Where you get your mortgage can have a big impact on how much you have to pay in regular mortgage payments, how fast you can pay off your house, and what you need to do and have to qualify for. When asked, most Canadians think that ‘the bank’ is the only place they can get a mortgage. They are unaware that there are many kinds of lenders available to them beyond the banks, that there are dozens and dozens of lenders competing for their business, or that they can do much better than they are doing now.

Canada’s Largest Mortgage Seller

Percentage of Renters, Owners, and Mortgagees

Why Canadians Buy Mortgages at Banks

Canada’s Largest Mortgage Seller

The largest lender of mortgages in Canada is typically one of the country’s major banks, often referred to as the “Big Five” banks. These banks are:

- Royal Bank of Canada (RBC)

- Toronto-Dominion Bank (TD)

- Bank of Montreal (BMO)

- Canadian Imperial Bank of Commerce (CIBC)

- Scotiabank (Bank of Nova Scotia)

Among these, Royal Bank of Canada (RBC) and Toronto-Dominion Bank (TD) are frequently contenders for the position of the largest mortgage lender in Canada, based on the total value of their residential mortgage portfolios. That doesn’t make them the best place to get a mortgage! The exact ranking can vary over time due to changes in market conditions, lending practices, and business strategies.

However, for many borrowers, getting a mortgage at a bank is not the best option; it is just the option they know about. Just like anything else, you need to shop the market to get the best deal. The good news is you don’t have to; that’s what a mortgage agent like myself does for you, and best of all, my services to you are free!

READ MORE: Discover All the Mortgage Lenders

Who Has a Mortgage?

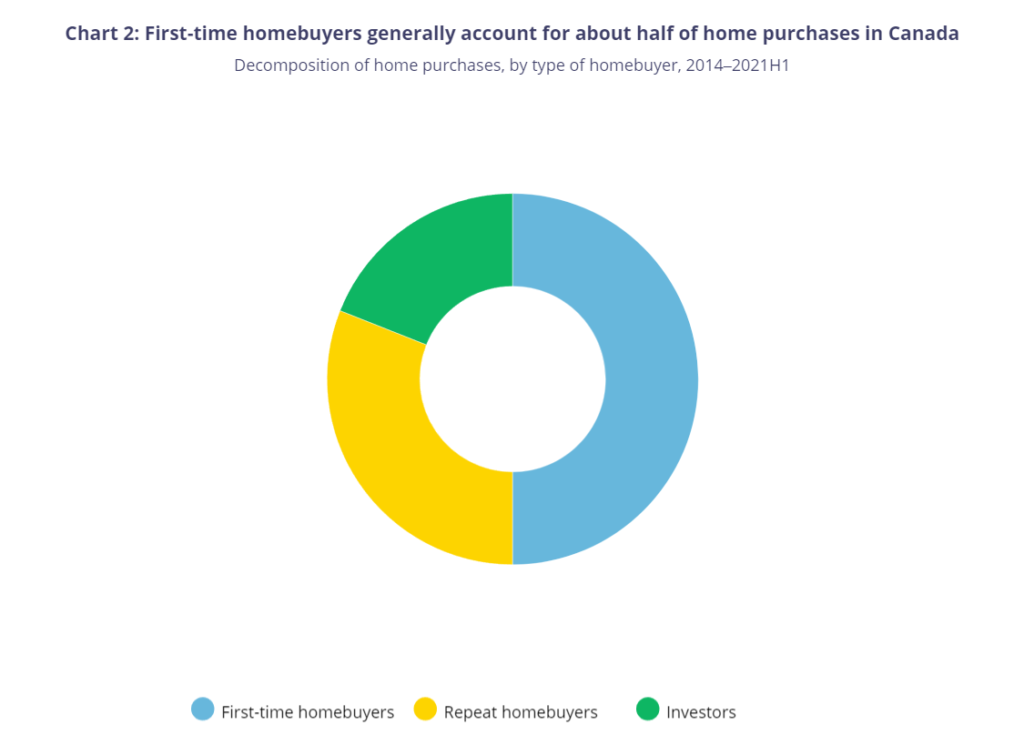

Most Canadians who get mortgages are first-time buyers, as first-time homebuyers account for about half of all home purchases in Canada. Most first-time buyers are typically around the age of 40, up from 36 just a few years ago.

