Navigating the world of mortgages can be daunting for both new and seasoned homeowners. A fundamental aspect of any mortgage is the “mortgage term,” which dictates several key financial decisions and outcomes over the course of homeownership. My goal in this article is to demystify mortgage terms, explore various available options, compare mortgage terms with mortgage amortization, and examine the implications of mortgage terms on penalties in Canada. Additionally, I will look at various scenarios to help borrowers choose the appropriate mortgage term based on their unique financial situations.

Comparing Mortgage Terms and Amortization

Implications of Mortgage Term on Penalties

Term Implications for Open and Closed Mortgages

Scenario Analysis: Choosing the Right Mortgage Term

What is a Mortgage Term?

In Canada, a mortgage term is the length of time during which the conditions of a mortgage contract, including the interest rate, are fixed and agreed upon by both the lender and the borrower. More simply, a mortgage term is the amount of time you are under contract with your mortgage lender. This term can range from a few months to several years, with the most common periods being 1, 3, and 5 years. Importantly, the mortgage term should not be confused with the mortgage’s amortization period, which is the total time it takes to repay the mortgage in full.

Types of Mortgage Terms

Mortgage terms come in various lengths and can be broadly categorized into short-term and long-term mortgages:

- Short-Term Mortgages: These typically last from 6 months to 3 years and are suitable for those who anticipate changes in interest rates or their financial situation.

- Long-Term Mortgages: Terms extending from 4 to 10 years, or even longer, offer stability in payments and are ideal for borrowers seeking consistency in their financial planning.

Comparing Mortgage Terms and Amortization

While the mortgage term refers to the duration of the contract terms, the amortization period is the overall timeline for paying off the mortgage. For example, a homeowner might have a 25-year amortization period with a 5-year mortgage term. At the end of the 5-year term, they would need to renew their mortgage, possibly under different terms or interest rates, until the full loan is amortized or paid off.

Confusion often occurs because Canadians often hear about 30-year mortgages. Americans have 30-year mortgage terms where the terms of the mortgage, such as interest rate, remain the same over the 30-year mortgage term. Canadians mainly have 5-year mortgage terms, but those mortgages can be amortized 25 year, 30 years and possibly even longer. Canadians do not have 30-year term mortgages.

Refinancing and Term

Refinancing a mortgage involves renegotiating the terms and conditions of an existing mortgage before its term expires, typically to take advantage of lower interest rates, access home equity, or consolidate debt. The choice of mortgage term during refinancing is crucial as it can impact the interest rate and the overall financial strategy of the borrower.

Shorter terms might offer lower rates and greater flexibility, allowing homeowners to adapt more quickly to changing financial situations or market conditions. Conversely, longer terms provide more stability in interest rates and monthly payments, which can be beneficial during periods of volatile interest rates or when budgeting is a priority.

Refinancing usually incurs costs, such as penalties for breaking the original mortgage term early, appraisal fees, and legal fees, which should be carefully weighed against the potential benefits of the new mortgage terms. Therefore, when considering refinancing, homeowners should evaluate their long-term financial goals, current economic trends, and personal risk tolerance to choose the term that best aligns with their needs.

Renewal

When a mortgage term concludes, borrowers face a critical decision: renewing their mortgage. Understanding how mortgage terms influence renewal options and strategies is essential for long-term financial planning. This section delves into the intricacies of mortgage renewals in Canada, offering insights into how the length and type of the original mortgage term can affect future borrowing conditions.

The Renewal Process

As a mortgage term reaches its end, the remaining balance of the loan must either be paid in full or renewed with a new term at potentially different conditions. Most borrowers opt to renew their mortgage, which involves negotiating a new term and interest rate with their lender or shopping around for better offers from other financial institutions.

Impact of the Original Mortgage Term on Renewals

- Rate Fluctuations and Term Length

- Short-term mortgages typically offer the flexibility to adapt more frequently to changing interest rates. If rates decrease, borrowers can benefit from lower rates upon renewal without waiting too long. Conversely, if rates increase, they are also exposed to higher rates sooner.

- Long-term mortgages provide stability against rate fluctuations over a more extended period. However, this can be a double-edged sword. While securing a low rate for many years can protect borrowers from rising rates, they might also miss out on potential savings if rates fall during their term.

- Financial Stability and Predictability

Renewing a mortgage after a long-term period often means fewer renewals over the amortization period, simplifying financial planning and reducing exposure to rate changes at each renewal. This predictability can be particularly beneficial for those on fixed incomes or tight budgets.

- Negotiation Leverage

- The end of a mortgage term offers an opportunity to renegotiate terms based on current financial standings and credit scores. Borrowers in good financial health or those who have seen improvements in their credit status may secure more favourable rates and terms during renewal.

