… How to Keep the Home When Life Changes

Divorce is never just an emotional transition—it’s a financial one too. And for many separating couples, the biggest question sitting in the middle of the table is the home.

You may be wondering: Can I keep it? Do I have to sell? What would it take financially to buy out my spouse?

Divorce financing isn’t a single solution. I consider it to be a ladder. You start with the simplest and least expensive options first, and if those don’t work, we move down the ladder to look for a solution that works for you.

As your mortgage agent, that’s exactly how I approach divorce finance. Instead of jumping straight to complicated financing, we methodically explore each rung of the ladder to see what works.

In this article, I’ll walk you through my Divorce Financing Ladder, and then I’ll show you how I’ve coded the divorce calculators on my website to help you understand where you might fit.

Topics I’ll Cover

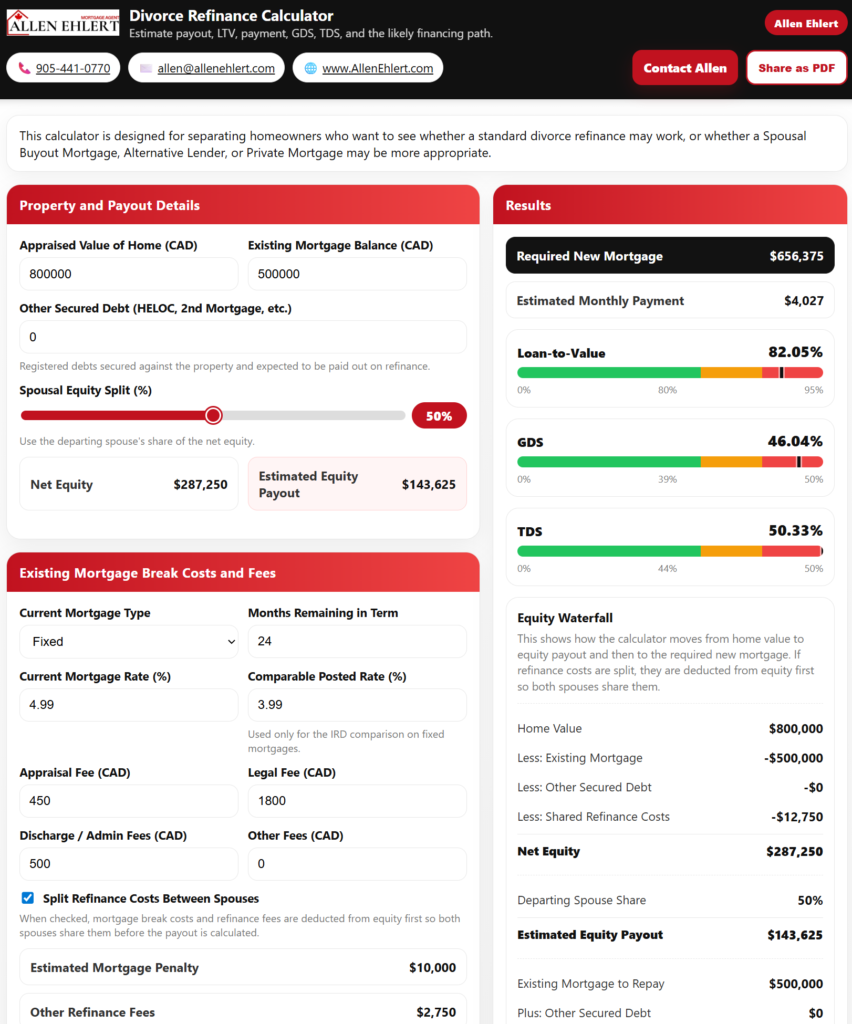

The Divorce Refinance Calculator

The Divorce Alternative Calculator

The Divorce Financing Ladder

When a couple separates and one person wants to keep the home, I typically look at solutions in a logical sequence. Think of it as a ladder—you start at the top with the easiest, cheapest option, and work downward if necessary.

Here’s how that ladder usually works.

Mortgage Assumption

The first, cheapest, and simplest option is called mortgage assumption.

This is when the lender allows one spouse to take over the existing mortgage while removing the other spouse from the loan. The interest rate, term, and conditions remain the same—you’re essentially stepping into the existing mortgage on your own.

Why this is attractive:

- No mortgage penalty

- No new mortgage application in many cases

- No refinancing costs

- You keep your existing rate

But there’s a catch.

The remaining spouse must qualify on their own income. If they can’t support the mortgage alone, the lender won’t allow the assumption.

Next, many lenders demand that the ‘leaving’ partner stay on the mortgage (like a co-signor) in case the ‘staying’ partner doesn’t pay. To my mind this essentially kills the idea of mortgage assumption.

