When a relationship ends and one spouse wants to remain in the home, a divorce refinance is often one of the first financial solutions explored. The Divorce Refinance Calculator is designed to help you understand what that might look like financially before speaking with a lender.

This guide walks you through how to use the Divorce Refinance Calculator step-by-step, what each section means, and how to interpret the results so you can make informed decisions about keeping the home.

In this guide:

What This Calculator Is Designed to Do

Information You Will Need Before You Start

Existing Mortgage Break Costs and Fees

Understanding the Results Section

Tips for Using the Calculator Effectively

What This Calculator Is Designed to Do

The Divorce Refinance Calculator helps estimate whether refinancing the property into one spouse’s name is feasible. It analyzes the financial structure of a potential refinance and provides insight into:

- The equity payout to the departing spouse

- The new mortgage amount required

- Estimated mortgage payments

- Loan-to-Value (LTV) ratios

- Debt service ratios (GDS and TDS)

- The likely financing path

Instead of guessing whether keeping the home might work, the calculator translates the situation into numbers lenders actually review.

Information You Will Need Before You Start

To get meaningful results, it helps to gather the following information beforehand:

- Current appraised value of the home

- Remaining mortgage balance

- Any HELOC or second mortgages

- Expected equity split between spouses

- Current mortgage interest rate

- Months remaining on the mortgage term

- Estimated income and debts

- Property tax and heating costs

Even rough estimates are sufficient for a first analysis.

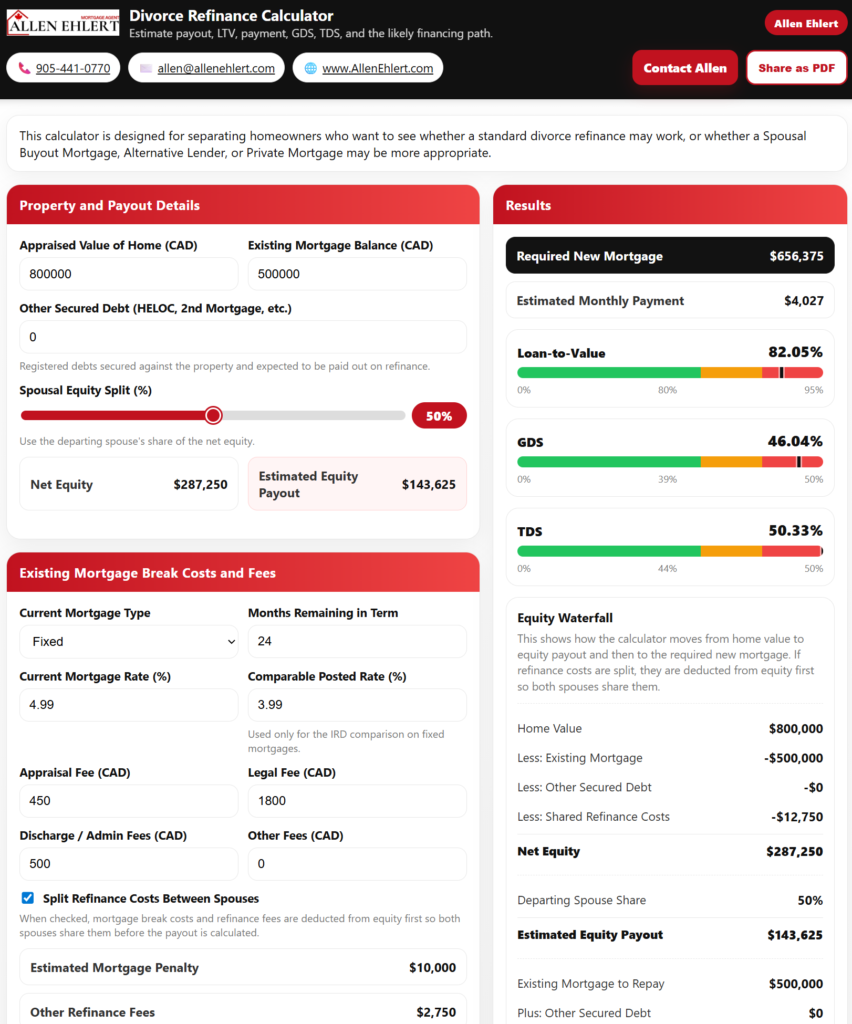

Property and Payout Details

This first section establishes the equity position in the home and estimates the payout required to buy out the departing spouse.

Appraised Value of Home

Enter the estimated or appraised value of the property.

If you do not have a formal appraisal, a recent market estimate from a realtor can be used as a starting point.

Existing Mortgage Balance

Enter the current outstanding mortgage balance.

This information can usually be found on your latest mortgage statement.

Other Secured Debt

Include any additional loans registered against the property such as:

- Home Equity Lines of Credit

- Second mortgages

- Private charges

These must typically be paid out as part of the refinance.

Spousal Equity Split

This slider determines what percentage of the equity is owed to the departing spouse.

Common examples include:

- 50% / 50%

- 60% / 40%

- Any negotiated arrangement in a separation agreement

Net Equity

The calculator subtracts mortgage balances and secured debts from the home value to estimate the equity remaining in the property.

Estimated Equity Payout

This amount represents the estimated buyout payment owed to the departing spouse.

Existing Mortgage Break Costs and Fees

Refinancing often requires breaking the existing mortgage, which may trigger penalties and additional fees.

