… Know the Door Out Before You Walk In

When you’re looking at a Private or Heavy Alt mortgage, it’s easy to zero in on the approval and feel relieved once somebody says yes. But in my part of the mortgage world, the real question is not just can you get in—it’s how are you getting out?

An exit strategy is a plan developed and assessed when the loan is originated, with the goal of moving you into conventional financing or allowing the property to be sold without delinquency. Because Private and Alternative mortgages are more expensive than prime mortgages and often structured as interest-only loans, they are a short-term bridge rather than a long-term home for your debt. In short, if the mortgage is the bridge, the exit strategy is the other side of it.

Allow me to discuss exit strategies:

Why It Matters Before You Sign

A Scenario That Brings It Home

What an Exit Strategy Means

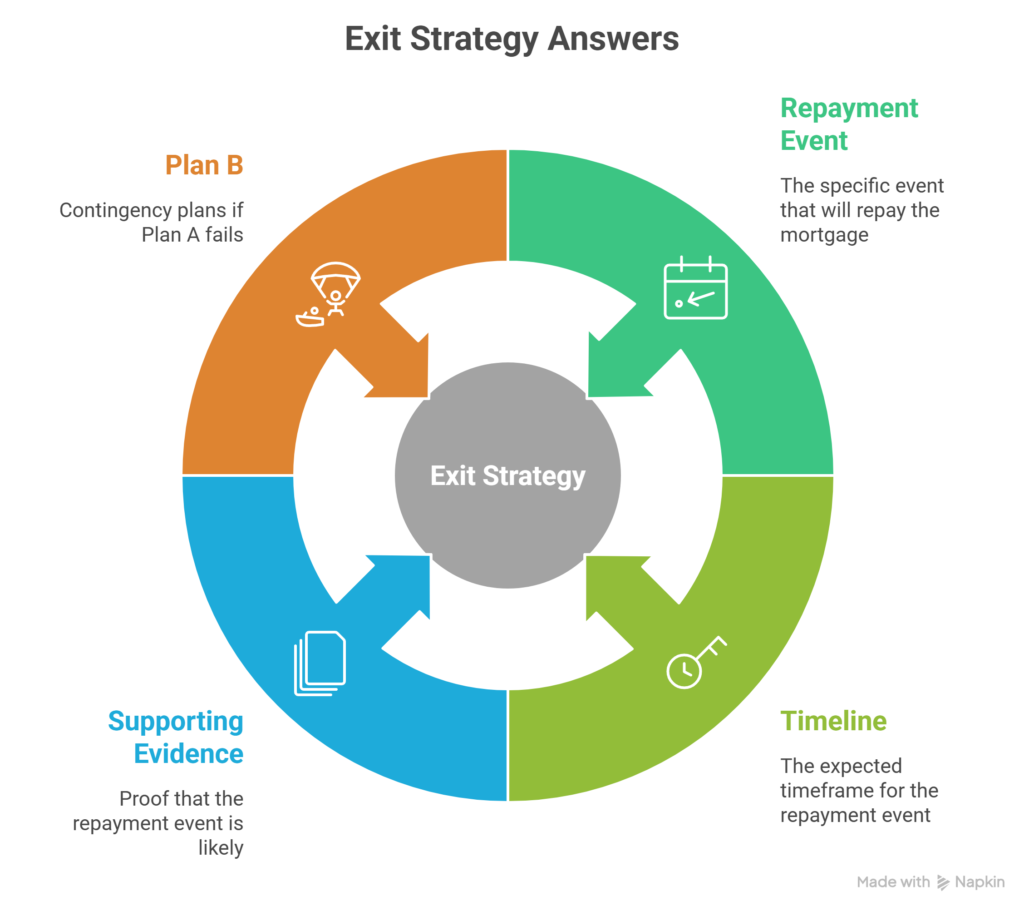

In simple terms, an exit strategy answers the question, how are you going to pay back and get out of this expensive mortgage? For my financial expert friends, an exit strategy is the documented repayment path attached to the file before funds advance. It answers four questions:

- What event repays the mortgage

- When that event should happen

- What evidence supports it

- What happens if Plan A slips

Your exit plan is assessed by your lender when you get your loan (at origination as part of underwriting). A lender’s decision to give you Private or Alternative financing should rest primarily on your willingness and capacity to service debt, not blind faith that the property alone will save the file (aka sell your house or go Power of Sale).

