When shopping for a mortgage, or any loan for that matter, it is important to think like a bank.

When it comes to securing a mortgage, most people don’t realize they’re stepping into a sophisticated business game. Banks are experts at maximizing profits, and unless you understand their strategies, you might end up paying more than you need to.

Ever wondered why your loyalty to one financial institution doesn’t always pay off? Or why shopping around for a mortgage isn’t just a smart idea—it’s an absolute necessity? In this guide, we’ll dive into the hidden tactics banks use to keep you locked in, the financial traps of complacency, and how you can flip the script to take control of your mortgage journey.

With the right approach—and the right ally, like a licensed mortgage agent—you can navigate this complex landscape, avoid the loyalty penalty, and secure the best possible deal for your unique circumstances. Let’s break down the insider strategies that banks don’t want you to know and how you can come out ahead.

Banking is a Business

Fundamentally, what is a bank? A bank is a business. A business is an organization that operates to generate profit for its shareholders who have invested their money with the expectation of a return. A bank takes depositors’ money for a low interest rate and lends it out to customers (often in the form of mortgages) at a higher rate. Financial types call this spread Net Interest Margin. The wider the NIMS, the more profit for the bank and the greater the return for shareholders. In short, a bank takes in money at the lowest rate possible and lends it out at the highest rate possible.

As a potential customer of a bank or any lender, you want the exact opposite of what you are offered. You want high interest for your deposits, but you want to borrow money at the lowest interest rate possible.

The Need to Lock You In

However, a bank is not a single-product financial institution. A bank has many financial products to sell from investments like GICs, stocks, and bonds, to various forms of insurance, to different kinds of bank accounts and banking services, to many different types of loans and even credit cards. A bank wants to sell you all these different products so you can become many different kinds of revenue streams for the bank. But to do this, the bank knows it needs to have a relationship with you, that’s the key, so you will only deal with them. Like any business, a bank wants you to be loyal only to them.

Everyone Else Shops Around

But is dealing with only one financial institution a good idea? If you are looking for a car, do you consider only one manufacturer and ignore all the others? If you are looking for a contractor to do work on your house, do you not get at least three quotes? When you apply for a job, doesn’t your potential employer request 3 references?

We all know that when you shop around you get a better deal. Being blindly loyal to only one company usually means that you end up paying more. If you stay with the same insurance company and don’t regularly shop around, you pay more car insurance. If you just deal with only one cell phone provider, you end up paying more, but why?

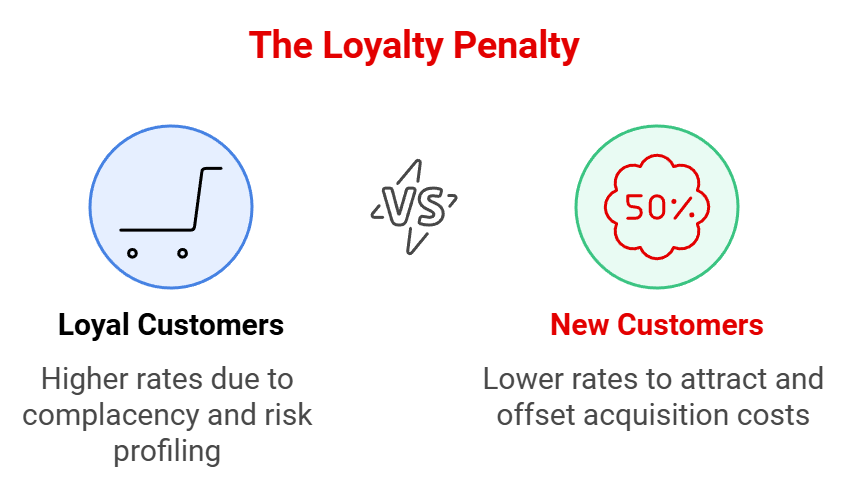

The Loyalty Penalty

This phenomenon is often referred to as the “loyalty penalty” or what companies cleverly refer to as “price optimization”. You pay a loyalty penalty because:

Complacency

Companies may bank on the complacency of long-term customers who don’t regularly check for better deals. They know it’s hard work to shop around, and businesses often use confusing wording or their own terminology for common things so you can’t shop compare. With these difficulties, customers are less likely to switch providers, allowing businesses to take advantage and gradually increase premiums.

