When securing a mortgage in Canada, most borrowers focus on interest rates, amortization periods, and lender terms. However, an often-overlooked distinction—whether a mortgage is registered as a collateral charge or a standard charge—can have significant implications for future financing flexibility, refinancing, and legal costs. Understanding the key differences between these two mortgage types ensures borrowers make an informed decision that aligns with their long-term financial goals.

Making things worse, when shopping for a mortgage, it is not immediately clear whether a mortgage being offered is a collateral mortgage or a standard mortgage; it certainly isn’t presented in the name. Making things worse still, is that all lender’s mortgage offerings are different making comparison extremely difficult. Lastly, collateral mortgages are extremely complicated financial vehicles and the people who sell them often don’t know the product very well themselves.

What is a Collateral Mortgage?

Which Mortgage Type is Right for You?

What is a Standard Mortgage?

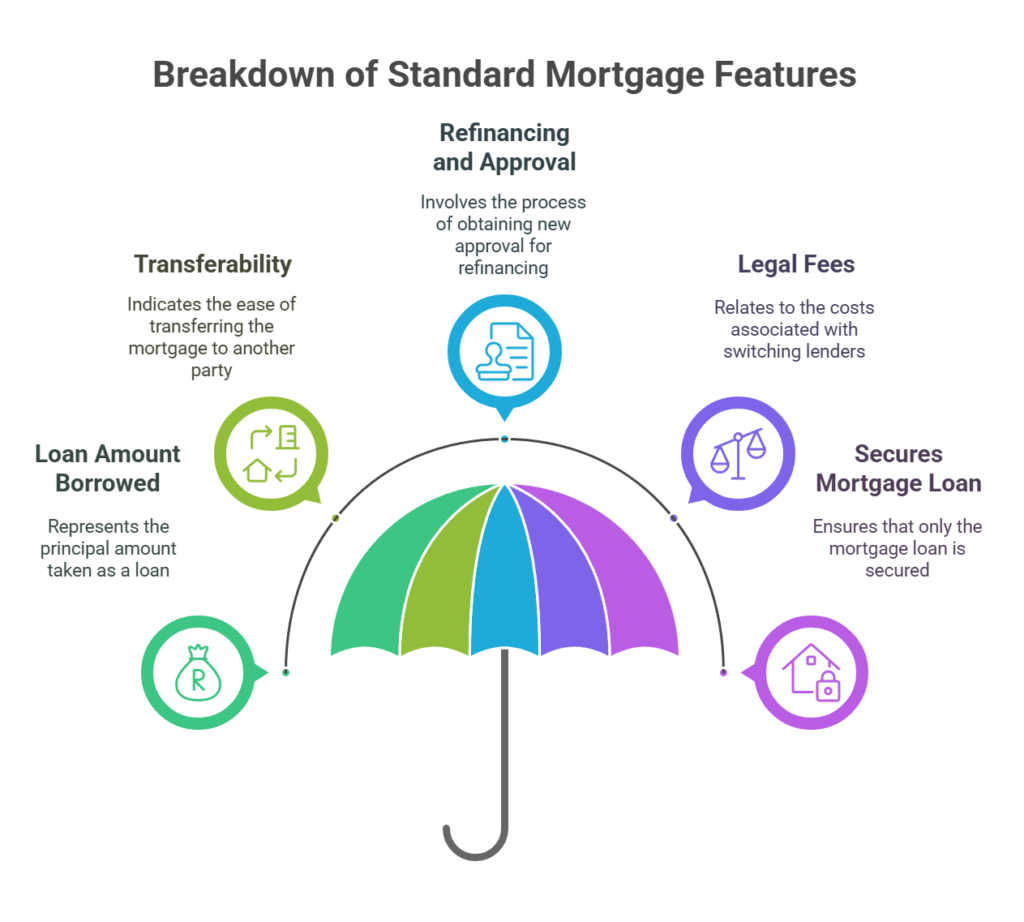

A standard charge mortgage is the conventional way lenders register a mortgage against a property. The mortgage amount recorded on the title is precisely the loan amount provided to the borrower, meaning the charge reflects the actual debt secured by the property.

With a standard mortgage:

- The borrower can easily transfer the mortgage to another lender at the end of the term without needing to discharge and re-register the loan, minimizing legal costs.

- If additional financing is required, a borrower must apply for a new loan or refinance the existing mortgage, which may involve legal fees and qualification reassessment.

- The loan structure is straightforward, with the mortgage terms and conditions outlined in a traditional lending agreement.

