Owning property in Canada is an attractive prospect for many, from newcomers and investors to Canadian expatriates looking to return home. However, financing a mortgage with funds sourced from outside of Canada presents unique challenges. Lenders, banks, and regulators impose strict scrutiny on international money transfers, requiring borrowers to provide extensive documentation proving the legitimacy of their funds.

For borrowers, understanding the policies surrounding foreign-sourced down payments can mean the difference between a seamless mortgage approval and a frustrating denial. This comprehensive guide explores everything you need to know about using foreign funds for a down payment, from legal requirements to practical strategies for ensuring lender acceptance.

The Legality of Using Foreign Funds in Canada

Source of Foreign Funds: What Lenders Want to See

Currency Exchange Considerations

The Role of Canadian Banks in Accepting Foreign Funds

High-Risk Countries: Where Funds May Not Be Accepted

AML Compliance and Source of Funds Verification

The Impact of Foreign Funds on Mortgage Default Insurance Eligibility

Gifted Foreign Down Payments: Acceptable or Not?

Private Lenders vs. Banks: Which One is More Flexible?

The Legality of Using Foreign Funds in Canada

Canada permits the use of foreign funds for real estate purchases, but strict oversight is in place to prevent illicit financial activity. The Financial Transactions and Reports Analysis Centre of Canada (FINTRAC) monitors large financial transfers, ensuring all transactions align with anti-money laundering (AML) laws.

Lenders require borrowers to prove that their funds were obtained legally. Simply transferring money into a Canadian account isn’t enough; a clear paper trail must accompany the funds.

All financial institutions and lenders in Canada are required to:

- Report large cash transactions over $10,000.

- Identify the source of foreign funds.

- Flag and investigate suspicious financial activity.

The onus falls on the borrower to demonstrate the legitimacy of their foreign funds. Simply having money in a bank account is not enough—lenders require detailed documentation to confirm that the funds are derived from lawful sources.

Source of Foreign Funds: What Lenders Want to See

Lenders in Canada assess the origin of foreign funds before approving them for a mortgage down payment. To satisfy lender requirements, borrowers must provide evidence that the funds come from an acceptable source.

Acceptable Sources of Foreign Funds

Lenders typically accept foreign funds that can be traced back to:

- Personal Savings – Earnings from legitimate employment, whether self-employed or salaried.

- Sale of Property – Proceeds from selling real estate abroad.

- Investment Liquidation – Stocks, bonds, or other financial assets converted into cash.

- Inheritance – Money received from a deceased relative (with legal documentation).

- Gift from Immediate Family – A documented financial gift from parents or close relatives.

Unacceptable or High-Risk Sources

Some sources of funds raise red flags with lenders:

- Large Unexplained Cash Deposits – Without clear documentation, these are often rejected.

- Unverified Wire Transfers – If the sender’s identity and reason for the transfer cannot be validated.

- Transfers from Sanctioned Countries – Countries under financial sanctions are prohibited.

- Undocumented Business Transactions – Business income without official tax records may be declined.

Having an unambiguous and verifiable paper trail is crucial to securing mortgage approval.

Documentation

The documentation serves to verify the origin, legitimacy, and transfer process of the funds.

Bank Statements

Lenders need to trace the movement of funds over time to ensure they were legally acquired.

Lenders may require:

- Recent bank statements (3 to 6 months) from the overseas account where the funds originated showing account history, sale of assets, investment statements, etc.. Some lenders may accept funds transferred just before closing, as long as there is a documented trail proving their origin from the originating country.

- Proof of Transfer to Canada: Lenders will require proof that the funds have been transferred from another country to a Canadian bank account under the client’s name. Bank statements showing the wire transfer and currency conversion may be required.

- The full statement, including account holder details, transaction history, and balances.

- Explanations for large deposits—if a significant sum appears suddenly, the lender will request additional proof of origin.

Tip: The bank statement must be an official document from the financial institution—screenshots or partial statements are often rejected.

Proof of Income

Lenders must confirm that the borrower or donor has a legitimate source of income that could have generated the funds.