- Lenders often send out renewal offers before the current term ends, typically offering existing rates or slightly better terms to retain their customers. However, savvy borrowers will shop around to ensure they are getting the best deal available, leveraging competitive offers to negotiate with their current lender.

Renewal Strategies Based on Mortgage Terms

- Anticipating Economic Changes

Borrowers should stay informed about economic trends as their renewal approaches. If interest rates are expected to rise, securing a longer-term mortgage at a current lower rate could save money in the long run. - Adjusting for Personal Circumstances

If there’s a possibility of significant life changes, such as a career move or family expansion, considering a more flexible term at renewal can be beneficial. This might mean switching from a fixed to a variable rate, or choosing a shorter term to allow for more frequent reassessment of financial needs and goals. - Utilizing Equity

Renewal time also provides an opportunity to tap into home equity for debt consolidation, home improvements, or other significant expenditures. This can be achieved by renegotiating a larger mortgage, provided that the increased debt load remains manageable.

Mortgage renewals present an opportunity for homeowners to reassess their financial strategies and adapt their mortgages to their current and anticipated future needs. By carefully considering the impact of their initial mortgage term on their renewal options, borrowers can make informed decisions that align with both their immediate and long-term financial goals. Always consider consulting with a financial advisor or mortgage specialist to explore the best renewal strategies tailored to individual financial situations.

Mortgage Terms and Rates

Interest rate is a critical factor that can significantly impact the total cost of borrowing. Interest rates can vary based on the length of the mortgage term, among other factors. Generally, lenders adjust rates to reflect the risk and economic forecast associated with the duration of the term. This article will rank the typical mortgage terms by their associated interest rates and provide insights into how these rates are typically structured.

Understanding Interest Rates Across Different Mortgage Terms

Interest rates are influenced by several factors, including the lender’s assessment of risk, economic conditions, and the Bank of Canada’s policy. Here’s how different mortgage terms typically rank in terms of interest rates:

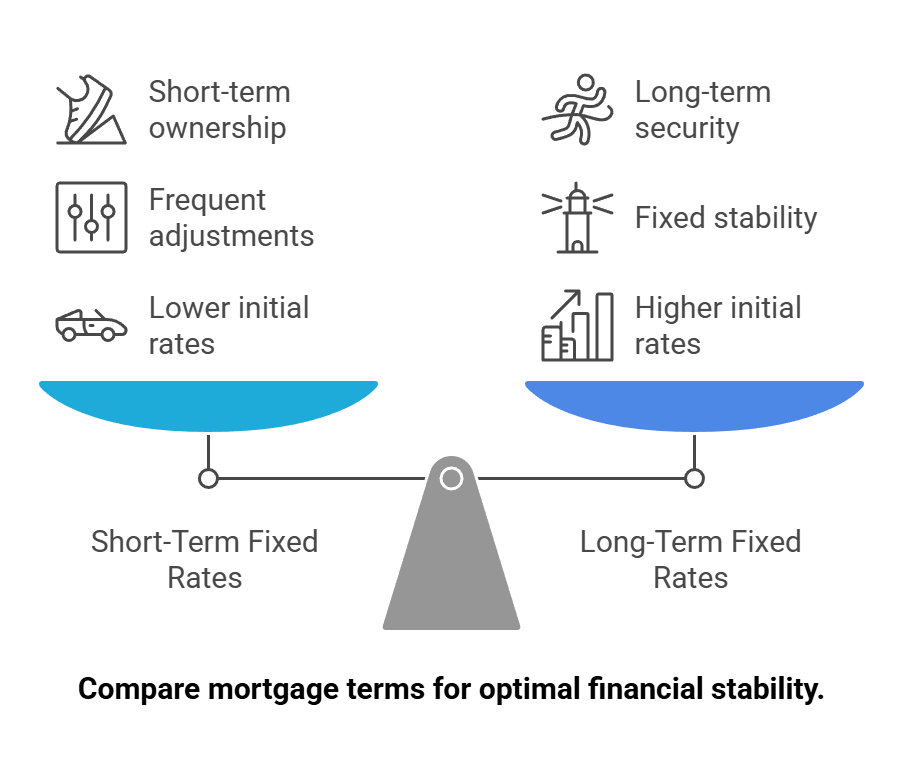

- Variable Rates and Short-Term Fixed Rates (1-2 years)

- Characteristics: These rates are often lower than those for longer terms (7 to 10 years) because they expose borrowers to more frequent rate adjustments based on market conditions. The lower rates compensate for the risk of future rate increases.

- Suitable for: Borrowers who anticipate a drop in interest rates or those planning short-term ownership.