Also, no lender is going to take on more risk. Only when someone’s financial position is stronger after the divorce (rare, but it can happen), and possibly the ‘staying’ partner has a lot of other business with the lender (hence it is the business relationship that is most important to the lender) that the lender says ‘OK’ to a mortgage assumptions and does a release covenant.

Now you can see why extremely few people can do a mortgage assumption. It is technically possible, so it is the first rung of the ladder.

That’s when we move down the ladder.

Divorce Refinance

If assumption isn’t possible, the next step is a Divorce Refinance. A Divorce Refinance is the most popular option sought by divorcing partners and their attorneys.

This involves breaking the existing mortgage and replacing it with a new one under a single borrower. The new mortgage pays off:

- The existing mortgage balance

- The equity owed to the departing spouse

- Any secured debts tied to the property

The benefit here is that the lender evaluates the scenario like a traditional refinance.

However, there are limits and costs.

You’ll need to get a professional appraisal (not a letter of opinion from a realtor) to determine the value of the home that you will need to pay for.

Since you are breaking a mortgage, you will be paying a mortgage penalty, which could be substantial… often in the tens of thousands if you are with a chartered bank.

It is common for realtor costs to be included in the discussion since you bought the home together; the costs of selling the home to bring the partners back to their original position are often included in the financing and payout.

Then there are other costs as well. Some are financed through the mortgage, others you pay afterwards if you are the partner ‘staying’.

Most lenders will only allow the mortgage (which is your mortgage portion, payout to the departing spouse, fees, penalties, and costs, etc.) to go up to 80% of the property’s value in a standard refinance.

The ‘staying’ spouse also must demonstrate they can afford the mortgage according to the lender’s rules.

After all of this (and it is considerable) if you can’t qualify, we move further down the ladder to a Spousal Buyout Mortgage.

Spousal Buyout Mortgage

This is where things get interesting.

A Spousal Buyout Mortgage is a special exception available in Canada during a legal separation or divorce. Under certain conditions, lenders may allow the mortgage to go up to 95% of the home’s value.

That extra flexibility often makes the difference between keeping the home and having to sell it.

To qualify, the situation usually requires:

- A formal separation agreement

- Verification of the equity payout

- Mortgage default insurance approval

- Strong enough income to support the payments

The big difference between a Divorce Refinance and a Spousal Buyout Mortgage is the requirement to pay default mortgage insurance on top of all the other costs because your new mortgage amount is more than 80% of the appraised value of your home.

A Spousal Buyout Mortgage solution is incredibly powerful—but not every scenario fits within the underwriting guidelines.

If you can’t demonstrate you can afford the home according to the lender’s and insurer’s rules (usually you have insufficient income or carry too much debt), or are underwater on your mortgage (you owe more than the home is appraised for) we move to the next step on the ladder: Divorce Alternative Mortgage.

Divorce Alternative Mortgage

If traditional lenders won’t approve the file, the next step is Alternative Lending.

Alternative lenders—often called “B lenders” (but they don’t like being called that because there is nothing ‘B’ or ‘not as good’ about them)—are more flexible when it comes to:

- Higher debt service ratios

- Complex income situations

- Credit challenges

- Recent financial disruptions

These mortgages usually come with slightly higher rates and fees, but they provide a bridge when prime lenders (like banks, credit unions, monoline lenders, etc.) say no.

The advantage of going with an Alternative lender is if you don’t have enough income or have too much debt for a prime lender, they may still consider you. You’ll have all the same costs to pay as with a Refinance Divorce, but you won’t have the default mortgage insurance premium to pay as with a Spousal Buyout Mortgage.

The disadvantage is that you’ll be paying higher rates, and there are usually borrower and lender fees.

The major problem is that your mortgage (which is your mortgage portion, payout to the departing spouse, fees, penalties, and costs, etc.) can’t be more than 80% of the appraised value of the home, and that can be what makes a Divorce Alternative Mortgage out of reach for some people.

Still, for many separating homeowners, this solution allows them to keep the home temporarily while rebuilding their financial position.

Divorce Private Mortgage

The final rung of the ladder is private lending.

Private lenders focus primarily on the equity in the property rather than strict income guidelines. This means they can approve scenarios that banks and alternative lenders cannot.

Private mortgages are typically short-term solutions to solve a particular problem, then move you up the mortgage ladder.

They’re often used to:

- Provide time for a property sale

- Stabilize finances after separation

- Allow a borrower to rebuild credit or income

While this option carries substantially higher rates and fees, it can be a crucial solution when someone needs time and flexibility during a major life transition.

The Divorce Refinance Calculator

My Divorce Refinance Calculator will help you discover what your buyout amount (or should I say possible amounts depending on what you negotiate) will be. Once you know the buyout amount, the next question becomes:

“Will I qualify for the new mortgage?”