Risk Profiling

Businesses sometimes use sophisticated algorithms to determine how likely customers are to tolerate price increases or switch providers. Those deemed less likely to shop around are targeted for higher rate increases.

Acquisition Cost

Acquiring new customers usually costs more than retaining existing ones. Businesses might offer lower rates to new customers to attract them, while gradually increasing rates for existing customers to offset acquisition costs. When you don’t shop around, you pay more because other customers do shop around.

The Shop Around Advantage

When it comes to mortgages, shopping around for the best mortgage is extremely important for several reasons:

Competitive Pricing

Different mortgage lenders often offer competitive rates to attract new customers. By shopping around, you can compare different lenders’ rates and find the most cost-effective option for your needs.

Tailored Options

Different lenders offer various options and discounts. Shopping around allows you to find a mortgage that best suits your specific needs and integrates well with your financial plan, your family circumstances, your work circumstances, your age and much more. Every lender offers different options and different costs for each lender. It’s important to know all the options available to you in the marketplace and no single lender is going to give you this perspective. They want you to only buy their product.

Changing Circumstances

Your personal and financial circumstances, such as age, marital status, employment, health, financial stresses, inheritance, etc. change over time. Often circumstances change unpredictably with little warning. These changes can have a big impact on what sort of mortgage is best for you. Regularly comparing your mortgage options ensures that you are always getting the best deal based on your current situation.

Market Changes

I always say the mortgage market is like a raging river; like the stock market, it is incredibly dynamic, with rates fluctuating due to factors like changes in the economy, the Bank of Canada, government regulation, taxation, competition between lenders, the real estate market, and much more. The only thing constant is rapid change. By shopping the market, you stay informed about the current market rates, mortgage offerings

