A Mortgage Investment Entity (MIE) can be an excellent fit for certain types of investors, but may not be suitable for others. The key is understanding the investor’s goals, risk tolerance, liquidity needs, and tax situation. Here’s a breakdown of who typically benefits from MIEs — and who should be more cautious or consider alternatives.

Investors Who May Benefit from a MIE

Mortgage Investment Entities (MIEs) offer a compelling investment opportunity for those seeking consistent income, portfolio diversification, and a tangible link to real estate without the responsibilities of direct ownership. While they may not be suited to every investor, MIEs can serve as a strategic fit for individuals and entities with specific financial objectives and risk profiles.

For investors focused on generating reliable monthly or quarterly income — such as retirees, pre-retirees, or trusts — MIEs offer interest-based distributions backed by secured real estate lending. They also appeal to tax-conscious investors looking to shelter income within registered or corporate structures, as well as to those seeking a conservative alternative to the volatility of equities or the low returns of traditional fixed-income products. Additionally, self-directed investors who are comfortable navigating private markets may find MIEs an ideal way to enhance yield in registered accounts.

The following section explores the types of investors who stand to benefit most from incorporating a MIE into their overall financial strategy.

Income-Oriented Investors

MIEs are particularly well-suited for investors seeking consistent, predictable income. Because returns are typically derived from interest on mortgages, MIEs often pay monthly or quarterly distributions, making them ideal for:

- Retirees looking to supplement pension income

- Pre-retirees building income-generating portfolios

- Trusts and estates requiring regular distributions

Tax-Aware Investors

MIEs can be very effective in tax-sheltered accounts (e.g., RRSP, TFSA, LIRA), where the interest income isn’t immediately taxed. They also suit:

- Corporations with retained earnings that can invest in interest-generating assets

- High-income individuals who use MIEs inside registered or corporate accounts to defer or manage tax exposure

Diversified, Conservative Investors

Some MICs specialize in low loan-to-value (LTV) first mortgages on residential properties — offering relatively conservative exposure to real estate. For investors looking to diversify outside of the stock market or GICs, a reputable, low-risk MIC can provide stable returns with real estate security.

Self-Directed Investors

Those with self-directed RRSPs or TFSAs often use MIEs as a component of their fixed-income allocation, especially if they’re looking for yields above what bonds or GICs offer.

Considerations

Mortgage Investment Entities (MIEs) are particularly well-suited for investors seeking steady, income-generating opportunities backed by real estate. They are ideal for income-oriented investors such as retirees, pre-retirees, and trusts that value regular distributions. Tax-aware investors, including high-income individuals and corporations, can benefit from placing MIEs in registered or corporate accounts to shelter or defer tax on interest income.

For those seeking conservative diversification, some Mortgage Investment Corporations (MICs) offer low-risk exposure to first mortgages with strong real estate security. MIEs also appeal to accredited or eligible investors who want access to private markets without the extreme volatility of private equity. Finally, self-directed investors using RRSPs or TFSAs often turn to MIEs to boost yield within a fixed-income portfolio.

In short, MIEs can be a strategic fit for investors looking for consistent income, tax efficiency, and low-correlation alternatives to traditional markets.

Investors for Whom MIEs May Not Be a Good Fit

While Mortgage Investment Entities (MIEs) can offer attractive, stable returns and diversification benefits, they are not universally suitable for all investors. Like any financial instrument, MIEs come with trade-offs that may not align with every investor’s objectives, time horizon, or risk tolerance.

For some, the illiquidity of private mortgage investments or the absence of capital appreciation potential can pose significant concerns. Others may find the administrative and transparency aspects of private market investing uncomfortable or overly complex. It’s essential to understand the types of investors for whom MIEs may not be the best fit, so that capital is allocated where it can perform effectively — and with confidence.

The following section outlines common investor profiles that may want to exercise caution or consider alternative strategies before investing in a MIE.

