In Canada, understanding and monitoring your credit score is crucial for managing your financial health. This score, a numerical representation of your creditworthiness, impacts various aspects of your financial life, from securing loans to negotiating better terms on credit. Here’s my expert guide on how you can access your credit score in Canada, its cost, its value, and strategies to improve it.

How to Get Your Credit Score in Canada

Is It the Same Score that a Mortgage Agent or Lender Would Get?

The Value of Knowing Your Credit Score

Credit Score Ranges and Classifications

How to Improve Your Credit Score

How to Get Your Credit Score in Canada

Canadians have several options to access their credit scores:

- Credit Bureaus

- Financial Institutions

- Online Financial Service Platforms

Credit Bureaus:

Equifax and TransUnion: These are the two main credit reporting agencies in Canada. Both agencies offer direct access to your credit score and reports through their websites.

Cost: Equifax offers a one-time credit report and score for a fee, or you can subscribe to a monthly service that provides ongoing access to your score and report. TransUnion offers similar services, with options for both one-time access and monthly subscriptions. Costs can vary, typically around $19.95 for a one-time report and score.

Financial Institutions:

Many banks and credit unions in Canada provide free credit score checks as a part of their online banking services. For instance, banks like RBC, CIBC, and Scotiabank offer this service to their clients. Cost is generally free as a part of banking services.

Online Financial Service Platforms:

Platforms like Borrowell, Credit Karma, and Mogo offer free access to your credit score and report, sourced from either Equifax or TransUnion. The cost is free.

Is It the Same Score that a Mortgage Agent or Lender Would Get?

The credit score you access yourself may differ from the “beacon score” that a mortgage agent or lender would pull. This is due to different scoring models and the specific version of the credit scoring formula that financial institutions might use for credit decisions. The scores you check yourself are often educational scores, while lenders might use scores tailored for specific credit products.

The Value of Knowing Your Credit Score

Knowing your credit score is invaluable for several reasons:

- Loan Qualification: It gives you an insight into what lenders see when you apply for credit, affecting your ability to qualify for loans, credit cards, and mortgages.

- Interest Rates: It can influence the interest rates you are offered; higher scores generally mean lower rates.

- Financial Planning: Regularly checking your score helps you understand how your financial behaviours affect your credit standing.

Credit Score Ranges and Classifications

In Canada, credit scores typically range from 300 to 900, and the way these scores are interpreted can vary slightly between the two major credit reporting agencies, Equifax and TransUnion. Here’s a general guide to understanding what different scores mean in terms of credit quality:

Excellent (800-900): This score range is considered exceptional. Borrowers with scores in this range usually enjoy the best interest rates and loan terms available. They are seen as very low-risk for lenders.

Very Good (720-799): Scores in this range are also highly favourable. Consumers with scores in this bracket are typically offered competitive interest rates and can generally qualify for a variety of lending products easily.

Good (650-719): A score in this range indicates a fairly responsible credit history. Borrowers here get average interest rates and have good options for most loans but may not qualify for the lowest rates.

Fair (600-649): This range is deemed satisfactory. Consumers with scores in this bracket are considered subprime borrowers and may face higher interest rates. While they can still obtain credit, the terms are less favourable.

Poor (300-599):

Scores in this range are considered low and often indicate significant credit issues or limited credit history. Borrowers in this category may find it difficult to secure traditional loans and may need to look at high-interest or secured credit options.

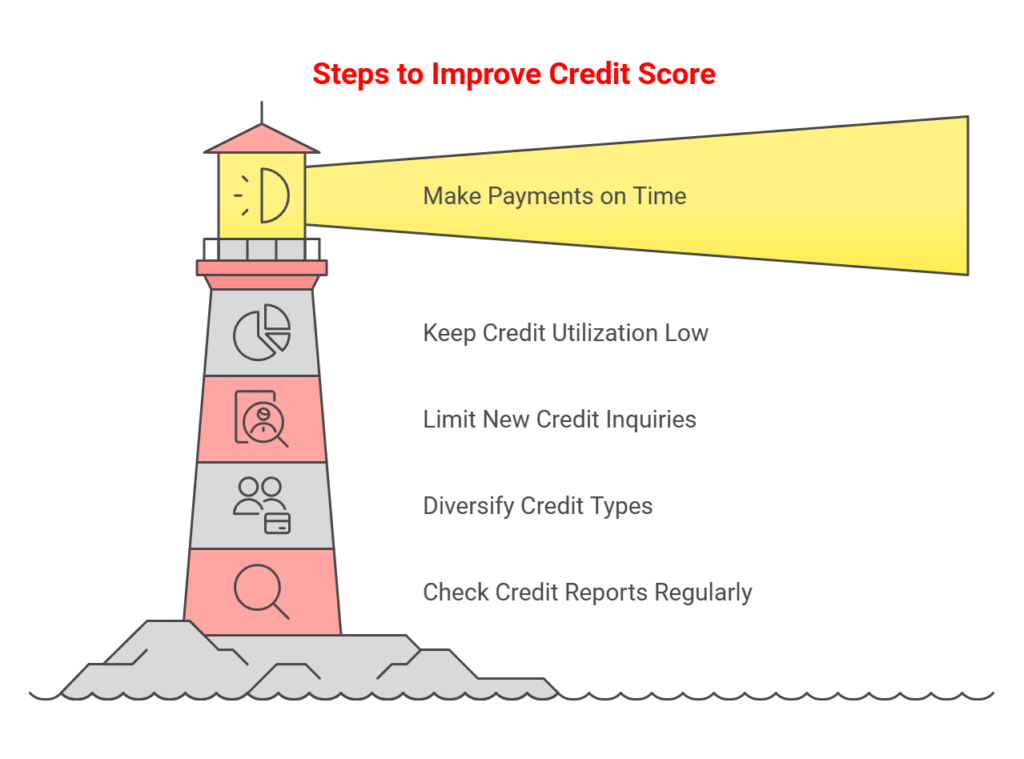

How to Improve Your Credit Score

Improving your credit score is a strategic process that involves managing your credit responsibly over time:

- Make Payments on Time: Always pay your bills and existing loan obligations on time. Late payments can significantly impact your credit score negatively.

- Keep Credit Utilization Low: Try to use less than 30% of your available credit limit across all your accounts. High utilization can signal risk to creditors.

- Limit New Credit Inquiries: Each time you apply for credit, a hard inquiry is made, which can lower your score. Limit the frequency of new credit applications.

- Diversify Your Credit Types: Having a mix of different types of credit (e.g., revolving credit like credit cards and instalment loans like a car loan) can positively affect your score.

- Check Your Credit Reports Regularly: Ensure there are no errors or fraudulent activities on your accounts. Dispute any inaccuracies you find with the respective credit bureau.

Conclusion

Understanding and monitoring your credit score in Canada is more accessible than ever, with multiple free and paid options available. While the scores provided by consumer platforms may differ slightly from those used by lenders, they still offer valuable insights into your financial health. Regularly checking your score, understanding the factors that affect it, and taking steps to improve it are crucial components of sound financial management.