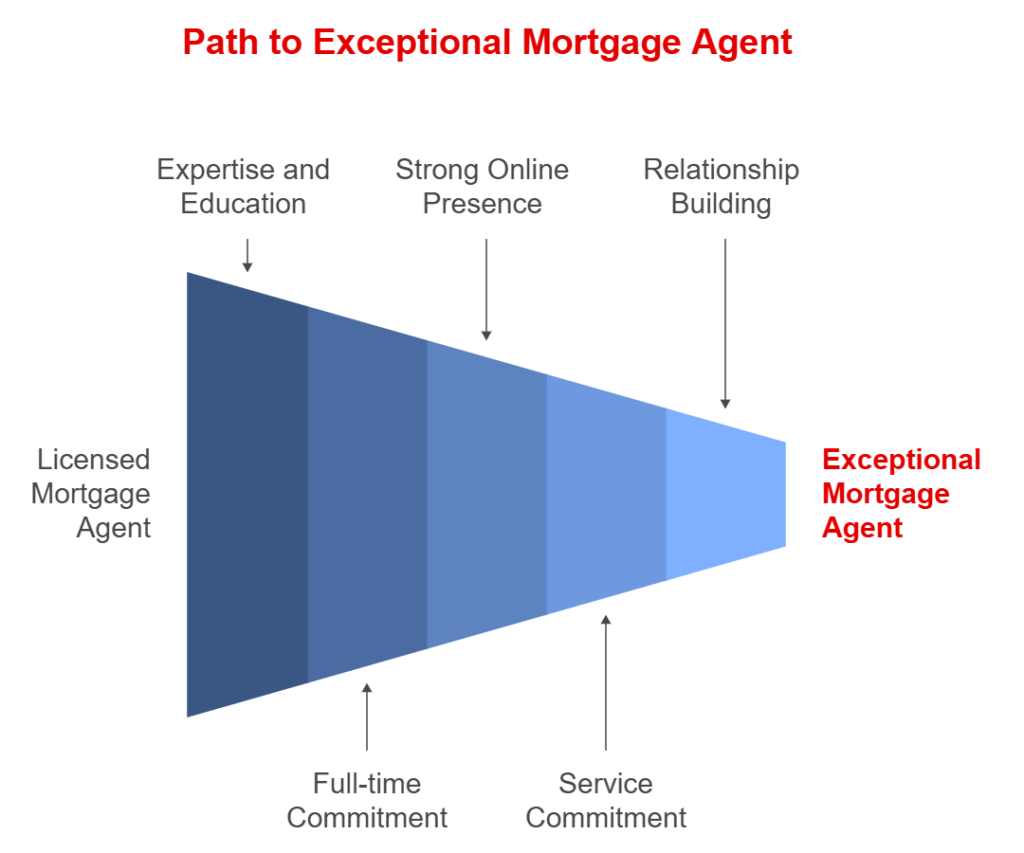

Why You Need a Mortgage Agent

But in truth, mortgages are extremely complex loan agreements. Not only within each mortgage agreement itself, but between mortgage lenders as well. How can someone who is not a mortgage professional shop the market when trying to do anything more than look at the posted rate? It is nearly impossible. This is why it is critical to use the services of a provincially licensed mortgage agent.

A trusted, licensed mortgage agent should:

- Assess your financial situation

- Provide expert advice

- Have access to multiple lenders

- Negotiate on your behalf

- Handle paperwork and application process

- Provide ongoing support

- Save time and stress

Assess Your Financial Situation

A mortgage agent should evaluate your financial status, including your income, debts, credit score, and savings. This assessment helps in determining how much you can afford to borrow and what type of mortgage would be most suitable for you. Your agent should consider your broader life goals, and financial and personal circumstances so the agent can target the mortgage options and offerings that are best for you.

Provide Expert Advice

Mortgage agents are knowledgeable about the various mortgage products available in the market. They can offer expert advice on different types of mortgages, interest rates, terms, and conditions to help you make an informed decision.

Access to Multiple Lenders

How many places can you think of where you can get a mortgage? Most mortgage agents have access to the offerings of 40 or more lenders and can compare and contrast the offerings of each. Unlike being limited to the products of a single financial institution, mortgage agents have access to a wide range of lenders, including banks, credit unions, and other financial institutions. This access allows them to shop around on your behalf to find competitive rates and terms that fit your needs so you will never have to pay that ‘loyalty penalty.’.

Negotiate on Your Behalf

Mortgage agents can negotiate with lenders to secure favourable terms and conditions for your mortgage. Their experience and relationships with lenders can be advantageous in getting you a better deal. Real estate agents often cite their ability to negotiate with superior experience and skills honed from the many deals they have closed. Likewise, mortgage agents are skilled negotiators who owe you in law a fiduciary duty to negotiate on your behalf to your advantage.

Handle Paperwork and Application Process

Applying for a mortgage involves a lot of paperwork and can be time-consuming. A mortgage agent can guide you through the application process, help you complete the necessary documents, and ensure that everything is submitted correctly and on time.

Provide Ongoing Support

A good mortgage agent will offer ongoing support throughout the life of your mortgage. They can assist with any questions or concerns you may have and can help you with future mortgage-related needs, such as refinancing or renewals. If something happens in your life or you have any concerns, reach out to your mortgage immediately so they can devise solutions while there is still time.

Save Time and Stress

By handling the legwork of finding and applying for a mortgage, a mortgage agent can save you time and reduce the stress associated with navigating the complex mortgage landscape.

A mortgage agent acts as an intermediary between you and potential lenders, providing expertise, access to a variety of mortgage options, negotiation skills, and support throughout the mortgage process. Their services can be particularly beneficial for first-time homebuyers, those with unique financial situations, or anyone looking to find the best mortgage terms available.

Best of all a mortgage agent’s services are free to you!