That’s where my Divorce Refinance Calculator comes in.

The Divorce Refinance Calculator goes deeper by estimating:

- The required new mortgage

- The monthly payment

- Loan-to-value ratio

- Debt service ratios (GDS and TDS)

- Mortgage penalties and refinancing costs

Instead of guessing whether a refinance might work, the calculator shows you how lenders are likely to view the scenario.

This is incredibly helpful for realtors as well.

“Before we assume you have to sell the home, let’s see if refinancing could work.”

The Divorce Refinance Calculator will provide a final analysis to tell you your likely path, including which other rung on the ladder you are looking at.

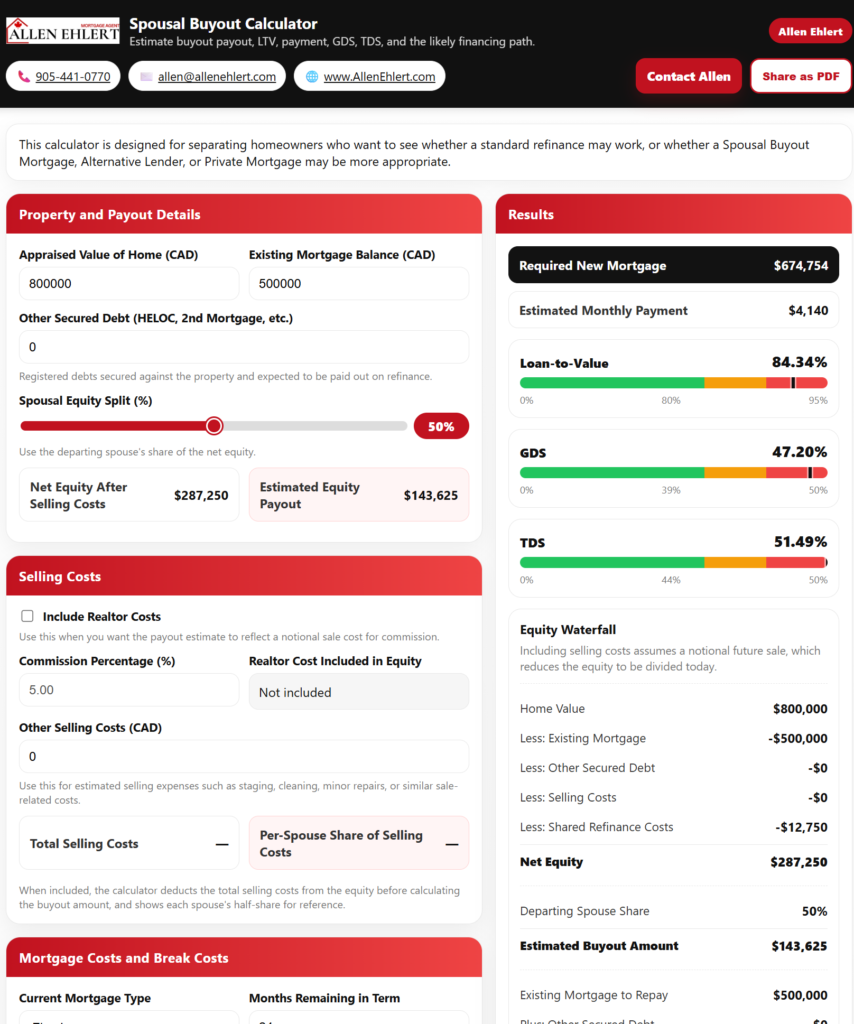

The Spousal Buyout Calculator

Not everyone can get a mortgage assumption or do a Divorce Refinance. One of the most common questions I hear is:

“How much would I actually need to buy out my spouse?”

That’s exactly what my Spousal Buyout Calculator is designed to answer.

My Spousal Buyout Calculator helps you estimate:

- The equity in the home

- The buyout amount owed to the departing spouse

- The potential mortgage required to keep the property

For clients, this calculator provides a quick way to test different scenarios.

With just a few numbers—home value, mortgage balance, and equity split—you can see the financial picture start to take shape.

I’ve coded my Spousal Buyout Calculator to provide a final analysis to determine your likely path, including which other rung on the ladder you are looking at if a Spousal Buyout Mortgage isn’t right for you, or it we can get you something better.