What You May Need to Provide:

- Employment Verification Letter – Stating income, position, and length of employment.

- Pay Stubs (3 to 6 months) – If the funds were saved from salary earnings.

- Tax Returns (Last 2 years) – To prove income consistency.

- Bank Statements Showing Salary Deposits – If income was earned from employment.

- Profit and Loss Statements (if self-employed) – Business owners must provide financials prepared by an accountant.

Tip: If the income is from a foreign employer, some lenders may request a letter translated into English and notarized.

Document Translation

In Canada, the mortgage application process is highly regulated, requiring strict compliance with financial and legal documentation standards. For borrowers whose mortgage application documents are in a language other than English or French, lenders demand certified translations to ensure clarity, consistency, and compliance with lending policies.

The challenge? Not all translations are created equal. Poorly translated documents can delay approvals, trigger compliance red flags, or even lead to a rejected mortgage application. Whether it’s a bank statement, income verification, or property sale agreement, getting it professionally translated is not just an administrative task—it’s a critical step toward homeownership.

READ MORE: Getting Mortgage Documents Translated

Currency Exchange Considerations

Foreign funds must eventually be converted into Canadian dollars (CAD), and the exchange rate can significantly impact the total amount available for the down payment.

Best Practices for Currency Conversion

- Monitor Exchange Rates – Rates fluctuate daily, and minor shifts can affect affordability.

- Use a Reputable Currency Exchange Service – Some services offer better rates than major banks.

- Avoid Last-Minute Conversions – Converting large sums at once may expose borrowers to sudden market fluctuations.

Exchange rates can increase or reduce the amount available for a down payment, so timing and method of conversion are critical.

Schedule II Banks

Another possible approach is to work with me to get your mortgage from a Schedule II bank. Schedule II banks are foreign subsidiaries of banks of other countries. For example, Shinhan Bank of Canada is a foreign subsidiary of Korea’s Shinhan Bank. They are happy do a down payment in either Canadian dollars or South Korean Won (KRW). Let me find for you the appropriate Schedule II bank from the country you are originating from and see if that is a possibility for you.

Timing the Transfer: How Long Should the Money Sit in Canada?

Most lenders prefer that foreign funds be seasoned—meaning they must sit in a Canadian bank account for at least 90 days before they can be used for a mortgage.

Why Do Lenders Require a Waiting Period?

- It establishes legitimacy and ensures the funds are not proceeds of financial crime.

- It prevents last-minute fraud attempts.

- It gives lenders ample time to conduct due diligence.

However, some lenders make exceptions for borrowers who can provide extensive documentation proving the source of the funds.

The Role of Canadian Banks in Accepting Foreign Funds

Not all Canadian banks have the same policies regarding international transfers. The process of moving money from an overseas account can vary significantly depending on the financial institution.

What Borrowers Need to Know

- Major Banks (RBC, TD, Scotiabank, BMO, CIBC) have strict regulations and may reject funds from high-risk countries.

- Alternative Lenders (credit unions, trust companies) sometimes are be more flexible with foreign deposits but other times they are the most restrictive (lender dependent).

- International Banks with a Canadian Presence (HSBC, ICICI, Bank of China) can facilitate smoother fund transfers.

