Mortgage Articles

Your Way to Your Best Life!

Rebuild Your Credit Using Credit Cards

Discover how to use credit cards strategically to rebuild bad or bruised credit.

Use My Mortgage Stress-Test Calculator and Buy Smarter

You’re thinking about buying a home—or maybe refinancing the one you’ve got. Exciting stuff! But then that phrase pops up: “mortgage stress test.” Suddenly it feels less like house-hunting and more like prepping for a pop quiz. Don’t worry—you’re not alone. Most...

Did You Miss Your Mortgage Renewal?

I get it. Life happens. The kids need new cleats, work is busy, and before you know it, that thick envelope from your lender sits unopened on the kitchen counter for weeks. Or maybe you saw the email and thought, “I’ll deal with it later.” But here’s the thing—ignoring your mortgage renewal package can cost you big time. Let’s talk about what really happens when you don’t respond to your lender’s offer, and why taking action (even just a small one) can save you thousands.

What Kind of Appraisal Do You Get?

One of the most common questions I hear from clients and even realtors is, “Why did my neighbour get their mortgage approved without an appraisal, but I have to pay $600 for one?” Or, “Why did this property only need a quick desktop valuation while my client’s took three weeks and a full inspection?” The answer? Not all appraisals are created equal—and not all properties or clients are treated the same.

Ultimate Canadian Mortgage Affordability Optimizer

Mortgage Affordability Calculator: Living in Canada has gotten downright expensive. Between the taxes that cost more than everything else put together, grocery bills that balloon every week, and the cost of housing that feels like it’s been strapped to a rocket, Canadians are stuck in what feels like a never-ending affordability crunch. Many families are lying awake at night, staring at the ceiling, wondering how they’ll keep that all-important roof over their heads.

Articles of Incorporation and Your Mortgage

If you’re a self-employed Canadian who runs your business through a corporation, chances are you’ve already heard about Articles of Incorporation. But when it comes time to apply for a mortgage, that’s often the point where things get a little murky. Suddenly lenders want documents you haven’t looked at in ages—or maybe didn’t even know you had.

Master Business License & Your Mortgage

Grab a coffee, because we’re about to connect the dots between the Master Business License (MBL) you filed away somewhere in a desk drawer and the mortgage you’ve been eyeing. Spoiler alert: lenders care about that slip of paper more than you might think, and knowing how to wave it around—figuratively, of course—can save you headaches, heartaches, and higher interest rates.

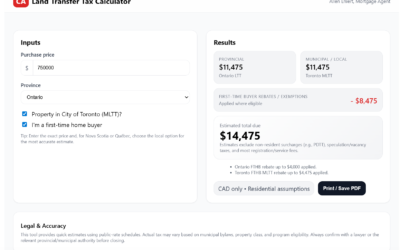

Ultimate Canadian Land Transfer Tax Calculator

… Cutting Through Canada’s Confusing Land Transfer Tax Regimes If you’ve ever bought real estate in Canada, you’ve probably run headfirst into the dreaded land transfer tax (LTT). It’s one of those costs that sneaks up on buyers and can quickly turn a dream deal into...

Commercial Mortgage 101

When you hear people talking about mortgages, they’re usually chatting about homes — houses, condos, maybe even a cute little duplex. But there’s a whole other world of financing out there: commercial mortgages. And let me tell you, it’s a different beast altogether. Whether you’re looking to buy your own storefront, scoop up an apartment building, or finally invest in that industrial unit your buddy keeps bugging you about, understanding how commercial mortgages work is absolutely crucial.

Ultimate Canadian Mortgage Penalty Calculator

Canadian Mortgage Penalty Calculators: Here’s the thing about mortgages: they look nice and tidy on paper, but the moment you want to change anything—refinance, renew early, sell before your term is up—you’ve technically “broken” your mortgage. And when you break your mortgage, you’re not walking away scot-free. You’re on the hook for a penalty.

Ultimate Canadian Mortgage-Free Accelerator Calculator

Use the Ultimate Canadian Mortgage-Free Accelerator Calculator to manipulate all the levers available in a mortgage to pay off your mortgage and become mortgage free as fast as possible.

Why Mortgages Require Appraisals

Ever wonder why, just when your client thinks they’re home free on their mortgage approval, the lender throws in the curveball: “We’ll need an appraisal.”

If you’re a realtor or a homebuyer, you’ve probably muttered under your breath, “Seriously? Why?!” Well, let’s break it down.

Ultimate Mortgage Renewal Calculator

Mortgage renewal season is here, and it’s bigger than ever. Across Canada, more mortgages are coming up for renewal than at any time in history. And while many folks just sign whatever their lender puts in front of them (because, hey, life’s busy), that simple decision can cost thousands—sometimes tens of thousands—of dollars over the life of a mortgage. Don’t lose money.

