…The “One Submission” Alternative Lender

If you’ve ever had a mortgage file that looked perfectly reasonable in real life—but got torpedoed by policy, the stress test, or “computer says no”—you already understand why the alternative-lending world exists. It’s the part of the market built for real people with real income quirks, real timelines, and the occasional credit bruise. Maple Financial is one of the more interesting players in that space because they’re deliberately trying to make alternative lending feel more predictable, more consistent, and less like you’re rolling the dice every time you pivot away from prime.

Alternative lending in plain English

There’s a Problem in the Alternative Lending Space

How to use this in the real world

Alternative lending in plain English

Alternative lending is the “middle lane” between traditional prime lenders and true private lending. It’s where you go when the borrower’s story makes sense—but the file doesn’t fit neatly into prime lender credit boxes.

A big reason this happens in Canada is the minimum qualifying rate (the “stress test”) for many mortgages. The rule is essentially: you must qualify at the greater of your contract rate + 2% or a minimum qualifying rate floor (often referenced as 5.25%). That gap can push otherwise responsible borrowers outside prime approvals—especially when they’re carrying other debts, have variable income, or are buying in higher-priced markets.

Now, quick real talk: alternative mortgages can come with higher rates and/or lender fees compared to prime. And private mortgages can be even more expensive, with higher risk if there isn’t a clear repayment plan. Regulators regularly remind consumers to understand the full cost, the term, the fees, and the exit strategy before signing anything.

That’s exactly where Maple Financial tries to stand out: they position themselves as a structured alternative lender that’s aiming for clarity and consistency instead of surprises.

Meet Maple Financial

Maple Financial describes itself as an alternative residential mortgage lender (you’ll see that language in their public communications). Their focus is squarely on the broker channel—and they emphasize a simplified experience where you submit once and they match the borrower to the appropriate “swim lane,” from near-prime to more private-style solutions.

On the corporate-development side, Maple announced a strategic equity investment from nesto via its wholly owned subsidiary CMLS (the release framed it as a partnership combining Maple’s underwriting model with technology and distribution).

Why Maple feels different

Most alternative lenders will tell you they’re “flexible.” Maple’s differentiation is more specific: they’re trying to make flexibility feel systematic.

Their messaging is built around three ideas:

Maple pushes a “single submission” concept across a spectrum of solutions, framed as near-prime through private. In the alternative world, that matters—because brokers and clients get exhausted re-packaging the same deal for lender after lender.

They also lean hard on their Broker Relationship Management (BRM) underwriting framework—positioned as a high-touch model built for broker partners. In their investment announcement, Maple explicitly described BRM as “industry-leading,” and framed the partnership as expanding Maple’s ability to deliver a “premier alternative lending experience.”

Finally, Maple repeatedly contrasts “predictable” and “transparent” terms against the common pain points brokers report in alt lending—things like inconsistent rules, hidden fees, and unpredictable outcomes. That theme shows up strongly in industry reporting and in direct quotes attributed to Maple’s leadership.

There’s a Problem in the Alternative Lending Space

There’s a big problem in the alternative lending space: many alternative lenders do not provide satisfactory service. There have been occasions where files have been submitted to an alternative lender, then we hear nothing for weeks and weeks, and finally the file is rejected with little or no explanation. Time is money, and to leave a client dangling because you can’t get back to them promptly is unacceptable.

We never have that problem with Maple Financial.

One of the biggest differences you’ll notice with Maple Financial is the level of customer service—and in the alternative lending space, that’s not a small thing. Instead of the typical experience where your file gets passed between departments, and you’re left chasing updates, Maple uses a dedicated one-point-of-contact model. That means the same person is involved in underwriting, structuring, and guiding your mortgage to funding. The result is faster decisions, clearer communication, and far fewer surprises along the way.

More importantly, their team is focused on understanding your full financial story—not just ticking boxes—so they can actively work toward getting your mortgage approved rather than looking for reasons to decline it. In a space where delays, confusion, and inconsistent responses are common, Maple’s approach is designed to feel more responsive, more predictable, and ultimately, much easier to navigate.

