… “Wait—You Need Permission for That?”

Introduction (Client Conversation Style)

If you’re thinking about adding a second mortgage, there’s something important we need to talk about—because this is where a lot of people get caught off guard and because not everyone out there ‘follows the rules’.

Most clients assume you can just go ahead and place a second mortgage behind your existing one. Fair enough—it sounds simple. But here’s the catch: your current lender actually has a say in that. In many cases, we need to get what’s called a Consent to Second Mortgage, which is basically your first lender giving permission for another loan to sit behind theirs.

Now, if we don’t address this early, it can slow things down or even derail a deal entirely (or worse)—and that’s the last thing I want for you. My job is to see these things coming before they become a problem, so we can structure everything properly from the start and keep things moving smoothly.

What We’re Going to Cover

What a Consent to Second Mortgage actually is

Other terms clients might hear

Why the ‘Consent to Second Mortgage’ document matters

How different lenders handle second mortgage consent

A quick story to bring it all together

What Is a Consent to Second Mortgage?

At its core, a Consent to Second Mortgage is exactly what it sounds like:

Your first mortgage lender is giving you written permission to place another mortgage behind them on title.

Think of it like this—your first lender is in first position, meaning they get paid first if anything goes sideways. When you introduce a second mortgage, you’re adding another lender behind them, which increases risk.

So the first lender essentially says:

“Alright, we’ll allow it—but only under our terms.”

Without that consent, you could actually be breaching your mortgage agreement, which is the last thing you want.

When Do You Need One?

You’ll typically need a Consent to Second Mortgage anytime:

- You’re adding a second mortgage behind an existing first

- The first mortgage is not being refinanced or replaced

- The existing lender has restrictions on additional financing (which most do)

A simple way to think about it:

If the first mortgage is staying in place and you’re layering debt behind it…you almost always need consent.

