In Canada, wells are a crucial water source for many rural and semi-rural properties where municipal water services are unavailable. Homeowners rely on wells to access groundwater for daily use, including drinking, cooking, and irrigation.

The need for a well typically arises when a property is located outside of urban areas, making connection to a municipal water system impractical or cost-prohibitive. Wells provide a self-sufficient, cost-effective water supply, but their functionality depends on factors such as water table depth, soil composition, and climate conditions.

When assessing a property, appraisers consider the type, condition, and water quality of a well, as these factors can significantly impact property value, financing eligibility, and long-term maintenance costs. Properly maintained wells offer a reliable water source, but factors like contamination risk, seasonal fluctuations, and pumping capacity must be carefully evaluated during an appraisal.

Bored Wells (Shallow or Intermediate Depth)

Driven Wells (Sand-Point Wells)

Artesian Wells (Pressurized Wells)

Horizontal Wells (Collector Wells)

Dug Wells (Shallow Wells)

In many rural parts of Canada, especially where the water table is high and drilling costs are prohibitive, dug or shallow wells are a common water source. These wells, often hand-dug or excavated with machinery, tap into groundwater close to the surface—typically no deeper than 30 feet.

They are cost-effective and easy to install, making them an attractive option for older properties, seasonal cottages, or farms where a deeper well isn’t necessary. However, their shallow depth makes them vulnerable to contamination from surface runoff, seasonal droughts, and bacterial infiltration, requiring regular maintenance, filtration, and testing.

Homeowners with dug wells must be diligent about water quality and wellhead protection, as any issues can affect not only daily water use but also property value and mortgage eligibility. While a dug well can be a perfectly functional water source, appraisers assess its sustainability, potential health risks, and whether alternative water sources might be needed in the future.

Dug Wells (Shallow Wells)

Depth: 10 to 30 feet

Construction: Excavated manually or with machinery, then lined with stones, bricks, or concrete rings.

Water Source: Shallow groundwater.

Common Issues: Contamination from surface runoff, seasonal drying.

Best For: Low-demand rural properties or temporary water sources.

Bored Wells (Shallow or Intermediate Depth)

In many rural and semi-rural areas of Canada, bored wells offer a practical solution for properties with a moderately deep water table where a traditional dug well might not provide enough reliability.

Constructed using a large-diameter auger, these wells typically extend 30 to 50 feet deep, making them deeper than dug wells but still classified as shallow or intermediate-depth wells. They are often lined with concrete or steel casing to prevent collapse and contamination, providing a more stable and long-lasting water source compared to hand-dug wells. Homeowners choose bored wells in regions with clay-heavy soil or inconsistent water tables, where deeper wells might be unnecessary but surface water infiltration is a concern.

While they offer better protection from contamination than dug wells, they can still be affected by seasonal water fluctuations, requiring careful monitoring and potential backup water solutions. From an appraisal perspective, the reliability and quality of a bored well are key considerations, as they impact both property functionality and lender financing approval.

Bored Wells (Shallow or Intermediate Depth)

Depth: 30 to 50 feet

Construction: Dug using an auger or boring machine and lined with concrete or steel casing.

Water Source: Shallow aquifers, with potential seasonal fluctuations.

Common Issues: Contamination risk similar to dug wells.

Best For: Properties in areas with a high water table.

Driven Wells (Sand-Point Wells)

In certain parts of Canada, particularly in areas with loose, sandy soil and a high water table, driven wells—also known as sand-point wells—provide a simple and cost-effective water source. These wells are created by driving a narrow, screened pipe into the ground, usually reaching depths of 30 to 50 feet to tap into shallow aquifers. Their affordability and quick installation make them popular for seasonal cottages, remote cabins, and irrigation systems, where access to deeper groundwater isn’t necessary.

However, because they rely on unconfined, shallow water sources, they are highly susceptible to contamination from surface runoff, drought conditions, and sediment buildup, making frequent water testing essential. While a driven well can be a practical solution for low-demand properties, appraisers assess its sustainability, water yield, and filtration needs, as these factors directly impact property usability, lender financing, and long-term value.