Maple’s product lineup

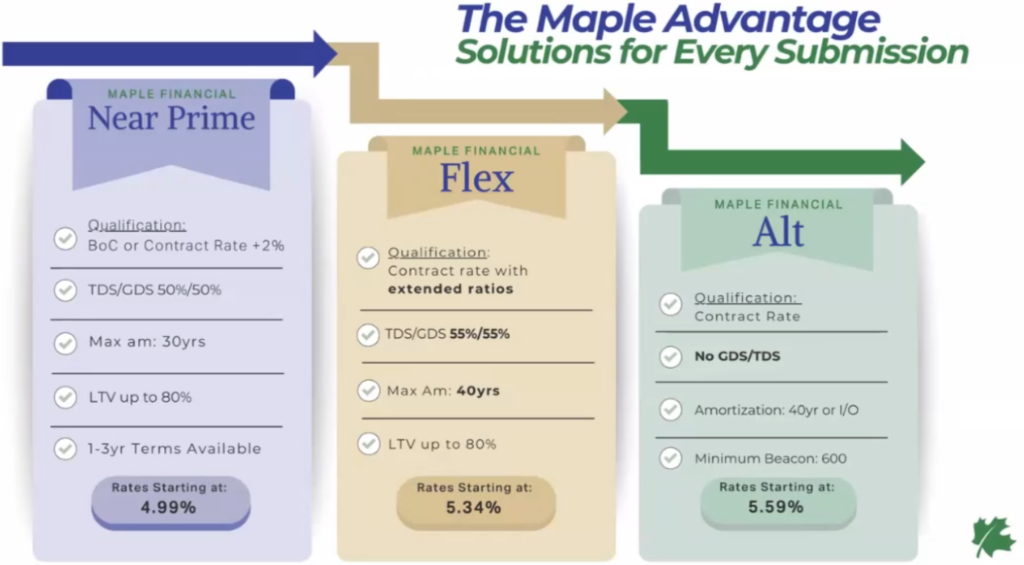

Maple’s core “shelf” is typically presented as three product buckets: Near Prime, Flex, and Alt.

What I like, from a borrower-experience standpoint, is that these programs are clearly positioned with specific credit/risk intent—rather than a vague “maybe we can do it” promise.

Near Prime

Near Prime is designed for borrowers who are “almost prime,” but not quite. This typically includes good borrowers who have been bumped out of traditional financing due to policy constraints, the stress test, or how their income is structured.

Typical loan amounts range from $200,000 to $1,500,000, with amortizations of up to 30 years.

From a qualification perspective, Near Prime generally works within 50% / 50% debt service ratios, and lending is available across major provinces, including Ontario, British Columbia, and Alberta, with location tiering applied.

Loan-to-value limits can reach up to 80% for many owner-occupied purchases and refinances, although certain property types—such as condominiums—may have additional restrictions depending on the scenario.

Pricing is based on Maple’s published rate sheet and varies depending on factors such as loan-to-value, credit profile, and term length.

Flex

Flex is Maple’s “B-side” solution, designed for borrowers who need more flexibility on ratios, amortization, or income structure. It’s particularly useful for borrowers with more complex financial profiles or some degree of credit softness.

Loan amounts typically range from $200,000 to $1,500,000, with amortizations extending up to 40 years, providing additional room to manage payments.

Flex allows for higher qualification thresholds, with maximum GDS/TDS ratios of 55% / 55%, and minimum credit scores generally starting at 550.

Loan-to-value limits are location-sensitive, with examples including up to 80% in stronger (A+) markets, while other areas may have lower limits or a sliding scale depending on risk and marketability.

This product also accommodates more flexible income verification methods, making it suitable for borrowers whose income doesn’t fit neatly into traditional documentation standards.

As with Near Prime, pricing is published on Maple’s rate sheet and varies depending on the specific details of the file.

Alt

Alt is Maple’s “near-private” style product, designed for borrowers who are equity-rich and require a short-term solution with a clear exit plan.

Loan sizes generally range from $200,000 to $1,500,000, and the product can include 40-year amortizations or interest-only payment options, depending on the structure.

Unlike the other products, Alt does not rely on traditional GDS/TDS ratios, and instead focuses more heavily on the strength of the property, the borrower’s overall situation, and—most importantly—the exit strategy.

Key qualification parameters include:

- First-position lending only

- Minimum credit score of 600

- Location-based restrictions and tiering

Loan-to-value limits are also structured by location, with examples including:

- Up to 75% in A+ locations

- Up to 70% in A and B locations, along with other caps depending on the property and scenario

Pricing for Alt includes a premium over Maple’s standard offerings (often referenced as “Select” rates), and full details are outlined in their rate sheet.

Who’s a great fit

If you’re wondering, “Okay… am I the kind of borrower Maple was built for?”—here are the profiles that tend to line up well with how their shelf is designed.

