…What Goes On Behind the Scenes

When I help you with a second mortgage, I want you to understand something:

This is not a quick add-on.

I don’t treat it like a simple top-up or shortcut.

I treat it as a full mortgage file, with structure, risk analysis, and a clear strategy—because that’s what protects you and ensures the solution works.

There’s a process I follow every time, and every step has a purpose.

Here’s how I approach it.

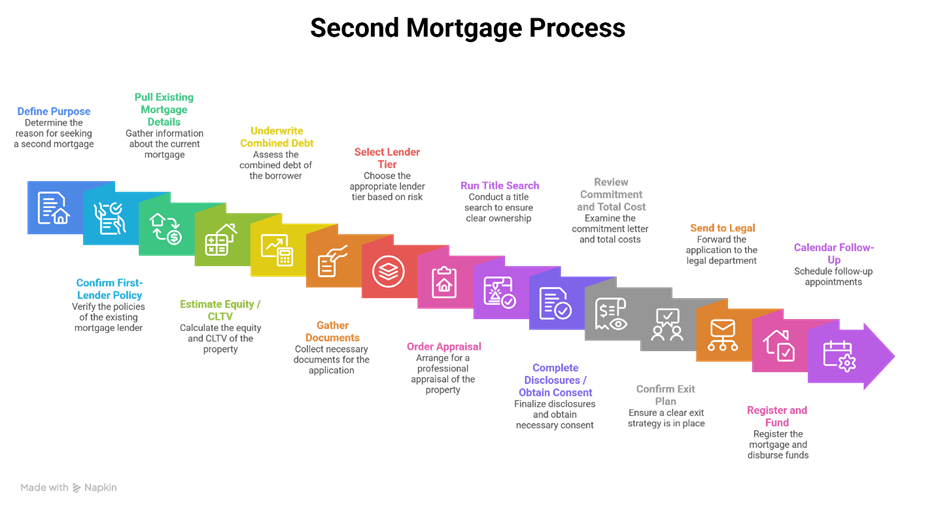

Step 1: I Start With the Purpose

Step 2: I Confirm Whether Your First Mortgage Even Allows It

Step 3: I Pull All the Details on Your Existing Mortgage

Step 4: I Calculate Your Equity and Set Realistic Limits

Step 5: I Underwrite the Full Picture—Not Just One Loan

Step 6: I Build a Complete Document File Early

Step 7: I Choose the Right Lender Tranche

Step 8: I Order an Appraisal to Confirm Value

Step 9: I Review Title and Existing Charges

Step 10: I Disclose Everything Properly

Step 11: I Walk You Through the Full Cost—Not Just the Payment

Step 12: I Define Your Exit Strategy

Step 13: I Coordinate Legal and Registration

Step 14: Funding After Conditions

Step 15: I Stay Involved After Closing

Step 1: I Start With the Purpose

Before we talk about lenders, rates, or approvals, I need to understand:

Why are you looking at a second mortgage?

Is it for:

- Debt consolidation

- Renovations

- Tax arrears

- Business purposes

- A buyout

- Reimbursing a down payment

- Or something else entirely

This matters because lenders don’t just look at whether you can afford the loan—they look at whether the use of funds makes sense from a risk perspective.

If the purpose isn’t clear or justified, the deal becomes much harder to structure properly. FSRA’s consumer guidance says the process starts with reviewing the borrower’s criteria and selecting a suitable lender based on the actual need. (fsrao.ca)

Step 2: I Confirm Whether Your First Mortgage Even Allows It

Before I go any further, I review your existing mortgage, charge terms, or lender policy to confirm whether a second mortgage is permitted

I look at:

- The lender

- The mortgage terms

- The charge structure

- Whether it’s insured

- Whether secondary financing is allowed

This step alone can stop a deal. This is critical because some first lenders will not allow subordinate financing, and insured mortgages have especially strict risk controls. On insured files, the mortgage insurer’s position and guidelines are a major constraint. (fsrao.ca)

Bottom line is that many lenders, especially prime lenders, simply do not allow second mortgages behind their position.

If we don’t confirm this early, we risk building a structure that can’t legally be completed.

Step 3: I Pull All the Details on Your Existing Mortgage

I need a full picture of what’s already in place.

That includes:

- Current balance

- Monthly payment

- Interest rate

- Maturity date

- Potential penalties

- Type of mortgage (collateral, standard, readvanceable, etc.)

I need the existing lender name, balance, payment, maturity date, penalty exposure, product type, and whether there is a collateral charge or readvanceable feature. Lenders may require your current mortgage details, including balance, term length, and amortization period, before approving additional equity-based borrowing.

This isn’t just for documentation—it’s for strategy.

Because how your current mortgage is structured directly affects what we can do next.

Step 4: I Calculate Your Equity and Set Realistic Limits

Next, I determine how much equity is actually available.

I determine the property value, subtract the existing first mortgage, and determine the maximum combined loan-to-value you can support. This tells me whether a second is realistic. A HELOC combined with a mortgage requires at least 20% equity, while a standalone HELOC requires more than 35% equity; that gives a useful benchmark for how lenders think about available equity.

I:

- Estimate or confirm the current property value

- Subtract your existing mortgage

- Calculate your combined loan-to-value (CLTV)

This tells us:

Is a second mortgage even realistic?

And more importantly:

How far can we go without putting you in a risky position?

Step 5: I Underwrite the Full Picture—Not Just One Loan

I don’t look at your first mortgage in isolation.

Do not look only at the first mortgage payment. I add the projected second-mortgage payment, property taxes, heating, condo fees if applicable, and all other debt. Residential underwriting guidance emphasizes sound underwriting practices and risk controls, which in practice means you have to work on your combined debt picture, not just your mortgage in isolation.