Understanding Property Evaluation

Whether you’re a realtor helping clients close deals faster, or you’re a homeowner trying to wrap your head around why some appraisals cost nothing and others come with a $700 bill attached, understanding how lenders assess property value is crucial. It’s not just about the number they land on—it’s about how they get there, and how that process affects everything from closing timelines to cash out of pocket.

Mortgages for New Medical Professionals

You’ve put in the years: university, med school, residency, sleepless nights, and long shifts. Now you’re finally launching your career as a medical professional. But despite your high earning potential, buying your first home might still feel out of reach because you don’t yet have the income history that lenders usually want to see.

Being on Commission

If you earn your living on commission — whether you’re a real estate agent, car salesperson, or any other commission-based professional — you already know that your income can feel like a bit of a roller coaster. Some months are stellar; others are… well, let’s just say you’re happy you put a little aside. But what does that mean when it’s time to buy a home? Or refinance? Or even just get pre-approved?

Why Investors Have an Unfair Advantage

Let’s face it—you’ve probably felt it yourself. You’re scrolling through property listings, crunching numbers on mortgage calculators, and wondering why it seems like the “big guys” always win. Investors seem to scoop up properties left, right, and center, often outbidding everyday families just trying to find a place to call home.

Where Does Mortgage Money Really Come From?

Ever sit across from a lender or mortgage broker and wonder, “Where are they getting all this money they’re handing out?” It’s a fair question. Most people think banks have vaults full of cash or some magical, bottomless pit of money. Not quite. The truth is, lenders have to “buy” money before they can lend it out.

Why Mortgages Aren’t Free

Have you ever wondered why mortgage rates aren’t just pulled out of a hat? Or why some lenders offer lower rates while others seem to tack on a premium? Behind every rate sheet is something called the cost of money, and if you’re in real estate or looking to buy a home, understanding this concept can give you a serious leg up. Not just for bragging rights at the next open house, but for helping you (or your clients) make sharper decisions, ask smarter questions, and understand why lenders price things the way they do.

Why Investors Aren’t Always Reliable

When you think of mortgage lenders, you probably picture big banks or trust companies with vaults full of cash just waiting to hand out. But there’s another side of the mortgage world—one that relies heavily on investors to fund deals. I’m talking about private lenders and Mortgage Investment Corporations (MICs). These lenders don’t use deposits or bonds to fund mortgages.

Mortgage in Retirement

There’s a common assumption floating around out there — maybe you’ve heard it. It goes something like this: “Once I retire, I shouldn’t have a mortgage.” Sure, in a perfect world, that’s a nice goal. But life isn’t perfect. Sometimes you downsize and still need financing. Sometimes you refinance for renovations or debt consolidation. Sometimes you’re helping the next generation with a down payment.

Mortgaging Age-Restricted Properties

Maybe you’re ready to downsize. Maybe you’re dreaming of a quieter, more community-focused place where you don’t have to shovel snow or cut the grass. Age-restricted properties — often branded as 55+ or “adult lifestyle communities” — can look like the perfect solution. But when it comes to getting a mortgage on one of these properties, things aren’t always as simple as they are with a traditional home or condo.

Non-Permanent Residents Can Buy Homes

If you’re living in Canada on a work permit or study permit and wondering if homeownership is even on the table, I’ve got good news: yes, you absolutely can buy a home. You don’t have to wait until you’ve got your Permanent Resident (PR) card in hand. But — and this is a big but — there are a few important things you need to understand about how lenders look at non-permanent residents (NPRs), how mortgages work for you, and what’s required to make it happen.

Commercial vs Residential Mortgages

Commercial vs Residential Mortgages: If you’ve ever gone through the process of securing a residential mortgage, you know the routine: income verification, a credit check, an appraisal, and a few legal documents. But when you step into the world of commercial lending, that simplicity disappears fast. Suddenly, you’re talking about holding companies, security agreements, debt covenants, environmental reports, and multi-party legal reviews.

Good Fences Make Good Neighbours

Fences and Neighbours: Replacing a fence sounds simple enough, right? Two neighbours, a bit of lumber, a weekend, and maybe a cooler of cold drinks. But once you start talking property lines, costs, and local by-laws, things can get a little prickly—especially if one neighbour wants a designer cedar wall while the other’s fine with chain link.

Why Some Lenders Borrow to Lend

You probably don’t sit around wondering how your lender pays for the mortgage they’re offering you. That’s fair—most people don’t. But if you’re a realtor or a savvy homebuyer, knowing a little about how non-bank lenders fund mortgages can help you understand why things don’t always go as planned when rates change or approvals get pulled.