A standard mortgage is ideal for borrowers who prefer the ability to shop around for better rates at renewal without incurring additional registration fees.

What is a Collateral Mortgage?

A collateral charge mortgage, on the other hand, is registered for an amount that exceeds the initial loan amount—sometimes up to 125% of the property value. This structure provides lenders with greater flexibility to extend additional funds in the future without requiring a new mortgage registration.

Key characteristics of a collateral mortgage include:

- The ability to borrow additional funds without the need for re-approval, as long as the borrower meets the lender’s lending criteria.

- Refinancing or switching to another lender at the end of the term typically requires full mortgage discharge and re-registration, which incurs legal costs and may limit lender options.

- The mortgage agreement may include terms that allow for different credit products, such as lines of credit, business loans, or personal loans, to be secured under the same charge.

Collateral mortgages are advantageous for borrowers who anticipate needing future credit access without wanting to go through the approval process again. However, the trade-off is that switching lenders later can be more expensive and restrictive.

Standard Mortgage Problems

When most people think about a mortgage, they think about a standard mortgage; it’s straightforward enough. You get a house, you take out a mortgage for a certain amount, you shop around at renewal time, and you pay it off as fast as you can.

The problem with standard mortgages is that they are rigid, while people’s lives are flexible and often chaotic. Further, people are generally not good at anticipating the challenges life can through at them mostly because they lack the life experience to know what can happen. So, when things happen, as they do with most people, people must go through a lot to get the help they need.

And this help comes with a lot of cost. For example, 60% of Canadians need to break their mortgage for some reason but that reason is almost always because something happened that they didn’t consider or anticipate. The cost of breaking a fixed mortgage is often tens of thousands of dollars. Any new borrowing comes with new financing costs, legal costs, appraisal costs and so forth.

Collateral Mortgage to the Rescue

That’s where the collateral mortgage saves the day. A collateral mortgage enables you to access additional credit, funds, mortgage options, etc. and all those options are available to you without any new approvals. When you consider all the unanticipated challenges in life happen that can happen over 25 or 30 years of amortization, and the need for the collateralized mortgage product makes a lot of sense.

In addition, a re-advanceable mortgage is a type of collateralized mortgage that, utilizing and financial planner strategy, can enable you to write off your mortgage interest, aggressively pay off your mortgage while building your investment or retirement portfolio.

Collateral Mortgage Problems

Collateral charge mortgages offer certain conveniences, such as easier access to additional credit, but they also come with notable drawbacks that many borrowers don’t fully understand until they try to refinance or switch lenders. The challenges of collateral mortgages primarily revolve around limited transferability, hidden costs, legal complications, and borrowing risks. Understanding these issues is crucial before committing to this type of mortgage structure.

Difficulty Switching Lenders at Renewal

From a lender perspective, and it is mainly the chartered banks who offer collateral mortgages (but not always), a collateral mortgage creates a sticky relationship with the client that becomes difficult to break.

With a collateral charge mortgage, the existing lender must completely discharge the mortgage before a new lender can register a new mortgage. This process:

- Triggers legal fees (often $500-$1,000 or more).

Because collateral mortgages register for more than the loan amount, refinancing often requires a full legal discharge and re-registration. - Requires a new mortgage approval, meaning borrowers must qualify again under updated lending guidelines.

- Limits negotiating power, as borrowers are often forced to renew with their existing lender instead of shopping around for better rates.

Since many borrowers focus on low introductory rates and initial approval ease, they often overlook the fact that they might be locked into a lender when their term ends and how that may cost them more in the long run.

While lenders market collateral mortgages as “convenient” for future borrowing, the reality is that they increase refinancing costs and create barriers to lender flexibility.

Future Borrowing Isn’t Guaranteed (Despite a Higher Registered Amount)

A major selling point of collateral mortgages is that they are often registered for a higher amount (sometimes 125% of property value) so borrowers can access additional funds later without needing to requalify.

However, this does not mean that future borrowing is automatically approved. Borrowers must still meet the lender’s:

- Creditworthiness criteria at the time of borrowing.

- Debt service ratios based on current income and liabilities.

- Property value assessment at the time of request.

If a borrower’s income decreases, debt increases, or credit score declines, the lender can refuse to lend additional funds—even though the mortgage was registered for a higher amount.

This misconception leads many borrowers to believe they have “pre-approved credit,” when in reality, they may still be rejected when they apply for more funds.

Risk of Additional Borrowing Without Awareness

Because a collateral charge can secure multiple credit products under the same registration, lenders can attach additional loans, credit lines, or credit card debt to the mortgage without requiring a new registration.