I look at:

- First mortgage payment

- Proposed second mortgage payment

- Property taxes

- Heating

- Condo fees (if applicable)

- All other debts

Because lenders look at your total obligations, not just one piece of the puzzle.

If the combined structure doesn’t work, the deal doesn’t work, and you won’t be approved.

Step 6: I Build a Complete Document File Early

Before I approach any lender, I make sure everything is in place.

I gather ID, income documents, current mortgage statement, property tax bill, proof of home insurance, a copy of the existing mortgage charge if needed, and support for the use of funds. Sorry, I know, that’s a lot of documents.

If the second is for renovation or consolidation, I document that clearly. FSRA’s mortgage-application guidance and consumer guidance both reinforce that licensed mortgage professionals should gather the borrower’s criteria and documentation before selecting the lender. (fsrao.ca)

That includes:

- Identification

- Income documentation

- Mortgage statement

- Property tax bill

- Insurance

- Supporting documents for the use of funds

This step is about control.

It allows me to:

- Present your file properly

- Avoid delays

- Position the deal with the right lender from the start

Step 7: I Choose the Right Lender Tranche

This is one of the most important parts of what I do.

If your file is very strong and the second is small, a prime lender may work. If ratios are tighter, credit is bruised, or the purpose is more complex, you may need a B lender or private lender. As FSRA has flagged private mortgages as an elevated consumer-protection priority, I am especially careful on cost, disclosure, and suitability when the file moves into private money. (fsrao.ca)

So I don’t send your file just anywhere.

I decide:

- Is this an A lender scenario?

- Does it fit a credit union?

- Is this better suited for a B lender?

- Or does it require private (MIC) financing?

That decision is based on:

- Your profile

- The structure

- The purpose

- The risk

Because sending a deal to the wrong lender wastes time and kills momentum.

Step 8: I Order an Appraisal to Confirm Value

Once the structure makes sense, I order an appraisal. This confirms value and protects you from structuring a second on guessed equity. Appraisal fees are among the typical costs when borrowing against home equity, and lenders commonly require an appraisal before approval.

This is critical.

It:

- Confirms the property value

- Protects you from overleveraging

- Validates the entire deal

I never rely on guesswork, or a realtor’s ‘letter of opinion’ when it comes to equity. When must know what it’s worth from a professional appraiser.

Step 9: I Review Title and Existing Charges

I make sure we understand exactly what’s on title. This requires a confirmation of ownership, legal description, existing charges, any secured lines, construction liens, matrimonial interests where relevant, and whether there is already a second charge on title. Title search and title insurance are common costs in home-equity borrowing, and title-related issues can derail closing if they are discovered too late.

That includes:

- Existing mortgages

- Secured lines of credit

- Any liens

- Ownership structure

- Legal considerations

Because issues here can stop a deal at the last minute if they’re not caught early.

Step 10: I Disclose Everything Properly

I ensure disclosures are complete and the borrower understands the costs, ranking, risks, and exit. FSRA regulates mortgage brokering in Ontario and expects licensed professionals to follow the applicable consumer-protection and conduct requirements. (fsrao.ca)

If the first lender requires consent, I get it.

I make sure:

- The structure is fully disclosed

- You understand the ranking (first vs second)

- You understand the risks

- Everything is compliant

This protects you—and it protects the deal.

Step 11: I Walk You Through the Full Cost—Not Just the Payment

Before you sign anything, I go through:

- Interest rate

- Lender fees

- Broker fees

- Legal costs

- Appraisal costs

- Payment structure (interest-only vs amortized)

- Penalties

Because the monthly payment is only part of the story.

You need to understand the total cost and how it fits your plan.

Step 12: I Define Your Exit Strategy

A second mortgage should have a clear repayment plan: refinance, sale, bonus, debt repayment program, settlement proceeds, or maturity of another obligation. This is especially important if the file is private or short-term, because regulators have highlighted consumer risks in that segment. (fsrao.ca)

Before we proceed, I want a clear answer to:

How does this get paid off?

That might be:

- Refinancing later

- Selling the property

- Increasing income

- Paying down debt

A second mortgage without an exit strategy is not a solution—it’s a risk.

Step 13: I Coordinate Legal and Registration

The lawyer or notary handles the mortgage instructions, title work, registration, and payout or disbursement conditions. Using a lawyer or notary is required to register the home as collateral.

I work with the lawyer to ensure:

- The mortgage is structured correctly

- The charge is registered properly

- All conditions are met

This is where everything comes together.

Step 14: Funding After Conditions

This usually means a signed commitment, satisfactory appraisal, clear title, insurance confirmation, legal completion, and any first-lender consent if needed. At that point, the second mortgage is registered, and funds are released through legal.

Funds are only released once:

- The appraisal is complete

- Title is clear

- Insurance is confirmed

- All documents are signed

- Any required lender consent is in place

Step 15: I Stay Involved After Closing

My job doesn’t end when the deal funds. I diary the maturity date, renewal window, and refinance review date. If the second is being used as a temporary solution, you should know the next step well before maturity.

My job doesn’t end when the deal funds.

I:

- Track your maturity date

- Plan your refinance window

- Revisit your strategy before the term ends

Because a second mortgage is often temporary by design.

And the next step matters just as much as this one.

Why This Process Matters

The biggest mistakes I see are:

- Skipping lender restrictions

- Assuming equity without confirming value

- Treating a second mortgage as permanent

- Not having a clear exit

That’s how deals go wrong.

Allen’s Final Thoughts

From your perspective, this might feel like a lot.

From my perspective, this is what ensures:

- The deal is structured properly

- The risks are controlled

- The outcome works for you—not just today, but later

Because a second mortgage isn’t just about accessing equity.

It’s about structuring it the right way, at the right time, with a clear plan.