Driven Wells (Sand-Point Wells)

Depth: 30 to 50 feet

Construction: A small-diameter steel pipe with a screened well point is driven into the ground.

Water Source: Shallow water tables in sandy or loose soils.

Common Issues: Prone to clogging, limited water yield.

Best For: Small homes, cabins, or temporary water supply.

Drilled Wells (Deep Wells)

In most parts of Canada, where groundwater is found at greater depths or where reliability is a priority, drilled wells—often referred to as deep wells—are the preferred water source. These wells are created using rotary or percussion drilling equipment, extending 50 to 500 feet or more into bedrock or deep aquifers to access clean, stable groundwater.

Unlike shallow wells, drilled wells offer greater protection from contamination, consistent water supply year-round, and higher water yield, making them ideal for year-round homes, farms, and high-demand properties. While they come with higher upfront costs due to specialized drilling and casing requirements, they are considered a long-term investment in water security.

From an appraisal standpoint, a well-maintained drilled well is a valuable asset, as it ensures a dependable water source and often makes the property more appealing to buyers and mortgage lenders. However, factors like well depth, water flow rate, and water quality are carefully evaluated, as they can significantly affect property usability and market value.

Drilled Wells (Deep Wells)

Depth: 50 to 500+ feet

Construction: Created using rotary or percussion drilling rigs, lined with steel, PVC, or concrete casing.

Water Source: Deep aquifers with more stable water levels.

Common Issues: Higher installation cost, but more reliable and lower risk of contamination.

Best For: Most modern homes, agricultural use, and commercial water supply.

Artesian Wells (Pressurized Wells)

In certain regions of Canada where confined aquifers exist beneath layers of impermeable rock or clay, artesian wells offer a unique and highly desirable water source. Unlike traditional wells that rely on pumps, artesian wells tap into naturally pressurized groundwater, allowing water to flow to the surface on its own or with minimal pumping. This makes them an excellent choice for rural properties, farms, and areas where deep, consistent water access is needed.

Because the water is drawn from deep underground and protected by natural barriers, artesian wells often provide cleaner, more stable water supplies with less risk of contamination compared to shallow wells. However, maintaining flow control and preventing water waste are important considerations, as excessive pressure can lead to overflow or depletion.

From an appraisal perspective, a properly installed and regulated artesian well is a valuable asset, enhancing both property functionality and long-term sustainability, particularly in areas where water access is a key factor in real estate desirability.

Artesian Wells (Pressurized Wells)

Depth: Varies; often deeper (100+ feet).

Construction: Drilled into a confined aquifer where water is under natural pressure.

Water Source: Water flows naturally to the surface without a pump (if pressure is high enough).

Common Issues: May require flow control to prevent waste.

Best For: High-yield wells, areas with naturally pressurized groundwater.

Horizontal Wells (Collector Wells)

In certain regions of Canada where traditional vertical wells may not be efficient or feasible, horizontal wells, also known as collector wells, provide an innovative solution for accessing groundwater. Instead of drilling straight down, these wells extend horizontally into an aquifer, capturing water from a wider area.

They are commonly used in municipal water systems, large agricultural operations, and commercial properties where high water demand requires a more efficient and sustainable approach. Horizontal wells can also be beneficial in river valleys or areas with permeable soils, where they tap into natural underground water flow more effectively than a single deep borehole. While their installation is more complex and costly, their ability to increase water yield and reduce drawdown stress makes them a high-value asset for large properties.

In home appraisals, these wells are assessed for installation quality, maintenance requirements, and long-term viability, as they can significantly enhance a property’s self-sufficiency, irrigation potential, and marketability.

Horizontal Wells (Collector Wells)

Depth: Varies; horizontal pipes extend into an aquifer from a central well.

Construction: Drilled horizontally to capture more groundwater flow.

Water Source: Underground springs, water-bearing gravel, or riverbanks.

Common Issues: Complex installation, maintenance challenges.

Best For: Large water supply needs (municipal systems, industries, high-volume irrigation).