That is exactly why an exit strategy matters so much in Private and Heavy Alt lending. CMHC says Alternative lenders often approve mainly on the strength of property equity and short-term cash flow, and they commonly serve self-employed borrowers, people with bruised or thin credit, and borrowers with short-term cash needs. Most Private lenders will ask me to spell out whether the payoff will come from a refinance, a sale, or another identifiable source of funds, such as an inheritance, settlement, or asset sale. If you cannot describe the path out in black and white, the deal may still get discussed, but it usually gets shakier, pricier, or both.

Put another way, the Private mortgage is supposed to be the pit stop, not the whole race. If the plan is basically “we’ll figure it out later,” that is not an exit strategy. That is just wishful thinking wearing a sport coat … and hope is not a strategy.

Why It Matters Before You Sign

It matters because of cost. Interest is the fee you pay to borrow money, that renewals can change your payment amount, and even small rate differences can materially affect what you pay over time. Since Private and Alternative mortgages are more expensive and often interest-only, you can see why “I’ll deal with it later” is not a harmless delay. It can become a very expensive shrug.

The consequences are real, not theoretical. In CMHC’s Ontario study, published in 2022 using 2020 and early 2021 data, only 72% of Alternative mortgage borrowers had what CMHC called an effective exit: 63.6% switched to a conventional lender, and 8.5% sold the property without default or foreclosure. But 27.8% stayed in the Alternative space, and CMHC warned that weaker exit performance can create long-term affordability strain because borrowers remain in higher-cost debt longer than intended.

It matters for underwriting, too. If your exit depends on raising the balance, stretching the amortization, or materially restructuring the file, you should treat that as a fresh underwriting event. Switching or breaking a mortgage can trigger setup, discharge, appraisal, and administration costs, and that prepayment penalties can cost thousands if you exit early without understanding the contract. In the Private space, renewal files may also bring updated valuation, legal work, and lender or broker fees.

Before you take a higher-cost short-term mortgage, you want to know whether the exit is realistic, documented, and timed properly. If not, the “temporary” solution can get sticky in a hurry.

The Exit Strategies

Below are the common exit routes when a file is built properly.

Refinance to a conventional lender after fixing a temporary problem.

This is the classic exit when the real issue is time. You need to clear arrears, reduce unsecured debt, rebuild credit, return to work, or produce cleaner income documentation. Example: You use a 12-month Private mortgage to pay out a maturing lender and stabilize the file, then move into a conventional mortgage once your debt ratios and income documents are back where they need to be.

Refinance first to a lower-cost Alternative or B lender, then graduate again later.

Sometimes one jump is too big. A borrower may need Private money for speed or flexibility, then step down into a lower-cost non-prime lender once the file is more documentable.

Example: A self-employed buyer closes quickly with Private funds, then refinances into a B-lender product a few weeks later once the urgent closing is behind them and the paperwork is complete.

Sell the property.

CMHC counts a sale without delinquency as an effective exit, and Canadian lender guidance regularly lists a sale as a primary payoff path.

Example: You take a short Private mortgage to finish light renovations, list the property, and repay the lender from the sale proceeds before extension fees ever enter the chat.

Use another asset or incoming cash event.

Some files are built around a known liquidity event, such as an inheritance, a legal settlement, liquidating an investment, or selling another property.

Example: You borrow against your home for nine months and pay the lender out when a cottage sale closes or investment proceeds become available.

Bridge one closing date to another

This works when the money is coming from a sale, but the dates do not line up neatly.

Example: You buy the next home before the current one closes, use a short bridge-style mortgage for the gap, and repay it from the proceeds once the old home closes.

Renovate, stabilize, or complete the project, then refinance or sell.