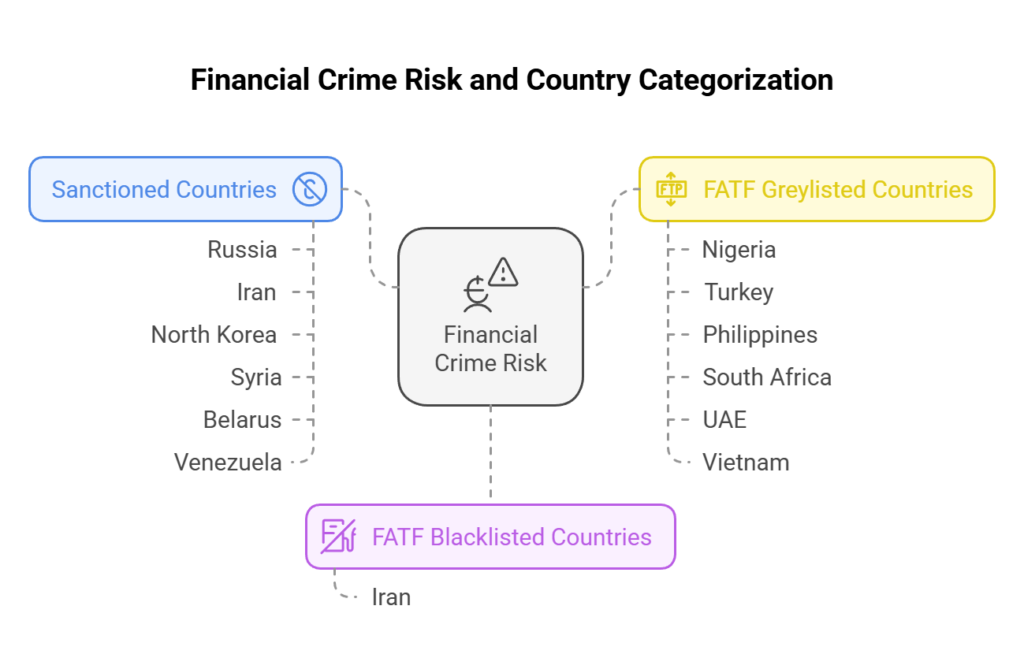

High-Risk Countries: Where Funds May Not Be Accepted

Some countries are flagged as high-risk for financial crimes, and lenders are often reluctant to accept funds from these jurisdictions.

Sanctioned Countries (Funds Not Accepted)

- Russia

- Iran

- North Korea

- Syria

- Belarus

- Venezuela

FATF Blacklisted Countries (Severe Scrutiny Required)

- Iran

FATF Greylisted Countries (Extra Documentation Required)

- Nigeria

- Turkey

- Philippines

- South Africa

- UAE

- Vietnam

If funds originate from one of these high-risk regions, lenders may reject the application outright or request extensive additional proof.

For more information, see Global Affairs Canada

AML Compliance and Source of Funds Verification

To comply with AML regulations, borrowers must provide:

- Bank statements showing account history.

- Proof of earnings, such as pay stubs or tax returns.

- Legal documents for inherited or gifted funds.

- Transaction records for property sales or asset liquidation.

If a lender suspects any irregularities, they may request additional documents or even decline the application.

The Impact of Foreign Funds on Mortgage Default Insurance Eligibility

If a down payment is less than 20%, the mortgage requires default insurance from CMHC, Sagen, or Canada Guaranty. These insurers have strict requirements regarding foreign down payments.

- Funds must be verified and seasoned.

- Lenders may reject funds from high-risk regions.

- Additional scrutiny applies to non-residents and new immigrants.

Buyers using foreign funds must ensure their down payment complies with insurer guidelines.

Gifted Foreign Down Payments: Acceptable or Not?

Gifted down payments from immediate family are generally accepted, but they must be accompanied by:

- A formal gift letter.

- Proof of the donor’s ability to provide the funds.

- Bank statements showing the transfer.

Some lenders do not accept gifts from overseas, so borrowers should verify policies beforehand.

Private Lenders vs. Banks: Which One is More Flexible?

If a traditional bank refuses foreign funds, private lenders may offer an alternative solution.

Differences Between Banks and Private Lenders

| Feature | Traditional Bank | Private Lender |

| Foreign Fund Acceptance | Strict | More Flexible |

| Documentation Required | Extensive | Less Rigid |

| Interest Rates | Lower | Higher |

| Speed of Approval | Slow | Faster |

While private lenders offer greater flexibility, they often charge higher interest rates and fees.

Summary

Using foreign funds for a mortgage down payment in Canada is possible, but it requires careful planning, proper documentation, and compliance with AML laws. Borrowers should transfer funds well in advance, work with financial professionals, and choose the right lender to avoid last-minute mortgage approval issues. With the right approach, they can successfully finance their dream home in Canada.