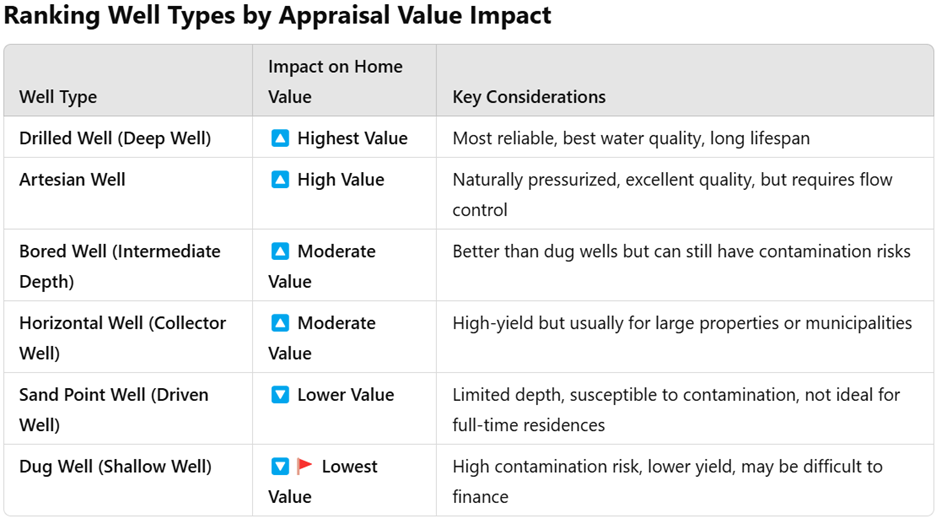

Wells: Appraisal Perspective

As a home appraiser in Canada, the type of well on a property can significantly impact its appraisal value. The well’s reliability, water quality, longevity, and maintenance costs all factor into how lenders, buyers, and insurers assess the home’s worth.

The drilled well (deep well) is the best well type in terms of home value. It provides reliable year-round water supply with a lower risk of contamination. It has the highest water yield, and longest lifespan. A properly maintained drilled well adds the most value to a home because it provides a consistent, high-quality water supply with fewer risks than shallow wells. This is especially true in rural areas where municipal water isn’t available, as buyers want a secure, long-term solution.

The dug well (shallow well) is the worst well type in terms of home value. There is high risk from surface runoff, seasonal fluctuations of water supply and a short lifespan. Water from a shallow well must be treated and frequently tested

Dug wells are seen as outdated and unreliable because they tap into shallow water sources (typically 10-30 ft deep). Many lenders hesitate to approve mortgages on homes with dug wells unless modern filtration or an alternative water source is available. If a home has only a dug well, it can lead to a lower appraisal value and fewer interested buyers.

Questions to Ask About a Well

Well Type & Depth

- What type of well does the property have? (Drilled, Dug, Bored, Sand Point, Artesian, etc.)

- How deep is the well? (Shallow: <50 ft, Intermediate: 50-100 ft, Deep: 100+ ft)

Water Quality & Flow Rate

- Has the water been tested recently? (e.g., bacteria, contaminants, mineral content)

- What is the flow rate in gallons per minute (GPM)? (Less than 3 GPM may be a concern for lenders.)

- Are there any known issues with water quality (e.g., iron, sulfur, hardness, or contamination)?

Age & Maintenance of the Well

- How old is the well? (Older wells may need upgrades.)

- When was the well pump last serviced or replaced?

- Does the property have a well record or past inspection reports?

Property & Location Factors

- Is the property in an area with known water shortages or contamination risks?

- Is the well the primary water source, or is there a backup?

- Is the property in a rural or urban fringe area (as this affects financing concerns)?