This is common in flip, BRRR, interim-purchase, and stabilization files. The Private or Alternative loan buys time for value creation or project completion, and the exit is either a refinance on the improved value or a sale.

Example: An investor buys a tired duplex, renovates and rents it, then refinances into a lower-cost hold mortgage after the work is done and the income is stabilized.

The common thread in every good strategy is that the payout event is specific. Not fuzzy. Not “probably.” Not “we’re pretty sure.” Specific.

A Scenario That Brings It Home

One of the easiest ways to see the difference between a good exit and a bad one is to look at a self-employed file, because CMHC identifies self-employed borrowers as a common Alternative-lending profile, and Canadian lender guidance often asks for evidence such as filed returns, debt targets, budgets, and documented timelines.

Think of this as a composite example. You own a landscaping company. The house has solid equity, but your taxable income looks skinny because you write off everything you legally can, and your bank renewal lands with a thud. A Private lender is willing to help, but only because the way out is dead simple and written down from day one: use the Private funds to pay out the maturing mortgage and stabilize short-term pressure, file two clean returns, keep business deposits consistent, and submit the refinance file at month 10.

Your accountant tidies the paperwork, I calendar the checkpoints, and your realtor is kept warm as Plan B in case the refinance misses. By the time the term matures, you are not scrambling with your hair on fire. You are moving into a lower-cost lender because the exit was built before the Private mortgage ever funded.

That is what a real exit looks like: not vibes, not hope, but a timed, documented plan with a backup.

How We Put This Into Practice

Here is what putting this into practice actually looks like.

- Name the repayment trigger. Is the exit a sale, a refinance, an inheritance, a bridge payout, or a project completion? If you cannot say exactly what repays the loan, the strategy is still too fuzzy.

- Collect proof, not just optimism. That proof may be filed tax returns, business statements, listing documents, appraisal targets, settlement paperwork, or evidence that another asset is being sold. Transparent files tend to get better terms, fewer conditions, and cleaner underwriting.

- Underwrite the takeout mortgage before you actually need it. If the plan is a refinance or equity takeout, assume the next lender will treat it like a fresh file and underwrite it accordingly.

- Put every professional in their lane early. Your accountant can clean up income reporting, your financial planner can confirm when funds from a sale, settlement, or liquidation will actually be available, your realtor can prepare the sale timeline if the property must be listed, your lawyer can flag title or contract issues, and you as the client can protect the file by avoiding unnecessary new debt and delivering documents quickly. As your coordinator, I’ll help you with all this.

- Set checkpoints before maturity. A practical rhythm is to review the file at 90, 60, and 30 days before the term ends, because renewals and lender changes can involve approvals, statements, fees, appraisals, and legal paperwork. I recommend shopping around a few months before the end of the term rather than waiting until the renewal letter shows up.

- Cost out Plan B. If the refinance is late or the sale slips, know the price of an extension, a renewal, or an early payout. Those prepayment penalties can cost thousands, and Private renewals may add fresh valuation, legal, lender, or broker costs.

When this is done well, you are not guessing when cash will arrive, the accountant is not rushing returns two weeks before maturity, the realtor is not being asked to perform miracles at the eleventh hour, and you are not stuck renewing an expensive mortgage because nobody owned the timeline. That’s how I turn a Private or Heavy Alt mortgage from a panic move into a planned transition.

Allen’s Final Thoughts

A Private or Heavy Alt mortgage should solve a problem, not become a lifestyle. A real exit strategy is specific, documented, time-bound, and supported by evidence. The safest short-term mortgage is the one that already knows how it gets paid out.

As your mortgage agent, I’m here to help you pressure-test whether Private or Heavy Alt financing is the right move in the first place, compare lenders and structures, explain the real cost of rates, fees, and penalties, build the exit strategy in plain English, and coordinate the moving parts with your accountant, realtor, lawyer, and financial planner. I can help you map the timeline, gather the right documents, stress-test Plan A against Plan B, and tee up the takeout mortgage well before maturity.

You do not have to white-knuckle this on your own. Let me help you solve today’s financing problem without losing sight of tomorrow’s best outcome.