Getting a Land Survey

Buying, selling, or upgrading a home is one of those times when small details can make or break the experience. You can renovate kitchens, paint walls, and swap out windows—but none of it matters much if you don’t actually know where your land ends and your neighbour’s begins. That’s where a land survey steps in. It’s the unsung hero of smart property ownership—a document that can quietly protect your investment, prevent disputes, and give everyone peace of mind.

Want to Pay Off Your Mortgage Faster?

If you’re like most homeowners, the thought of shaving years — and thousands of dollars in interest — off your mortgage is pretty appealing. You want that debt gone sooner so you can enjoy more freedom, more flexibility, and less financial pressure. The good news? You don’t have to win the lottery or double your income to do it. Sometimes, it’s as simple as tweaking how often you make your payments.

Handling Property Line Disputes

Property Line: Few things can sour a cup of morning coffee faster than a knock at the door and your neighbour saying, “You’re on my property.” Whether it’s a fence, a shed, or even a few inches of driveway, property line disputes are some of the most common—and emotionally charged—conflicts between homeowners. They don’t just stir up tension; they can affect your property’s value, your enjoyment of your home, and even future financing or resale.

What’s Your Income Story?

Once upon a time, mortgage applications were simple: you worked a 9-to-5 job, had a steady salary, and lenders barely batted an eye. Fast forward to today’s economy — people wear multiple hats, juggle side gigs, pick up overtime, and sometimes work more than one job to make ends meet or get ahead.

New to Canada? You Can Buy a Home

Moving to Canada is a huge life decision. New culture, new career, new weather (get ready for winter!), and, for many, a big dream: owning a home. But if you’ve only been here a few years and don’t have much of a Canadian credit history, you might wonder: “Can I even qualify for a mortgage?”

Lenders and Being on Commission

If you’re earning your keep on commission — whether you’re slinging homes, closing car deals, or working your tail off in any other commission-heavy gig — you already know that explaining your income isn’t always simple. Some months you’re flush; others, not so much. But when it comes to getting a mortgage, how you get paid matters just as much as how much you get paid.

The Truth About “Limited Feature Mortgages”

We’ve all seen them — those ultra-low mortgage rates advertised by the big banks or online lenders. They’re tempting, no doubt about it. Who doesn’t want to save a few bucks on interest? But here’s what you might not realize: those “basic,” “no-frills,” or “limited feature” mortgages come with some fine print that can cost you more down the road than you save upfront.

Get Ready for Open Banking

Open Banking: If you’ve ever felt like getting a mortgage meant running an obstacle course—chasing down pay stubs, digging through old bank statements, sending documents back and forth—you’re not alone. The process can feel outdated, clunky, and stressful. But here’s the good news: change is on the horizon. It’s called Open Banking, and it’s going to flip the script on how we verify income, assets, and financial history.

Self-Employed? CMHC Can Help You Buy a Home

If you’re self-employed in Canada, you already know the drill: your income looks fantastic before your accountant works their magic. After write-offs and deductions? Not so much. That’s why so many business-for-self (BFS) clients feel like they’re being punished when it comes time to apply for a mortgage. Even though you might have great cash flow, solid savings, and strong financial habits, your “net taxable income” doesn’t always tell the full story.

Who Owns the Appraisal?

If you’ve ever gone through a mortgage process and found yourself wondering, “Wait, I paid for that appraisal—why won’t the lender give me a copy?” you’re not alone. This is one of the most common sources of confusion and frustration among homebuyers, homeowners, and even some realtors. It feels like you should have a right to it, right? After all, you footed the bill!

Ultimate Canadian Mortgage Payment Scenarios Calculator

Ultimate Canadian Mortgage Payment Scenarios Calculator. It’s not just about crunching numbers—it’s about putting you in the driver’s seat. You can run scenarios, compare your current mortgage to a new one, or even pit different lenders against each other. The best part? It shows you not only how your monthly payments stack up, but also how much interest you’ll save (or pay) over the term and the entire life of your mortgage.

Featured Publications

Articles

- Extended Amortizations and Hypothetical Calculations

Office of the Superintendent of Financial Institutions (OSFI) - Minimum Qualifying Rate for Uninsured Mortgages

Office of the Superintendent of Financial Institutions (OSFI) - Residential Mortgage Underwriting Practices and Procedures

Office of the Superintendent of Financial Institutions (OSFI) - Guideline on Existing Consumer Mortgage Loans in Exceptional Circumstances Financial Consumer Agency of Canada

Book: “The Program”

- Part 1 – Building Your Down Payment

- Part 2 – Mortgage Payoff Strategies

- Part 3 – Building Wealth Through Real Estate