Can You Really Afford That Home? Do you qualify for that home?

You’ve found the dream home: open-concept kitchen, backyard for summer BBQs, maybe even a finished basement for movie nights. The mortgage payment looks doable. But here’s the kicker: just because you can afford the payment doesn’t mean the bank will agree.

That’s where my Carrying Cost Calculators come in. They go beyond the basic “can I pay the mortgage?” question. They measure affordability two ways:

- Whether the payments fit your budget from both a housing and total debt perspective.

- Whether you’ll actually pass the bank’s stress test and qualify for the mortgage in the first place.

And to make it crystal clear, the results appear on a multi-coloured slide that visually shows your level of risk—from “comfortable” to “caution” to “danger zone.”

Here’s what we’ll cover today:

Why Carrying Costs Matter (It’s More Than Just Your Mortgage Payment)

How the Calculators Work: GDS, TDS, and the Stress Test Toggle

A Realtor’s Secret Tool for Setting Realistic Expectations

A Story: Jasmine and the Townhouse That Almost Stretched Too Far

Putting the Numbers Into Practice

Why Carrying Costs Matter (It’s More Than Just Your Mortgage Payment)

Too many buyers make the mistake of saying, “As long as I can swing the mortgage, I’m fine.” But lenders—and life—look at the bigger picture.

Carrying costs include:

- Mortgage payment

- Property taxes

- Heat (and condo fees if applicable)

- Other debts like car loans, student loans, and credit cards

If those numbers eat up too much of your income, you risk being house rich but cash poor—owning the home but stressed every month. That’s why lenders use carrying cost ratios to decide whether to approve you, and why you need to understand them before you go house hunting.