Well Documentation

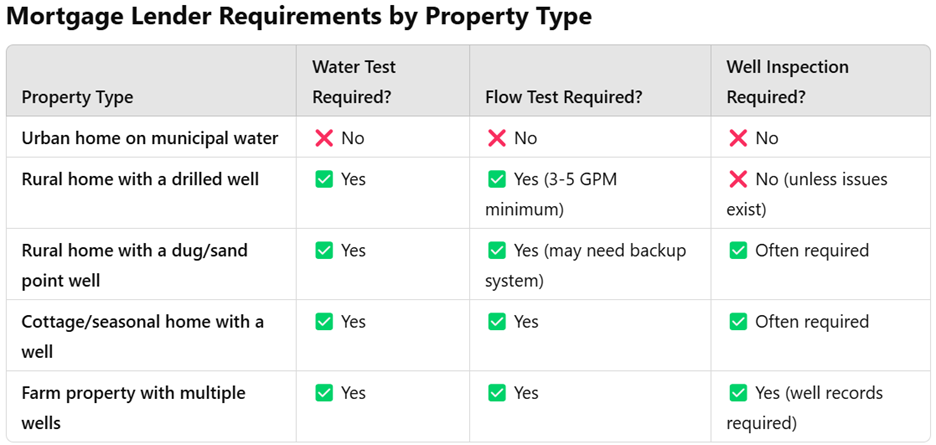

When applying for a mortgage on a property with a well, lenders typically require proof that the water is safe for consumption and provides a sufficient supply for daily use. The required documents generally include:

- Well Water Test Report (Potability Certificate)

- Well Flow Test Report (Yield Test)

- Well Inspection Report (Sometimes Required)

- Well Record (Well Driller’s Report or Well Log)

Well Water Test Report (Potability Certificate)

Issued by: A local public health unit, private lab, or licensed water testing service.

Tests for:

- Bacteria (E. coli & Total Coliforms) – Must be absent for water to be considered safe.

- Nitrates & Nitrites – High levels can indicate contamination.

- Chemical & Mineral Content – Tests for metals (iron, lead, arsenic), hardness, and pH balance.

Validity: Usually within 30 to 90 days before mortgage approval.

How to Get It:

In Ontario, free water testing is available through local public health units.

In other provinces, private labs or well specialists may conduct the test.

Well Flow Test Report (Yield Test)

Issued by: A certified well contractor, hydrogeologist, or licensed well driller.

Tests for:

- Gallons per minute (GPM) flow rate – Lenders typically require at least 3-5 GPM for adequate supply.

- Sustained water pressure – Ensures the well can meet household needs.

- Recovery rate – Measures how quickly the well replenishes after water use.

Validity: Often within 6 months of mortgage approval.

Why It Matters: If the well cannot provide enough water, the mortgage may not be approved without improvements or alternative solutions.

Well Inspection Report (Sometimes Required)

Issued by: A licensed well inspector or certified home inspector specializing in wells.

Includes:

- Well depth & casing condition – Ensures the structure is intact and properly sealed.

- Pump condition – Verifies that the pump is functional.

- Signs of contamination risks – Checks for leaks, cracks, or proximity to septic systems.

When Required: If the well is old, unregistered, or has uncertain maintenance history, lenders may request an inspection before mortgage approval.

Well Record (Well Driller’s Report or Well Log)

Issued by: The original well driller or the provincial well registry.

Includes:

- Date of installation.

- Depth, diameter, and flow rate at the time of drilling.

- Construction details (e.g., casing material, screen type).

How to Get It: In Ontario, well records can be obtained from the Ministry of the Environment, Conservation and Parks (MECP) Well Records Database. Other provinces have similar well registries.

Summary

In Canada, wells are essential for rural and semi-rural properties that lack access to municipal water systems. Different types of wells provide varying levels of reliability, water quality, and long-term viability, all of which impact property value, mortgage eligibility, and desirability.

Drilled wells (deep wells) are the most valuable, offering a consistent, high-quality water supply with minimal contamination risk and long lifespans. These wells are particularly important in areas where municipal water is unavailable, making them a key asset for rural properties.

Dug wells (shallow wells) are the least desirable, as they are highly susceptible to contamination, seasonal drying, and require frequent maintenance, often leading to mortgage financing challenges.

Other well types, such as bored wells, driven wells (sand-point wells), artesian wells, and horizontal wells, vary in usability based on water table depth, soil conditions, and property needs.

When appraising a home, factors like well type, depth, water quality, flow rate, and maintenance history are crucial in determining the property’s value and marketability. Buyers and lenders prioritize secure, reliable water sources, making well functionality a major consideration in real estate transactions.