Percentage of Renters, Owners, and Mortgagees

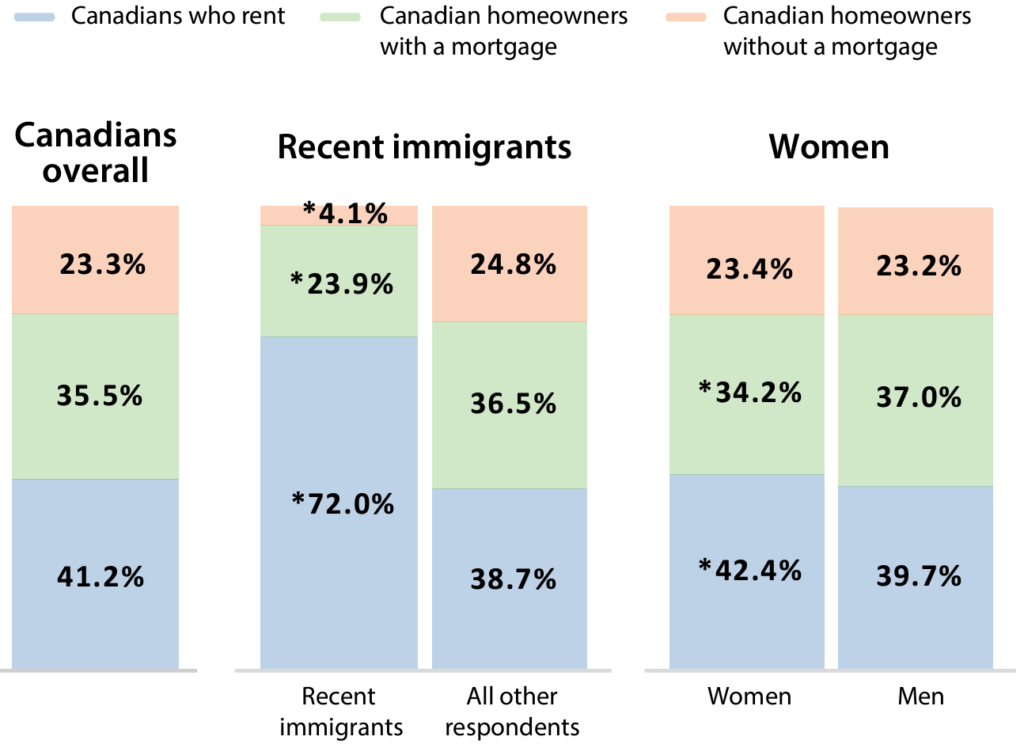

In Canada, according to a report by the Financial Consumer Agency of Canada, 23% of Canadian homeowners are mortgage-free, 41% rent, and 36% have a mortgage.

More key facts:

- 9 in 10 Canadian homeowners between 25 and 44 (88%) have a mortgage

- 17% of Canadian seniors (65+) have a mortgage

- The average mortgage is $338,522

- Defaults are historically low at 0.15 percent

- Approximately 30% of Canadians are debt-free

- Approximately 50% of mortgages are 5-year fixed mortgages

- The average age to be mortgage-free is 56 in Quebec, 57 in Ontario, and 58 in Western Canada

- The average age of first-time home buyers was 36, but now it is approximately 40.

Where Canadians Buy Mortgages

Due to a lack of knowledge Canadians have about where they can get a mortgage, 60% of Canadians purchase a mortgage through a bank. Purchasing a mortgage through a bank often has the benefit of convenience, as these banks have extensive networks across the country and offer a wide range of mortgage products, making them dominant players in the Canadian mortgage market.

Why Canadians Buy Mortgages at Banks

Purchasing a mortgage through a bank has the benefit of convenience and the comfort of obtaining a mortgage from a brand that consumers know. However, like purchasing milk at a convenience store instead of going to a grocery store, customers usually end up paying more.

Do Banks Properly Disclose

Unfortunately, many Canadians don’t feel that banks are treating them honestly regarding their mortgage. “Things are kept hidden from consumers, and the consumer has to be very weary. It’s really like walking into a used car salesroom,” says Dennis Wall on the CBC show Marketplace. Banks often don’t disclose what they are locking their clients into and how that can harm them. CBC reports that banks are often not honest about what they are selling to customers.

More financially knowledgeable Canadians obtain their mortgages through a mortgage agent. Mortgage agents have access to a variety of lenders and can negotiate competitive rates on behalf of their clients. A bank mortgage salesperson only sells that bank’s products. They have no fiduciary duty to the customer. Fiduciary duty means that the mortgage agent must, by law, put the interests of their client first. The bank salesperson has no such duty. Furthermore, a mortgage agent is a provincially licensed mortgage professional who must meet and maintain the criteria set by the province. A bank salesperson is not required to be licensed.

Mortgage Agent Advantage

Mortgage agents can secure lower rates due to their relationships with multiple lenders and their ability to shop around. Just like Canadians who shop around for a better wireless plan or car insurance, mortgage agents shop and compare mortgages from a large number of lenders to get you your best mortgage.

Some of the advantages mortgage agents provide their clients include:

Negotiation and Competition

Mortgage brokers often have access to a variety of lenders and can negotiate competitive rates on behalf of their clients. They may be able to secure lower rates due to their relationships with multiple lenders and their ability to shop around.

Volume Discounts

Brokers may receive volume discounts from lenders, which they can pass on to their clients. Since brokers often bring a significant amount of business to lenders, they might be able to secure more favourable terms.

Bank Loyalty and Existing Relationships

Banks may offer competitive or preferential rates to their existing customers, especially those with a strong banking relationship or significant assets with the bank. In some cases, customers might find better rates or terms directly from their bank.

Promotional Offers

Both banks and mortgage brokers can have promotional offers at different times, which can affect the rates available. It’s important to compare current offers and not just standard rates.

Customization and Service

While brokers might offer lower rates, some borrowers may prefer the service, convenience, or specific mortgage products offered by their bank. Additionally, banks might be more willing to customize solutions for their clients.

Rate Isn’t Everything

It’s important to consider other factors beyond the interest rate, such as prepayment options, penalties, term length, and flexibility. Sometimes a slightly higher rate might come with benefits that are more valuable to the borrower.

Ultimately, it’s strongly advisable for borrowers to shop around, compare rates and terms from multiple sources, and consider their specific needs and circumstances before making a decision. Just like you get three quotes before hiring a contractor to do work on your home, ensure you shop the market to get your best mortgage.