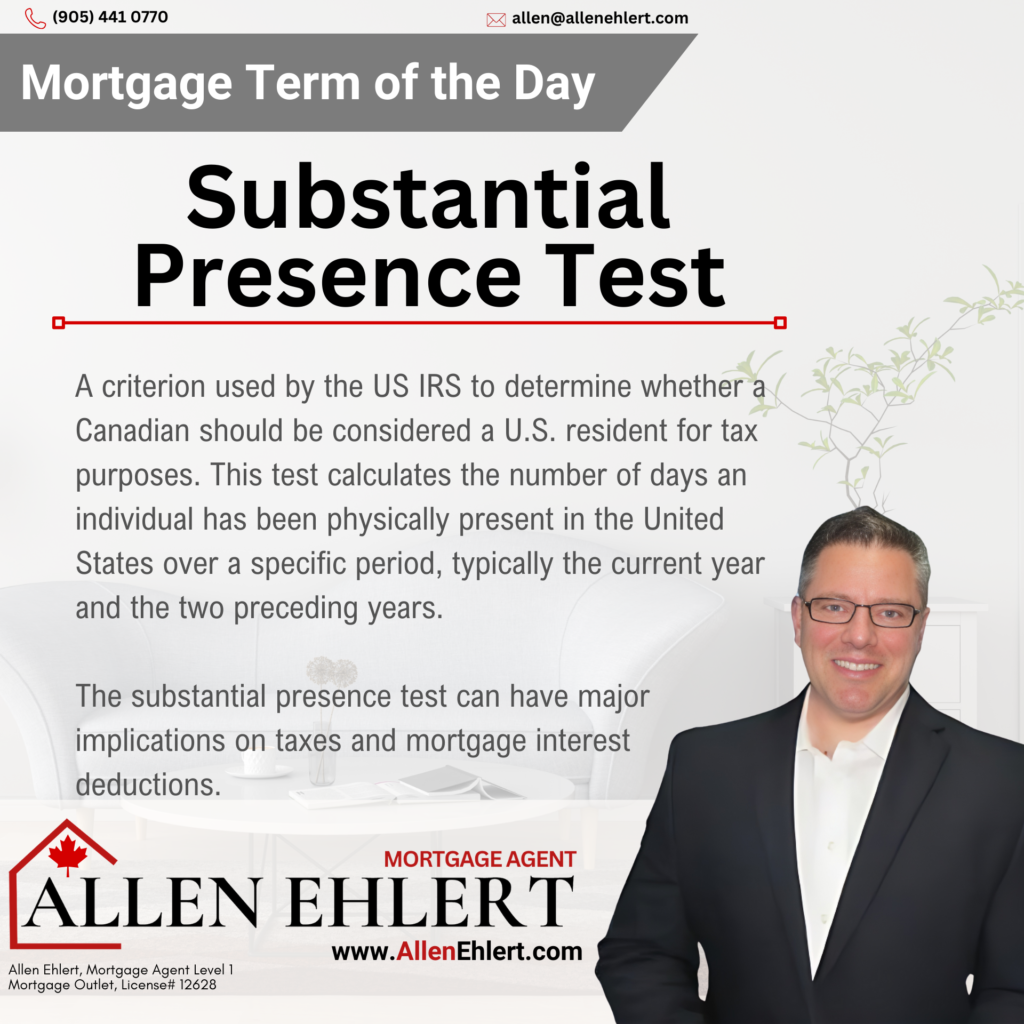

The substantial presence test is a criterion used by the United States Internal Revenue Service (IRS) to determine whether a non-U.S. citizen or non-U.S. permanent resident (i.e., a foreign national like a Canadian) should be considered a U.S. resident for tax purposes. This test calculates the number of days an individual has been physically present in the United States over a specific period, typically the current year and the two preceding years.

How Does the Substantial Presence Test Work?

To meet the Substantial Presence Test, an individual must have been physically present in the U.S. for:

At least 31 days during the current year, and

183 days during the 3-year period which includes the current year and the two years immediately before that. The 183 days are calculated as:

- All of the days the individual was present in the current year.

- 1/3 of the days the individual was present in the previous year.

- 1/6 of the days the individual was present in the year before that.

Relation to Mortgages

The Substantial Presence Test can affect a person’s eligibility for certain financial products, including mortgages in the U.S. Here’s how:

Residency Status for Loan Eligibility:

Meeting the Substantial Presence Test may classify an individual as a U.S. resident for tax purposes, which can influence their ability to secure a mortgage. U.S. residents typically have better access to mortgage products compared to non-residents.

Non-residents may face stricter lending requirements, such as higher down payments, different interest rates, or limited loan options.

Tax Implications:

If an individual qualifies as a U.S. resident through the Substantial Presence Test, they may be subject to U.S. tax on their worldwide income. This can influence the documentation and qualifications for a mortgage, as lenders typically review tax returns to assess an applicant’s financial stability.

Mortgage interest deductions may also differ depending on residency status for U.S. tax purposes.

Foreign National Mortgages:

For those who do not meet the Substantial Presence Test and are classified as non-residents, some lenders offer foreign national mortgages. These loans may have unique qualification requirements and often come with more stringent terms.

Summary

In summary, the Substantial Presence Test plays an important role in determining a person’s tax residency status, which can impact mortgage eligibility, tax liabilities, and the terms under which loans are offered in the U.S.