How This Can Become a Problem:

- Hidden Credit Risks – If a borrower takes out a HELOC, personal loan, or business loan secured under their mortgage charge, they may not realize their total secured debt is increasing.

- Higher Interest Rates on Additional Loans – Unlike the main mortgage, which might have a low fixed rate, new loans added under the collateral charge could have higher variable rates.

- Increased Foreclosure Risk – Because all debts under a collateral charge are secured against the property, defaulting on a single loan (even a credit card) could trigger foreclosure.

This risk is particularly high for borrowers who use variable-rate credit products, as interest rates can rise unexpectedly, increasing monthly payments and overall debt load.

Potential for “Hidden Debt” on Credit Reports

When a borrower applies for a new mortgage or other loans, lenders typically assess their existing secured debts by checking their credit report.

However, collateral mortgages do not always report their full registered amount on credit reports. Some lenders only report the actual loan balance, not the full registered value.

Why This Matters:

- If a borrower applies for another loan or mortgage, the new lender may manually check the property title and discover the higher registered charge, making the borrower seem riskier.

- This can lead to denied credit applications or higher interest rates.

- Borrowers may be unaware that their full collateralized debt load affects their creditworthiness more than expected.

Home Equity May Become “Locked In”

For homeowners looking to sell their property or access equity, a collateral mortgage can reduce options because:

- If a property is registered with a high collateral charge (e.g., 125% of value), a borrower may struggle to get a second mortgage or HELOC from another lender.

- If the lender refuses additional borrowing, the borrower must refinance with another lender, incurring legal fees.

This makes collateral mortgages a poor choice for homeowners who want to maintain full control over their home equity.

Limited Transparency and Disclosure Issues

Many borrowers are not fully informed about the nature of collateral charge mortgages when they sign their contracts.

- Some banks automatically register mortgages as collateral without informing borrowers.

- Many borrowers assume their mortgage is standard, only to find out later that switching lenders is costly.

- Lenders may highlight the benefits (access to future borrowing) but downplay the drawbacks (transfer restrictions).

Regulators have pushed for clearer disclosures, but borrowers should always ask directly whether their mortgage is collateral or standard before signing.

Standard Mortgage to the Rescue

As financial products like collateral mortgages become increasingly complex, so do the problems that surround them compound. At a high level, most of the problems that impact collateral mortgages do not exist or at least not as strongly with standard mortgages.

First, standard mortgages are relatively easy to transfer, often for free, particularly at the end of term or renewal. When your car insurance or your cell phone plan term ends, you know you need to shop around, or you will pay way more for insurance or your cell phone. Mortgages are exactly the same. You are only cheating yourself if you don’t shop around for a better deal at the end of your mortgage term. Chartered banks don’t want you to do this because if you do, they have to offer you a lower interest rate to keep you (the rate they are offering their new clients… not you!). Collateral mortgage are expensive, difficult, and sometimes impossible to transfer. Keep that top of mind!

If something bad happens, such as job loss, drop in credit score, drop in home value or other negative financial impact, people assume the ability to borrow more money is always guaranteed; not true, being in a collateral mortgage can be far worse than being in a standard mortgage. This reality usually not explained to clients as collateral mortgage are often marketed as offering easy access to additional funds, actually come with significant risks that can trap borrowers in a difficult financial situation when they need help the most.

With a standard mortgage, if you have equity in your home, you may still be able to refinance with another lender, even if your credit has declined. With a collateral mortgage, you are often locked in with your current lender, limiting your options. And if the chartered bank declines your request for additional borrowing while preventing you from switching lenders, your only option may be a private mortgage which comes with much higher rates.

Collateral Mortgage Risks in a Financial Crisis

| Risk | Collateral Mortgage | Standard Mortgage |

| Future Borrowing | Not guaranteed despite higher registration | Requires refinancing but allows lender choice |

| Switching Lenders | Difficult and costly | Easy and often free |

| Refinancing Costs | High (legal fees, re-registration) | Lower (often just an admin fee) |

| Access to Home Equity | Controlled by lender, could be blocked | More flexible with second mortgage options |

| Risk of Power of Sale | Higher (all secured debt can trigger Power of Sale) | Lower (unsecured debts handled separately) |

| Negotiating Power | Low—lender controls terms | High—borrowers can shop around |

Key Differences Between Standard and Collateral Mortgages

| Feature | Standard Mortgage | Collateral Mortgage |

| Registered Amount | Only the loan amount borrowed | Can be up to 125% of property value |

| Portability to Another Lender | Easily transferable | Requires discharge and re-registration |

| Future Borrowing | Requires refinancing and new approval | Additional credit may be available without new approval |

| Associated Costs | Lower legal fees when switching lenders | Higher legal costs if switching lenders |

| Usage | Secures only the mortgage loan | Can secure multiple loan products |

Collateral Mortgage lenders

Many of Canada’s major banks and some alternative lenders prefer to register mortgages as collateral charges. This allows them to secure multiple lending products under one registration, making it easier for them to extend additional credit without requiring the borrower to requalify.

