… It’s not only about what you can buy, but how much you should buy.

Buying a home is exciting—no doubt about it. But let’s be honest: it’s also one of the biggest financial decisions you’ll ever make. The million-dollar (well, sometimes literally) question is, “How much house can I actually afford?” That’s where my Purchase Price Affordability Calculator comes into play.

This isn’t just a quick online tool. It’s designed to give you three perspectives:

- What financial planners say you should spend to keep your life balanced.

- What a prime lender or bank would actually approve you for (even if it risks making you “house rich, cash poor”).

- The point above which you won’t qualify with a bank, and might need to explore alternate or private lenders—if that risk makes sense for you.

Here’s what I’ll cover today:

Why Affordability Matters More Than You Think

How the Calculator Works: Three Numbers That Change the Game

A Realtor’s Secret Weapon in the Field

A Story: Sarah and the House Hunt That Made Sense

Putting the Numbers into Practice

Why Affordability Matters More Than You Think

Imagine falling in love with a gorgeous home—spacious kitchen, backyard for summer BBQs, maybe even a fireplace for cozy winter nights. Then, reality hits: the monthly payments are a stretch. Suddenly, your dream home feels more like a burden.

Affordability isn’t just about what the bank says you can borrow. It’s about what allows you to still live your life—take vacations, save for retirement, and not panic when the car needs repairs. My calculator lays out the landscape clearly so you see where smart money meets lender policy.

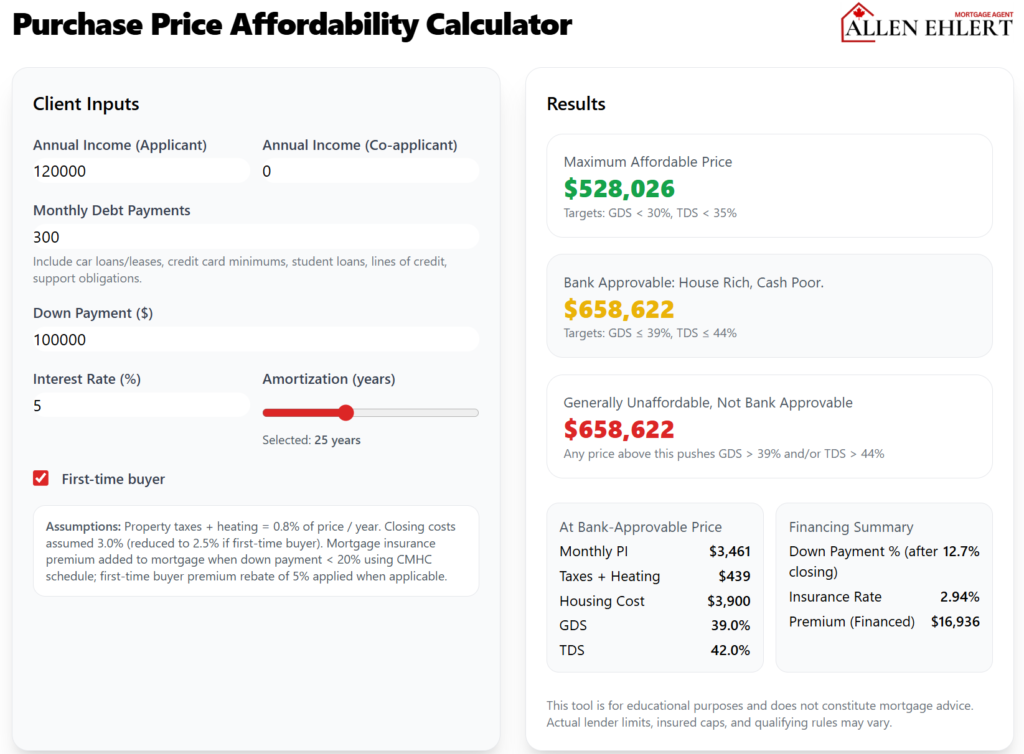

How the Calculator Works: Three Numbers That Change the Game

Here’s where this tool goes further than most:

- First Number – Financial Planner’s Threshold:

Financial planners generally recommend spending no more than a certain percentage of your income on housing costs. This number keeps your lifestyle balanced—so you’re not sacrificing everything else to keep the lights on. - Second Number – Bank Approval Limit:

This is what a prime lender would actually approve you for, based on Canada’s lending rules. Here’s the catch: banks don’t care if you can still afford hockey lessons, dinners out, or annual family trips. If you buy at this level, you may feel stretched—house rich, but cash poor. - Third Number – The Hard Ceiling:

This is the point where prime lenders simply won’t approve you anymore. If you’re determined to go higher, you’d be looking at private or alternate lenders. It’s not always the wrong choice, but it’s one that comes with higher rates and risks that need serious consideration.

By showing you all three, the calculator doesn’t just answer “How much can I borrow?”—it answers “How much should I spend?”

A Realtor’s Secret Weapon in the Field

If you’re a realtor, this tool isn’t just handy—it’s a game-changer. Picture this: you’re touring homes with clients who are still fuzzy about their budget. Instead of guessing, you whip out the calculator, plug in the numbers, and—bam!—you’ve just given your clients clarity from three different perspectives.

That means fewer wasted showings, more trust, and clients who feel empowered instead of confused. Realtors who use this tool set themselves apart as true advisors.

A Story: Sarah and the House Hunt That Made Sense

Let me tell you about Sarah, a first-time buyer in Oshawa. She had her heart set on a $950,000 home. The calculator showed her three numbers:

- A financial planner would have told her $780,000 was the sweet spot.

- The bank would have stretched her to $950,000—technically doable, but leaving little wiggle room.

- Anything higher wasn’t even an option without going private.

Sarah’s realtor focused the search around $780,000. Within weeks, she landed a semi-detached that ticked every box and left her with money in her pocket each month. She avoided the trap of being house poor and instead bought a home she could actually enjoy.

Putting the Numbers into Practice

Here’s how different people can use the tool:

- First-time buyers: Get clarity on the “comfort zone” versus the “bank’s zone” before hitting MLS.

- Realtors: Use the three-number breakdown to manage expectations and focus your client’s search.

- Move-up buyers: Compare what’s smart versus what’s technically possible when upsizing.

- Families: Test scenarios—what if you pay off a car loan first, or increase your down payment?

This is financial reality made visual—it’s like looking at your budget under a spotlight.

Allen’s Final Thoughts

At the end of the day, my Purchase Price Affordability Calculator is more than a tool—it’s a roadmap. It gives you clarity from three different angles: the financial planner’s lifestyle threshold, the bank’s approval limit, and the ceiling that pushes you into alternate lending territory.

My job as your mortgage agent is to help you navigate those numbers. Sometimes it’s about protecting you from being stretched too thin; other times, it’s about helping you access the right lender—even if that means considering alternatives. I’ll walk you through strategies to strengthen your approval, improve your affordability, and keep your financial life balanced.

Whether you’re a buyer wanting peace of mind or a realtor wanting a reliable partner, I’m here to ensure the numbers make sense—not just on paper, but in your real, everyday life.