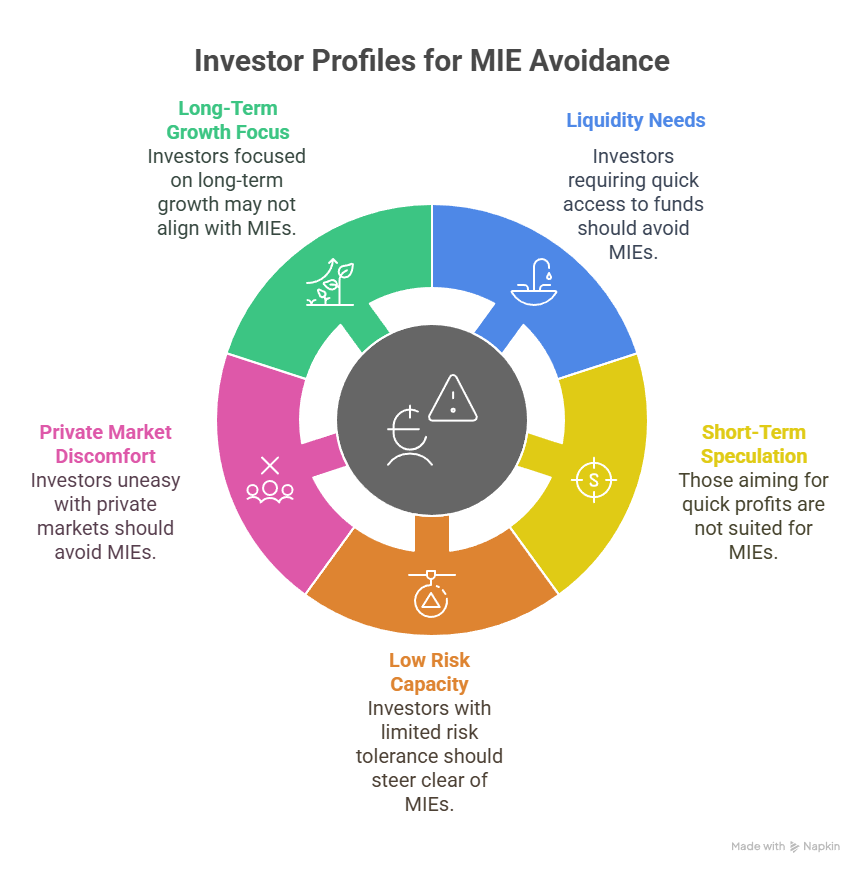

Those Who Need Liquidity

MIEs are not liquid like publicly traded securities. Redemption often requires 30–90 days’ notice, and some funds have restrictions on when and how much can be withdrawn.

If an investor may need their capital quickly or unpredictably, MIEs may not be appropriate.

Short-Term Speculators

MIEs are income-focused, not designed for capital appreciation. Investors looking for fast growth or speculative returns (e.g., from real estate flips, stocks, or crypto) will likely be disappointed by the steady but modest returns.

Highly Risk-Averse Investors Without Risk Capacity

While some MIEs are conservative, they are not risk-free. There’s always the risk of borrower default, real estate market downturns, or portfolio underperformance. Investors who are extremely risk-averse and can’t tolerate any principal risk may be better suited to insured GICs or government bonds.

Investors Uncomfortable with Private Markets

Some people simply don’t feel comfortable investing in non-publicly traded assets. MIEs typically require reading offering memorandums, understanding default procedures, and being okay with less frequent valuation updates. Transparency is growing, but not all investors are equipped or willing to do the homework.

Younger Investors with Long-Term Growth Focus

For investors in the wealth accumulation phase, MIEs may not offer enough growth potential. A diversified equity portfolio — though riskier — may be more aligned with long-term wealth-building objectives.

Considerations

Mortgage Investment Entities (MIEs) may not be suitable for every investor. Those who require liquidity should be cautious, as MIEs are not easily redeemable and often have holding periods or withdrawal restrictions. Short-term speculators seeking rapid growth or capital appreciation may also find MIEs unappealing due to their income-focused, steady-return nature.

Additionally, highly risk-averse investors who cannot tolerate potential capital loss might be better served by insured GICs or government bonds, as MIEs carry some credit and market risk. Investors who are unfamiliar or uncomfortable with private market investing may struggle with the limited transparency and lower regulatory oversight typical of MIEs. Finally, younger investors focused on long-term growth may find better opportunities in equities or real estate development ventures, which offer higher upside over time.

In essence, MIEs are best avoided by investors who prioritize liquidity, aggressive growth, or capital protection above all else.

Summary Table

| Investor Type | Good Fit for MIE? | Why / Why Not |

|---|---|---|

| Retiree Seeking Income | Yes | Regular interest distributions, low volatility |

| Business Owner with Retained Earnings | Yes | Passive income stream in a corporate structure |

| High-Income Individual (Using TFSA/RRSP) | Yes | Tax-sheltered interest income |

| First-Time Investor with Low Risk Tolerance | No | Illiquidity and credit risk may be too high |

| Short-Term Trader or Speculator | No | MIEs are built for income, not growth or capital gains |

| Growth-Oriented Millennial Investor | Possibly Not | Limited upside; equities may provide better long-term growth |

| Income-Focused Trust or Foundation | Yes | Steady income and capital preservation opportunities |

| Liquidity-Conscious Investor | No | Limited redemption flexibility |

READ MORE

Investing in Mortgage Investment Entities

The Mortgage Investment Entity Client

Summary

Mortgage Investment Entities (MIEs) offer a unique opportunity for investors seeking consistent, real estate-backed income and tax-efficient returns. They are especially attractive to income-oriented individuals—such as retirees, pre-retirees, and trusts—as well as tax-conscious investors looking to optimize their registered or corporate accounts. Conservative investors seeking diversification beyond equities or GICs, and self-directed investors aiming for higher yields within registered plans, also tend to benefit from MIEs.

However, MIEs are not ideal for everyone. Investors who require liquidity, prefer capital growth over income, or have little risk tolerance may find MIEs too restrictive or unsuitable. The lack of immediate access to funds, coupled with the private nature of the investment and the steady (rather than rapid) return profile, may not align with the goals of speculative or highly risk-averse investors. Additionally, younger investors in the wealth-building stage might prefer growth-oriented assets like equities.

In short, MIEs can be a strategic fit for the right investor profile—particularly those seeking stable income and conservative, tax-aware diversification. But for those who prioritize liquidity, high growth, or complete capital preservation, alternative investment vehicles may be a better choice.