgage with a new one, which usually involves paying off the existing mortgage and creating a new mortgage agreement with potentially different terms, such as a new interest rate, term length, or loan amount. Some borrowers switch lenders due to dissatisfaction with their current lender’s service or because another lender offers products or services that better meet their needs. New lenders may offer incentives to attract borrowers, such as covering the costs of switching (e.g., appraisal fees, legal fees) or offering cash bonuses. Refinancing a mortgage will require you in Canada (unlike the United States (LINK)) to pay a penalty, often a substantial one (hold on to your socks!). How much penalty you pay depends greatly on whether you have a variable rate mortgage or a fixed rate mortgage.

Read More:

Breaking Your Mortgage: Canada vs United States

10 Reasons Canadians Refinance Their Mortgage

4 Ways to Refinance Your Mortgage

Fixed vs Variable: The Scenario

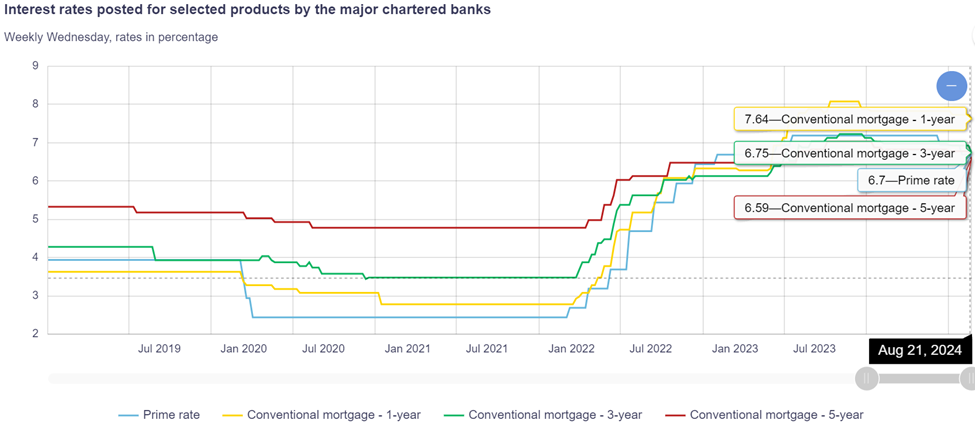

John and Mary in Anytown, Anyprovince, Canada want to buy a $900,000 house, have enough money for a $300,000 down payment and closing costs, and now need a $600,000 mortgage. They are debating on whether to get a 5-year fixed or 5-year variable mortgage at a Canadian bank. The bank has a posted rate of 6.59% for a 5-year fixed mortgage. They are aware of the penalties for breaking a mortgage in Canada. They also know from Allen Ehlert that variable mortgages are offered at a higher interest rate than fixed-rate mortgages. They want to know, if after 2 years on this mortgage (3 years remaining), if something happens that requires John and Mary to refinance, break their mortgage, and pay the penalty, which mortgage would be the best to get; fixed or variable.

Let’s take a look.

Variable Rate Mortgage Penalty

For a variable-rate mortgage, the penalty is generally calculated as three months’ interest. Assume an interest rate of 5.85% on a 5-year variable rate mortgage. John and Mary need to break after 2 years of a 5-year term.

Step 1: Calculate the Monthly Interest

- Monthly Interest Rate: 5.84% annually = 5.84% / 12 months = 0.4867% per month

- Monthly Interest Payment: 0.004867 × $600,000 = $2,920.20

Step 2: Calculate Three Months’ Interest

- Three Months’ Interest: $2,920.20 × 3 = $8,760.60

Final Penalty for Variable-Rate Mortgage: $8,760.60

If John and Mary break their variable rate mortgage after 2 years to refinance, consolidate debt, or switch lenders, they will have to pay a penalty of $8760.60.

Fixed Rate Mortgage Penalty

When you need to refinance a fixed-rate mortgage, an Interest Rate Differential (IRD) penalty applies. To calculate the Interest Rate Differential (IRD) penalty for John and Mary if they decide to refinance a 5-year fixed-rate mortgage at 5% after 2 years (banks’ posted rate is 6.75%), with a remaining mortgage balance of $600,000, calculated as follows:

Step 1: Understand the Components

- Current Mortgage Rate: 5%

- Original Term: 5 years

- Remaining Term: John and Mary have 3 years remaining on the mortgage.

Posted Rate: 6.75% (for a term equal to the remaining term, typically the 3-year posted rate if 3 years remain)

- Outstanding Balance: $600,000

Step 2: Calculate the IRD Penalty

The IRD penalty is calculated based on the difference between the mortgage rate (5%) and the current posted rate (6.75%) applied to the remaining balance for the remainder of the term.