Current Mortgage Type

Select whether your mortgage is:

- Fixed

- Variable

Penalty calculations differ depending on the mortgage type.

Months Remaining in Term

Enter the number of months left before your mortgage renews.

This information affects the penalty calculation.

Current Mortgage Rate

Enter the interest rate on your existing mortgage.

Comparable Posted Rate

For fixed mortgages, lenders often use the difference between the current rate and a comparable posted rate when calculating the Interest Rate Differential (IRD) penalty.

NOTE: Calculating exact mortgage penalties are extremely difficult as different lenders use different methods based on different figures. The calculator does it’s best to give you an estimate.

Refinance Costs

Additional refinancing expenses may include:

- Appraisal fees

- Legal fees

- Administrative discharge fees

- Miscellaneous costs

Split Refinance Costs Between Spouses

When enabled, the calculator deducts refinance costs from the equity before calculating the payout.

This means both spouses share the costs proportionally.

If disabled, the spouse keeping the home absorbs the refinance costs.

Estimated Mortgage Penalty

The calculator estimates the cost of breaking the current mortgage. It can never be definitive.

Total Costs

This shows the combined estimate of penalties and refinance expenses.

New Refinance Assumptions

This section models what the new mortgage might look like.

New Refinance Interest Rate

Enter the estimated interest rate for the new mortgage.

See my Rates page as a starting point: Rates & Statistics – Allen Ehlert | Mortgage Agent

Amortization Period

Select the amortization period using the slider.

Common options include 25 years or less.

A longer amortization reduces the monthly payment but increases total interest over time.

Income and Property Costs

Lenders assess whether the remaining spouse can afford the new mortgage using debt service ratios.

Gross Annual Income

Enter your total annual income before taxes.

Other Monthly Debt Payments

Include obligations such as:

- Car loans

- Credit card minimums

- Student loans

- Personal loans

Property Taxes

Enter the annual property tax amount.

Heating Costs

This represents the estimated monthly heating expense.

Many lenders assign a value between $150 to $200 a month for heating costs when calculating housing affordability.

Understanding the Results Section

After entering the information, the calculator generates several key outputs.

Required New Mortgage

This is the estimated mortgage amount required to:

- Pay off the existing mortgage

- Pay out the departing spouse

- Cover refinance costs

Estimated Monthly Payment

This shows the projected monthly mortgage payment based on the interest rate and amortization selected.

Loan-to-Value (LTV)

Loan-to-Value compares the new mortgage size to the property value.

Example:

Home Value: $800,000

Mortgage: $640,000

LTV = 80%

Most lenders require 80% or lower for a Divorce Refinance.

The gauge in the calculator visually shows whether the LTV falls within acceptable ranges.

GDS and TDS Ratios

These ratios measure mortgage affordability.

Gross Debt Service (GDS)

GDS measures housing costs relative to income.

Typical guideline: 39% or lower

Total Debt Service (TDS)

TDS includes housing costs plus other debts.

Typical guideline: 44% or lower

These ratios help determine whether the refinance may qualify with prime lenders.

Equity Waterfall

One of the most helpful features in the calculator is the Equity Waterfall.

This section visually shows how the numbers flow from:

- Home value

- Existing mortgage

- Other debts

- Refinance costs

- Equity payout

This step-by-step breakdown helps users understand exactly how the refinance amount is calculated.

Recommended Path

Based on the LTV and debt ratios, the calculator suggests a likely financing direction.

Possible outcomes include:

- Standard divorce refinance

- Spousal buyout mortgage

- Alternative lender financing

- Private mortgage solutions

This guidance helps users understand where they may fall within the divorce financing ladder.

Example Scenario

Imagine a homeowner named Sarah.

Her situation looks like this:

Home value: $850,000

Mortgage balance: $520,000

Equity split: 50%

Income: $135,000

After entering the numbers into the calculator, Sarah discovers:

- Her buyout payment would be about $165,000

- The required new mortgage would be about $700,000

- Her LTV would remain under 80%

This means a Divorce Refinance may be possible, allowing her to keep the home.

Without running the numbers, Sarah might have assumed selling was her only option.

Tips for Using the Calculator Effectively

For the most useful results:

- Use realistic property value estimates

- Include all secured debts

- Enter accurate income information

- Test multiple interest rate scenarios

- Adjust amortization to explore payment differences

Many users run several scenarios to understand the full range of possibilities.

Contact Me

While the calculator provides valuable insight, it is still an estimate tool.

IMPORTANT: No Calculator can replace professional underwriting!

There are many lenders who take different approaches and use different numbers, we call this lender policies. Moreover, lenders are constantly changing their rates and their policies. Furthermore, lenders frequently grant exceptions to their rules and policies.

This is why, when you are ready, you need to contact me.

Actual mortgage approval depends on additional factors including:

- Credit history

- Employment stability

- Documentation

- Government legislation and guidance

- … and much, much more!

I analyze your full situation and working with you determine the most appropriate, suitable financing strategy for your situation.

Allen’s Final Thoughts

A divorce refinance can feel overwhelming at first because there are so many moving pieces. The Divorce Refinance Calculator helps simplify the process by turning a complex financial situation into a clear set of numbers.

By estimating the equity payout, refinance costs, mortgage size, and affordability ratios, the tool gives separating homeowners a practical starting point for understanding their options.

If you find yourself navigating a separation and trying to determine whether keeping the home is possible, running the numbers through this calculator is often the best first step. From there, a mortgage professional can help guide you through the next stage and identify the most appropriate financing path for your situation.