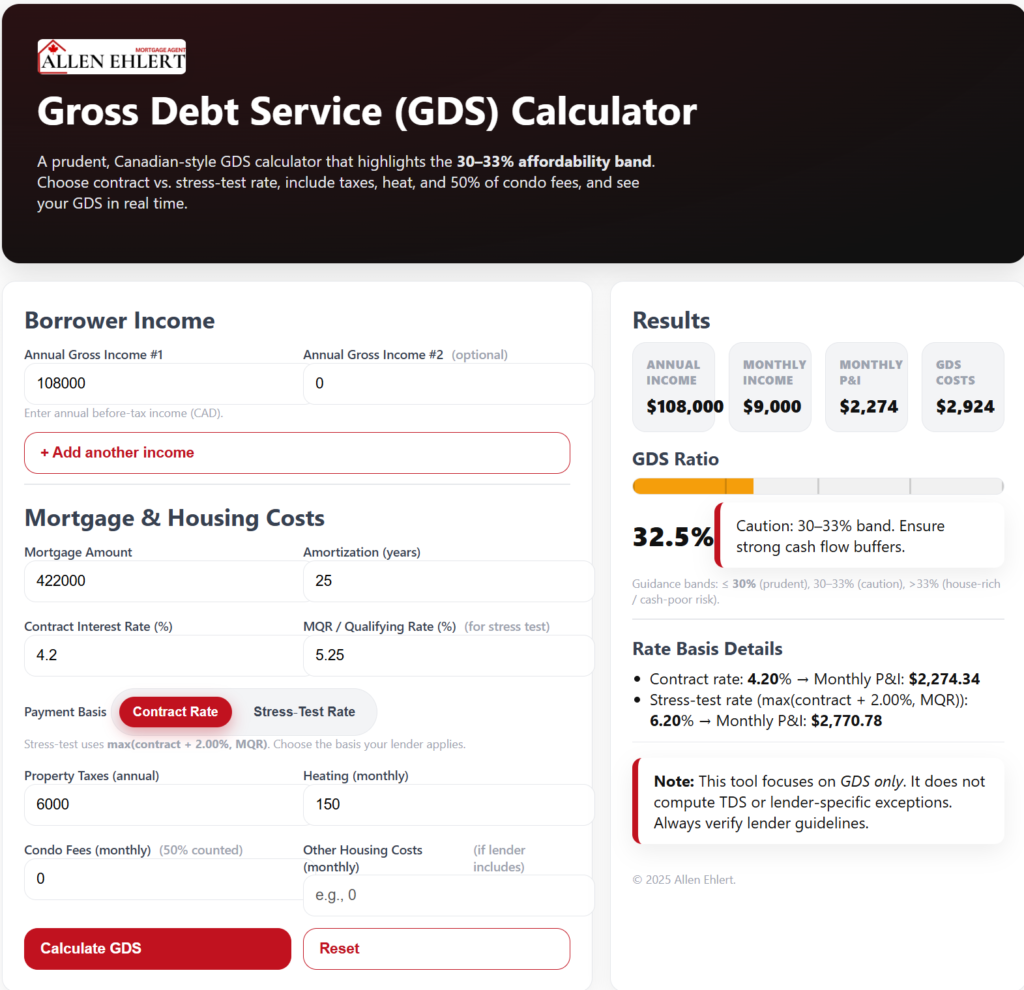

How the Calculators Work: GDS, TDS, and the Stress Test Toggle

Here’s where my calculators shine. They calculate both:

- Gross Debt Service (GDS): Housing costs vs. your income.

- Total Debt Service (TDS): Housing + all your other debts vs. your income.

But that’s just the beginning.

The calculators also include a stress test toggle. This lets you see:

- Your affordability in reality: What you can pay comfortably right now.

- Your affordability in the bank’s eyes: Whether you pass Canada’s mortgage stress test (currently the higher of 5.25% or your contract rate + 2%).

This is the game-changer. Because plenty of clients think, “I can make these payments.” But when the bank applies the stress test, they no longer qualify. The calculator reveals that gap in seconds.

And instead of drowning you in numbers, it displays the results on a multi-coloured slide. You instantly see whether you’re in the green (safe), yellow (tight), or red (high risk). It’s visual, intuitive, and takes the guesswork out of affordability.

A Realtor’s Secret Tool for Setting Realistic Expectations

Realtors, this is your secret weapon during buyer consultations. Imagine showing a client the multi-coloured results slide. Instead of saying, “This house might be a stretch,” you can show them exactly where they fall on the risk spectrum—and whether they’ll pass the bank’s stress test.

That builds trust, avoids wasted showings, and positions you as a true advisor. Plus, no client wants to fall in love with a home they can’t qualify for.

A Story: Jasmine and the Townhouse That Almost Stretched Too Far

Jasmine, a young professional in Ajax, thought she had it all figured out. She’d budgeted for a $750,000 townhouse, and her monthly payment looked manageable. But when she ran the numbers through my Carrying Cost Calculator and hit the stress test toggle, the slide turned yellow edging into red.

- Her GDS was right at the limit.

- Her TDS, once her car loan and student loan were added, pushed her past what the bank would accept.

- Under the stress test, she didn’t qualify at all.

Instead of hitting a wall later in the mortgage approval process, Jasmine adjusted her search. She targeted a $680,000 home that put her back in the green zone. Come approval time, she breezed through—no heartbreak, no surprises.

Putting the Numbers Into Practice

Here’s how to make the most of the calculators:

- First-time buyers: See whether your “dream budget” actually passes the stress test.

- Realtors: Use the colour-coded results to set expectations early.

- Move-up buyers: Factor in existing debts so you don’t overextend.

- Families: Test how paying off a car loan or credit card could push you from yellow back to green.

- Investors: Check if carrying multiple properties still keeps you bank-approvable.

It’s like a dress rehearsal before the main event—you want to know if you can play the role before opening night.

Allen’s Final Thoughts

Buying a home isn’t just about what you think you can pay—it’s about what the bank will actually approve. My Carrying Cost Calculators bridge that gap. They combine GDS, TDS, and the stress test toggle into one simple tool, then display the results on a colour-coded slide that makes your risk crystal clear.

And that’s where I come in. As your mortgage agent, I’ll help you interpret those results, explain what lenders are really looking for, and coach you on strategies to improve your numbers—whether that means restructuring debt, tweaking the purchase price, or exploring alternate lending options.

Because getting a mortgage isn’t just about qualifying. It’s about qualifying comfortably, wisely, and with confidence.