You’re a strong borrower on paper, but the prime box doesn’t love your file. Near Prime is explicitly built for that “almost there” borrower segment, with defined loan amounts, amortizations, and debt-ratio caps.

You need more breathing room on ratios or amortization. Flex allows higher stated debt-service ceilings (55/55) and longer amortizations (up to 40 years), which can be a practical pressure-release valve when today’s payment math is tight.

Your income is real, but it doesn’t show up cleanly in traditional documents. Flex references bank-statement style verification for certain income components (for example, “contributory income” supported by bank statements, with caps on how much can be used). That’s the kind of structure that can help self-employed or variable-income borrowers who still have a credible story.

You have equity and a clear exit—so a short-term, structured “Alt” mortgage actually makes sense. Maple’s Alt product materials emphasize repayment ability/fallback and, importantly, an exit strategy mindset (and they outline parameters like first-position security and LTV caps by location tiers).

And one more that matters for brokers and referral partners: Maple’s leadership and industry coverage repeatedly talk about making alt lending more consistent and less surprise-prone, using an institutional backbone and clearer “swim lanes.” That’s not just marketing fluff—it’s a direct response to the pain points that cause deals to blow up late in the game.

Who should probably pass

Alternative lending is a tool. A good tool, used the right way. But it isn’t magic.

You’ll likely be a poor fit for Maple (or any structured alt lender) if:

You’re looking for prime pricing with private-level flexibility. Maple publishes a rate sheet and product parameters, and their shelf is clearly segmented by risk tier; if the expectation is “give me bank pricing but ignore bank rules,” you’re setting yourself up for frustration.

You don’t have a credible exit strategy on a short-term solution. Maple’s Alt materials and public commentary keep circling back to repayment capacity and exit strategy—not just the property value. If there’s no path forward (refinance, sale, income normalization, debt cleanup), a short-term mortgage can become an expensive treadmill.

Your credit profile is below the minimums for the lane you’re trying to use. For example, Maple references minimum FICO expectations (Flex minimum 550; Alt minimum 600). If you’re below those thresholds, we may need a different lender type, or a different plan altogether.

The property or location doesn’t meet the program’s marketability requirements. Maple’s location tiering and LTV caps are explicit in their product materials. If the property is outside those parameters (or is hard to sell, hard to value, or hard to insure), that changes the conversation fast.

And one last “big picture” poor fit: if you’re uncomfortable with fees and higher borrowing costs in exchange for flexibility, you may prefer to delay buying, adjust the budget, or restructure debt first.

How to use this in the real world

Here’s where this gets practical—for you, and for the realtors you work with.

A quick story that sounds familiar

Let’s say you’re buying a home and you’re self-employed. You’ve got money in the bank, clients paying invoices, and you’ve been running your business for years. But (because you’re not new to taxes) your declared income is optimized, and your prime approval comes back short.

Meanwhile, your realtor’s sweating bullets because the closing date is coming up fast—and nobody wants to relist, renegotiate, or watch the deal collapse over paperwork.

This is the kind of moment where an alternative “waterfall” approach can be a lifesaver. Industry coverage describes Maple’s model as: submit once, they adjudicate upstream first, and if it doesn’t fit, they move it downstream into the best-fit product lane.

What you do as the borrower

This is the “don’t wing it” part. If you want an alternative approval to be smooth, you need a clean, well-packaged story.

Here’s the procedure I walk you through:

First, we diagnose why prime said no (or why the numbers don’t work): stress test constraints, income recognition, ratios, property, credit, or timing.

Second, we choose the right lane—Near Prime vs. Flex vs. Alt—based on what the product sheets actually allow (not what we wish they allowed).

Third, we build your exit plan (even if the exit is simply “stabilize income, pay down X debt, and refinance back to prime in 12–24 months”).

Allen’s Final Thoughts

If you take one thing away from this, let it be this: alternative lending isn’t a “last resort”—it’s a strategy when the prime box doesn’t reflect real life. Maple Financial is interesting because they’re aiming to make that strategy more predictable: one submission, a defined product shelf (Near Prime, Flex, Alt), and a service model that’s built around broker execution rather than leaving you to chase five different lenders with five different rulebooks. As your mortgage agent, I’m here to quarterback the whole thing—coaching you on how to present your income story properly, stress-testing the payment and renewal risks, setting expectations with your realtor, and mapping the cleanest exit so you’re not “stuck” in an expensive lane longer than you need to be.