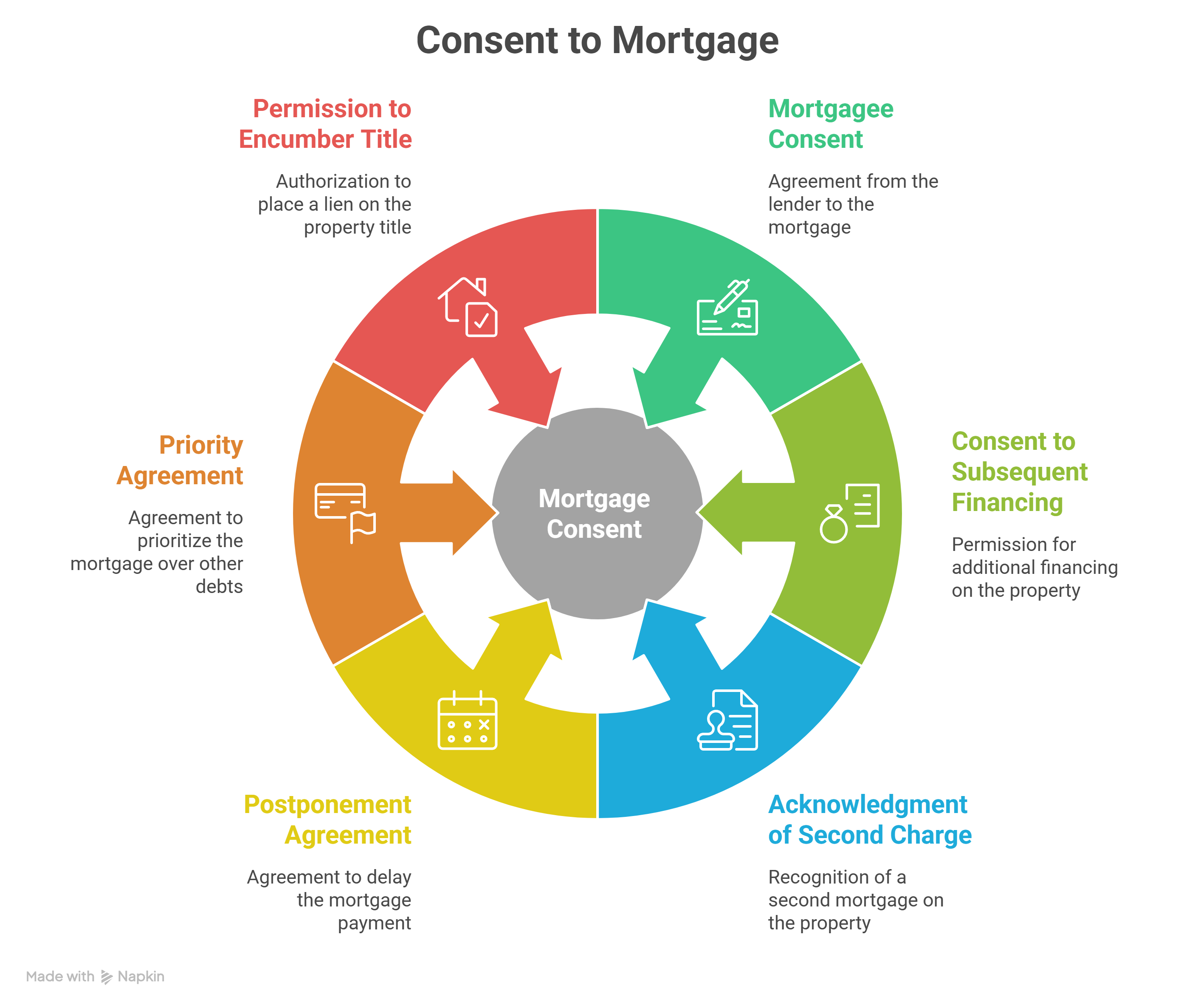

Other Terms Clients Might Hear

This is where confusion creeps in. Different lenders and lawyers love different terminology.

You might hear:

- Mortgagee Consent

- Consent to Subsequent Financing

- Acknowledgment of Second Charge

- Postponement Agreement

- Priority Agreement

- Permission to Encumber Title

Same idea, different labels.

If it sounds official and slightly intimidating… it’s probably the same thing.

Why the ‘Consent to Second Mortgage’ Document Matters

This isn’t just paperwork—it’s risk control.

Here’s why it matters:

- The first lender is protecting their priority position

- They’re ensuring the borrower isn’t becoming overleveraged

- They’re preventing situations where a second lender complicates enforcement

But here’s the real-world impact:

If you skip this step or assume it’s not needed:

- Deals can get declined late in the process

- Lawyers may refuse to close

- The first lender could technically call the mortgage

In other words, it’s not just a form—it’s a gatekeeper.

How Different Lenders Handle Second Mortgage Consent

This is where experience really matters. Not all lenders play the game the same way.

Big Banks (Rigid and Protective)

Think Royal Bank of Canada or TD Canada Trust.

- Typically restrict or outright decline

- Prefer (OK… Demand) you refinance with them instead

- May allow it only under low LTV and strong profiles

Translation: “We’d rather control the whole deal.”

Monoline Lenders (Practical but Policy-Driven)

Examples include First National Financial LP and MCAP.

- Review on a case-by-case basis

- Focus on:

- Combined LTV

- Debt serviceability

- Purpose of funds

Translation: “Convince us this still makes sense.”

Credit Unions (Relationship-Focused)

Such as Meridian Credit Union.

- More flexible and human-driven

- Decisions often influenced by:

- Member relationship

- Story behind the deal

Translation: “Let’s talk it through.”

Private / MIC Lenders (Flexible but Strategic)

Like Ginkgo MIC or Tembo Financial.

- Most open to layered financing

- Focus heavily on:

- Exit strategy

- Property value

- Overall deal structure

Translation: “If the numbers work, we’re in.”

How You Can Use This

Let’s say you want funds for:

- Renovations

- Investing

- Debt consolidation

Before you assume a second mortgage is easy:

- First, check your existing mortgage terms

- Second, understand your lender’s stance

- Third, structure and cost it properly from the start

Because the cheapest first mortgage isn’t always the most flexible one.

A Story From the Field

I once worked with a client—we’ll call him Mike.

Mike had a great rate with a major bank and didn’t want to touch it. He needed $80,000 for renovations and figured a second mortgage was the perfect solution.

Sounds simple, right?

Well… not quite.

When he submitted for a second mortgage, everything looked clean—and then came the curveball:

The first lender refused consent.

Now he had a choice:

- Abandon the deal

- Or restructure everything

He ended up refinancing instead, which solved the problem—but it delayed the timeline and substantially increased costs.

The lesson? If he had checked the lender’s policy upfront, he could have structured it properly from day one.

Allen’s Final Thoughts

A Consent to Second Mortgage might seem like a small technical detail—but in reality, it’s one of those pivotal pieces that can quietly determine whether your deal moves forward or falls apart.

When you understand how lenders think, how risk is evaluated, and when consent is required, you stop reacting to problems and start anticipating them. That’s where real confidence—and real value—comes from.

And here’s the thing—you don’t have to figure this out on your own.

As a mortgage agent, this is exactly where I step in:

- I review your existing mortgage terms before issues arise

- I structure deals based on lender behaviour—not guesswork

- I communicate with lenders to position your file properly

- I help realtors keep deals together and clients informed

- I create strategies when the obvious path doesn’t work

Whether you’re a client trying to access equity or a realtor trying to keep a deal alive, my role is simple:

Make the complex clear—and keep your dreams moving forward.