- Difference in Rates:

- Mortgage Rate: 5%

- Posted Rate for Remaining Term: 6.75%

- Rate Difference: 6.75% – 5% = 1.75%

- Calculate the Interest Rate Differential:

- IRD = (Rate Difference) × (Remaining Balance) × (Remaining Term)

- IRD = 1.75% × $600,000 × 3 years

- Convert the Percentage to Decimal:

- 1.75% = 0.0175

- Calculate the Penalty:

- IRD Penalty = 0.0175 × $600,000 × 3 = $31,500

Final IRD Penalty:

In this scenario, the IRD penalty to refinance the mortgage would be $31,500.

If John and Mary break their fixed rate mortgage after 2 years to refinance, consolidate debt, or switch lenders, they will have to pay a penalty of $31,500 (that’s $22,739 more in penalty than breaking the variable rate mortgage).

Considerations:

- Bank Policies: The exact calculation method may vary slightly depending on the lender’s specific terms and how they apply the posted rates (some might use the rate discount given at the start of the mortgage instead of the posted rate).

- Verification: This is a basic calculation, and actual penalties may vary depending on the specific terms and conditions of the mortgage agreement, as well as any potential discounts or adjustments applied by the lender. There may also be caps or floors on the penalty.

- Consultation: It is advisable for the client to confirm the exact penalty with their lender, as the lender may have specific methods for calculating the IRD penalty. (see link to article)

- Cash Back: If the client received cash back when they got their mortgage, a portion of the cashback will need to be repaid.

Mortgage Interest Cost: Fixed vs Variable

To complete our comparison, we need to look at the difference in interest cost between the fixed-rate mortgage and the variable-rate mortgage for 2 years. We select 2 years because we have 3 years left in our 5-year term mortgage after we need to break the mortgage to do refinancing.

After doing the calculations:

- Fixed-Rate Mortgage (5%): The interest cost over the first two years is approximately $58,551.56.

- Variable-Rate Mortgage (5.84%): The interest cost over the first two years is approximately $68,783.22.

In the first two years, the variable-rate mortgage costs more in interest compared to the fixed-rate mortgage, reflecting the higher interest rate on the variable-rate loan.

Total Cost: Fixed vs Variable

If you must break your mortgage after 2 years, would you be farther ahead with a fixed mortgage or a variable mortgage?

Fixed Mortgage

Interest Cost: $58,551.56

IRD Penalty: $31,500

Fixed-Rate Mortgage Total Cost: $90,051.56

Variable Mortgage

Interest Cost: $68,783.22.

3 Months Interest Penalty: $8,760.60

Variable-Rate Mortgage Total Cost: $77,543.82

Generally speaking, when comparing a 5-year variable rate mortgage with a 5-year fixed rate mortgage, when you have to break your mortgage 2 years into the mortgage, the fixed rate mortgage is about $12,500 more expensive than the variable rate mortgage.

Under these circumstances, the variable rate mortgage, despite the higher interest rate, is the better choice.

So, the real question is, given that 60% of Canadians will need to refinance their mortgage during their term (and most never thought that they would need to), should you go variable, knowing you’ll save about $12,500 because of mortgage penalties if you need to refinance or go fixed, because you don’t think you’ll be like most Canadians, and you are sure you will not need to break your mortgage?

Instead of going with a 5-year fixed mortgage at 5%, Allen Ehlert advises John and Mary to consider a 3-year fixed mortgage at 5.15%. Variable rate mortgages are offered as 5-year terms and so in this example, the variable rate mortgage’s interest rate doesn’t change.

A Different Strategy

Under the same circumstances, the total costs of the 3-year fixed-rate mortgage are:

The total interest cost at 5.15% on the first 2 years of a $600,000 mortgage is $60,413.97.

IRD Penalty (2 years into a 3-year term): $14,940

Total Cost: $75,354

There is about a $2,190 savings in total costs in favour of the 3-year fixed mortgage vs. the 5-year variable mortgage if John and Mary break the mortgages after 2 years of the 3-year term, and $8,369 in savings if John and Mary don’t need to refinance their mortgage.

Don’t Get Blinded by Rate

Interest rates are important, but because mortgages are complicated, people look only at rates when comparing mortgage products. This example proves that chasing the cheapest rate often ends up being the most expensive option. There is always so much more than rates when it comes to mortgages. Contact Allen Ehlert to get the best advice on one of the biggest financial decisions you will make in your life.