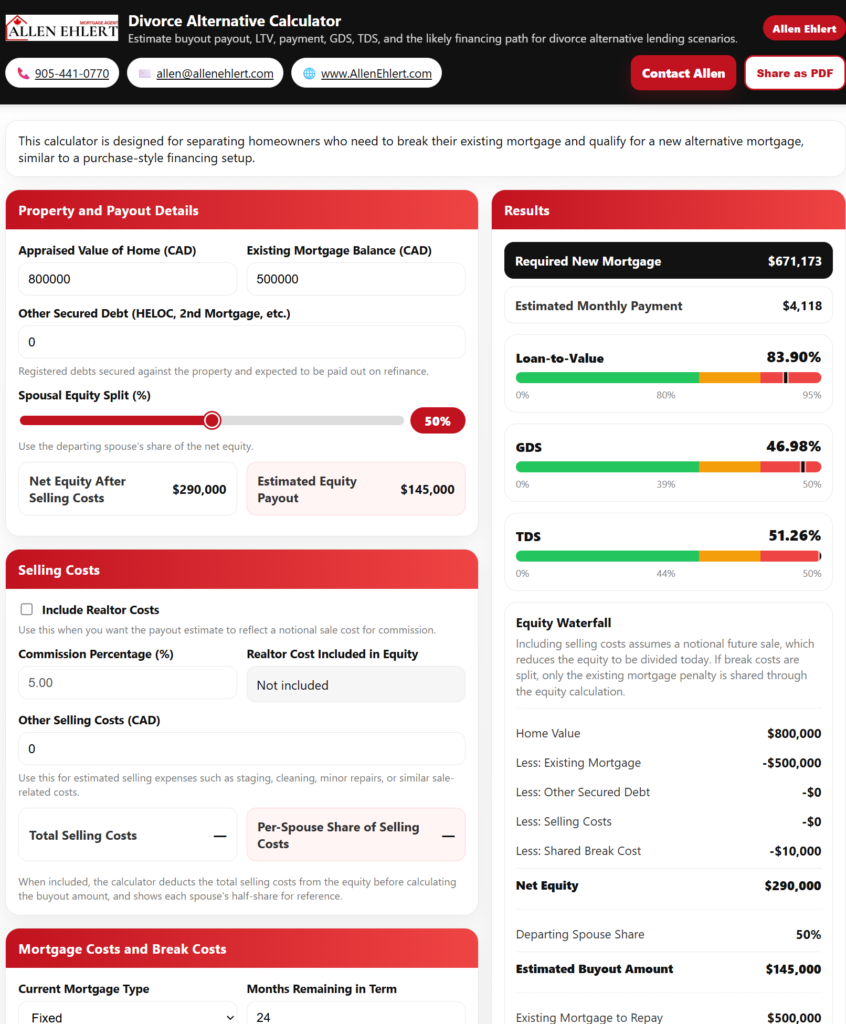

The Divorce Alternative Calculator

Sometimes the numbers don’t quite work with traditional or ‘prime’ lenders.

That’s where my Divorce Alternative Calculator becomes useful.

This tool models scenarios where:

- Alternative lenders may be required

- Mortgage penalties need to be factored in

- Selling costs are considered

- Broker and lender fees are included

It also estimates the cash required at closing, which is often the biggest surprise for clients during a refinance.

By using the Divorce Alternative Calculator, homeowners can explore whether alternative financing might allow them to stay in the home—even if the prime lending route doesn’t work.

A Story From the Real World

Let me give you a quick example.

A client once called me after a separation. She was convinced she would have to sell the house because her friends had told her that “banks never approve these situations.”

Her home was worth about $900,000 and the mortgage was roughly $550,000.

Using the calculators, we worked through the numbers together.

First we estimated the buyout.

Then we tested a refinance scenario.

Then we looked at a spousal buyout mortgage.

It turned out she did qualify.

Not only was she able to keep the home, but her monthly payment ended up lower than she expected.

The reality is that many homeowners assume the worst simply because they don’t know what their options are.

A few calculations can change that conversation entirely.

Allen’s Final Thoughts

Divorce is one of life’s most difficult transitions, and the financial decisions that come with it can feel overwhelming.

But here’s the good news: you don’t have to navigate it alone, and you don’t have to guess.

My Divorce Financing Ladder gives you a clear roadmap. We start with the simplest and least expensive solutions and work our way down only if necessary. Along the way, my calculators on my website help bring clarity to the numbers so you can see what might actually be possible.

If you’re a homeowner going through a separation—or a realtor helping clients in that situation—I’m here to help.

As a mortgage agent, I can:

- Analyze your buyout scenario

- Determine which rung of the financing ladder may work

- Structure refinance or buyout solutions

- Explore alternative and private lending options

- Work alongside your realtor and legal team

Sometimes the solution is refinancing.

Sometimes it’s alternative financing.

And sometimes, the best decision really is to sell and start fresh.

The key is understanding the numbers first.

That’s exactly why I coded up these calculators—and why I’m here to help you work through them.