- Medium-Term Fixed Rates (3-5 years)

- Characteristics: These are the most common choices for Canadian homeowners. The 5-year fixed rate is usually the lowest interest rate mortgage available, followed by the 3-year fixed rate. The rates are typically higher than short-term rates but provide a middle ground of stability without locking in for too long.

- Suitable for: Homeowners looking for a balance between rate stability and flexibility.

- Long-Term Fixed Rates (7-10 years)

- Characteristics: These rates are usually higher, reflecting the lender’s risk in fixing the rate for an extended period. Borrowers pay a premium for the security of knowing their rate will not change. Generally, long-term fixed-rate mortgages are the most expensive compared to other mortgage terms, but if you are lucky enough to lock in a very low rate, such as those offered during the pandemic, you’d be enjoying those rates for the next 10 years. Remember, Americans have 30-year terms.

- Suitable for: Borrowers seeking long-term stability in their monthly payments, especially in a low-rate environment.

Interest Rate Trends and Economic Influence

- Economic Environment: During periods of economic instability or high inflation, longer-term rates may be more appealing as they protect borrowers from potential rate increases.

- Market Predictions: Financial experts and market trends can also influence decisions. If rates are expected to rise, locking in a longer-term rate might be wise. Conversely, if rates are predicted to fall, opting for a shorter term could be beneficial.

Choosing the right mortgage term and associated rate is a strategic decision that should align with a borrower’s financial situation, risk tolerance, and future plans. By understanding how mortgage terms typically rank in terms of interest rates, borrowers can make more informed decisions that optimize their financial health over the term of their mortgage. As always, consulting with a mortgage professional can provide personalized advice and insights tailored to individual financial circumstances.

Implications of Mortgage Term on Penalties

Choosing the right mortgage term is crucial due to the penalties for breaking a mortgage agreement early. In Canada, mortgage penalties can be substantial, particularly with fixed-rate mortgages, where penalties are often calculated using the “interest rate differential” (IRD).

The IRD method for calculating mortgage penalties on a fixed-rate mortgage takes into account the amount of time remaining on the mortgage contract or term. The longer the amount of time remaining on the mortgage term, the higher the mortgage penalty. Consequently, you need to take into account when considering your mortgage strategy, the likelihood that you may need to break your mortgage because if you do, any savings you may have thought you’d make by focusing on interest rate could be wiped out multiple times by failing to consider the costs of breaking your mortgage.

In contrast, variable-rate mortgages typically use three months’ interest to calculate penalties. Understanding these differences is vital for homeowners to make informed decisions about refinancing or selling their properties before the term ends.

Term Implications for Open and Closed Mortgages

Mortgages are either open or closed, each offering distinct flexibilities and restrictions that cater to different borrower needs.

An open mortgage allows borrowers to pay off their loan at any time without incurring penalties, making it an ideal choice for those who anticipate coming into extra funds or plan on selling their home in the near future. However, the trade-off for this flexibility is typically a higher interest rate compared to closed mortgages.

On the other hand, a closed mortgage often features lower interest rates but includes restrictions on the amount of extra money a borrower can put toward their mortgage annually without facing a prepayment penalty. Closed mortgages suit those who do not anticipate paying off their mortgage early and seek the stability of consistent, predictable payments. The choice between an open and closed mortgage will largely depend on the borrower’s financial stability, future plans, and risk tolerance.

At the end of a mortgage term, otherwise known as ‘at renewal’, borrowers can stay with an open or closed mortgage, or switch depending on their new circumstances.

Scenario Analysis: Choosing the Right Mortgage Term

- Scenario: Rising Interest Rate Environment

- Term Choice: Short-term or variable-rate mortgage.

- Rationale: Allows the borrower to reassess and potentially secure a lower rate if interest rates stabilize or drop in the near future.

- Scenario: Stable Financial Situation and Market

- Term Choice: Long-term fixed-rate mortgage.

- Rationale: Locks in a low rate for financial predictability and protection against potential rate increases.

- Scenario: Plans to Move or Sell Shortly

- Term Choice: Short-term or open mortgage.

- Rationale: Minimizes penalties due to early termination of the mortgage.

- Scenario: First-Time Homebuyer with Limited Funds

- Term Choice: Long-term fixed-rate mortgage.

- Rationale: Ensures consistent and predictable mortgage payments, aiding in budget management.

Summary

Understanding the nuances of mortgage terms is crucial for making decisions that align with personal financial goals and market conditions. By carefully selecting the mortgage term, Canadian homeowners can manage their finances more effectively, minimize penalties, and adapt to both their changing needs and the economic landscape. Always consult with a mortgage professional to tailor financial decisions to individual circumstances, ensuring that the chosen mortgage strategy optimally supports long-term goals.