Big Banks That Use Collateral Mortgages

The following major banks typically register all or most of their mortgages as collateral charge mortgages:

- TD Canada Trust – Registers all new mortgages as collateral charges by default.

- Scotiabank – Offers STEP (Scotiabank Total Equity Plan), which is a collateral charge product that allows multiple credit products under one registration.

- National Bank – Uses collateral charge registration for many of its mortgage products.

- CIBC – Uses collateral registration for some of its mortgage products, especially those tied to home equity lines of credit (HELOCs).

- HSBC Canada (before acquisition by RBC) – Often used collateral charges for their mortgage products.

Alternative Lenders and Credit Unions That Use Collateral Mortgages

- Manulife Bank – Their Manulife One mortgage is a fully collateralized lending product that combines a mortgage with a HELOC.

- Home Trust – Often registers its mortgage products as collateral charges, particularly for alternative borrowers.

- First National (for some products) – While First National offers both types, they frequently use collateral registration, especially when bundling with other lending products.

- MCAP – Registers many of its mortgage products as collateral charges.

Standard Mortgage lenders

Some lenders prefer to use standard charge mortgages, which provide greater flexibility for borrowers who want to refinance or switch lenders at the end of their mortgage term.

Big Banks That Offer Standard Charge Mortgages

While many banks use collateral mortgages by default, some allow borrowers to choose a standard charge mortgage:

- Royal Bank of Canada (RBC) – RBC typically registers standard charge mortgages unless the borrower requests a HELOC or certain specialized products.

- BMO (Bank of Montreal) – BMO primarily registers mortgages as standard charges, making it easier to transfer to another lender.

Monoline Lenders That Use Standard Mortgages

Monoline lenders are financial institutions that specialize in mortgage lending without offering traditional banking products like chequing accounts or credit cards. Most monoline lenders register mortgages as standard charges to give borrowers flexibility:

- First National (for many products) – While First National uses collateral mortgages for certain products, many of its mortgages are standard charge.

- MCAP (for some products) – Like First National, MCAP offers both options, but standard charge mortgages are commonly available.

- RFA Mortgage Corporation – Primarily offers standard charge mortgages.

- Radius Financial – Uses standard charge registration.

- Merix Financial (and its subsidiaries) – Typically offers standard mortgages.

- Lendwise – Offers standard charge mortgages.

Credit Unions That Offer Standard Mortgages

Some credit unions still use standard charge mortgages, although many have started shifting toward collateral registration:

- DUCA Credit Union – Often registers standard charge mortgages but offers collateral options for HELOCs.

- Meridian Credit Union – Provides borrowers with a choice but is known for offering standard mortgages.

- Coast Capital Savings – Offers both options, with a preference for standard charges on conventional mortgages.

Which Mortgage Type is Right for You?

The truth is that both types of mortgages have strengths and weaknesses and the type of mortgage that is right for one person can be very wrong for another. So before talking about which is right for you, collateral or standard, you need to first have a good discussion about what your objectives are both now and in the future. The better you can anticipate your needs, the more accurately you’ll be able to make the right choice for you.

Choose a Standard Mortgage If:

- You prioritize the ability to switch lenders easily at renewal for better rates.

- You do not foresee needing significant additional credit in the future.

- You want a simpler, more transparent mortgage structure with no risk of additional debt being tied to the property.

Choose a Collateral Mortgage If:

- You anticipate needing access to future credit, such as a home equity line of credit (HELOC), without going through a new approval process.

- You prefer the convenience of a pre-approved credit limit against your home.

- You are comfortable with potential limitations on switching lenders without incurring fees.

Summary

Choosing between a standard and collateral mortgage depends on an individual’s financial strategy, risk tolerance, and long-term plans. A standard charge mortgage offers ease of movement between lenders and cost-effective refinancing, while a collateral charge mortgage provides built-in financial flexibility at the expense of transferability.

Let’s talk about your future borrowing needs and discuss your options to ensure that your chosen mortgage structure aligns with your homeownership and financial goals. Making an informed decision today can prevent unexpected costs and restrictions in the future.