… The Strategic Middle Step Between Private and Prime

Most people don’t wake up and say, “I’d love to pay 1–2% more than the bank for my mortgage.”

You want the lowest rate possible. Of course you do. That’s rational.

Sometimes the lowest rate isn’t the smartest first move. Sometimes the smartest move is the right lender for your situation — and that’s where Community Trust (CT) fits.

Community Trust isn’t a private lender charging 10–12%. It’s not a prime bank either. It’s a structured alternative lender — typically 1–2% above prime — designed for borrowers who are viable, responsible, and real… but just slightly outside the tight boxes banks use.

Let’s walk through when it makes sense to use Community Trust — and when it doesn’t.

What I’ll Cover

When You’re Paying Off a Private Mortgage

When Your Debt Levels Are Just Over Bank Limits

When You’re Self-Employed and Your Income Doesn’t Underwrite Cleanly

When You’ve Co-Signed for Someone Else

When You Have Assets but Limited Income

When Community Trust Is Not the Right Choice

Story: From Private to Stable#A-Story:-From-Private-to-Stable

When You’re Paying Off a Private Mortgage

This is one of the strongest use cases.

Maybe you used private money to:

- Build a property

- Finish a renovation

- Get through a credit issue

- Close quickly when a bank couldn’t

Now you’re paying 9%, 10%, maybe more. You want out. Totally fair.

You go to a bank. They look at your file and say:

“Sorry. Your total debt payments are too high compared to your income.”

Here’s what that means in plain English.

Banks add up:

- Your mortgage payment

- Property taxes

- Heating costs (they use a standard number)

- Car loans

- Credit cards

- Lines of credit

- Student loans

- Any required monthly debt payment

They divide that by your gross income (before tax). Most prime lenders cap that at 44%.

If you’re at 45%, 47%, 48%? Declined.

Community Trust allows:

- Up to 50% as standard

- Up to 60% in certain strong credit cases

That 6–16% difference can mean the difference between staying in expensive private debt and moving into something far more manageable.

In this case, CT becomes a structured step off private — not the final destination, but the bridge.

When Your Debt Levels Are Just Over Bank Limits

Let me give you a real-world example.

You earn $8,000 per month before tax.

Your combined monthly debts look like this:

- Mortgage: $2,800

- Taxes: $400

- Heating: $150

- Car loan: $600

- Credit cards: $350

- Line of credit: $300

Total: $4,600

$4,600 ÷ $8,000 = 57.5%

A bank capped at 44% would only allow $3,520. You’re not even close.

Community Trust, allowing up to 60%, would allow $4,800.

Same person. Same income. Same bills. Different outcome.

You’re not reckless. You’re just outside the prime formula.

When You’re Self-Employed and Your Income Doesn’t Underwrite Cleanly

You write off expenses. That’s smart tax planning.

But your tax return might show less income than you actually live on.

Banks typically want:

- Two-year average income

- Clean Notice of Assessment history

- Strict documentation

Community Trust can use:

- 12 months of bank statements

- Accountant letters

- More flexible income analysis

If your income is real but doesn’t present neatly on paper, CT can often see what the bank can’t.

When You’ve Co-Signed for Someone Else

This one catches people all the time.

You helped your child buy their first home. You co-signed.

Now you want to refinance your own property. The bank includes that entire mortgage payment in your debt calculation — even though you’re not paying it.

Community Trust will remove that debt from the calculation if you can show three months of proof the other party is making the payments.

That can dramatically improve your approval chances.

When You’re Rebuilding Credit

Life happens.

Consumer proposal. Late payments. Rough patch.

Prime lenders often have automatic decline triggers.

Community Trust may consider:

- Active consumer proposals (at capped loan amounts)

- Past mortgage arrears

- Lower credit scores with strong compensating factors

You still need a solid story. You still need structure. But you’re not automatically disqualified.

When You Have Assets but Limited Income

Maybe you’re retired.

Maybe you’re between jobs.

Maybe you have substantial savings, RRSPs, or investments — but not strong employment income.

Banks require income.

Community Trust has a net-worth approach (typically up to 65% of the property value) where, if your liquid assets can cover the mortgage payments for the term, income restrictions may not apply the same way.

That’s a powerful niche.

A Story: From Private to Stable

Let me tell you about “Mark.”

Mark built a duplex. Construction ran long. Costs crept up. He finished with private financing at 10.5%.

Once complete, he wanted out. He went to a bank.

Declined.

Why? His combined monthly obligations — including two car loans and a line of credit — put him at 46% of his income. The bank’s cap? 44%.

Two percent difference. That’s it.

We moved him to Community Trust at a rate about 1.5% higher than prime — but far lower than private.

His monthly payment dropped substantially. His cash flow stabilized. He now has a clear path to prime at renewal.

That’s how you use CT properly.

When Community Trust Is Not the Right Choice

Let’s be clear.

If you:

- Qualify comfortably under 44% of income

- Have strong credit (700+)

- Have stable documented income

- Own a standard property

Prime will be cheaper. Full stop.

There’s no reason to pay 1–2% more if you don’t need the flexibility.

Community Trust also isn’t ideal for active construction draw financing. It works better once a property is complete and ready for permanent financing.

How Realtors and Clients Can Use This Strategically

Realtors:

If you have a listing where the seller is stuck in private debt and struggling with payments, this could be the bridge that saves the deal.

If your buyer is solid but slightly over bank ratios, this could prevent a collapse.

Clients:

If you’ve been declined by a bank, don’t assume you’re unqualified. It may simply be a formula issue — not a financial irresponsibility issue.

Allen’s Final Thoughts

Community Trust isn’t a “backup plan.”

It’s a strategic middle step.

Private → Community Trust → Prime.

It charges 1–2% more than banks because it offers flexibility banks won’t.

Used correctly, it can:

- Get you off private

- Stabilize your payments

- Buy you time to repair credit

- Structure income properly

- Remove qualification obstacles

Used incorrectly, it’s unnecessary.

My job as your mortgage agent is not just to find you a lender.

It’s to map out the smartest path — sometimes that’s prime immediately. Sometimes it’s a year or two with an alternative lender like Community Trust. Sometimes it’s sequencing lenders deliberately.

I’ll analyze:

- Your debt structure

- Your income presentation

- Your credit profile

- Your long-term goals

Then we’ll build a strategy — not just get an approval.

If you’re wondering whether Community Trust makes sense for you, let’s have that conversation. We’ll look at the numbers together and decide if it’s the right middle step — or if we can go straight to the finish line.

Client Summary

Community Trust Mortgages

If you’ve been told you don’t quite fit the bank’s box — or you’re worried your situation is “too complicated” — Community Trust (CT) may be a strong alternative lender worth considering.

They are not a typical big bank. They specialize in flexibility. That means they look beyond just your credit score and income type. Let’s walk through what that really means for you.

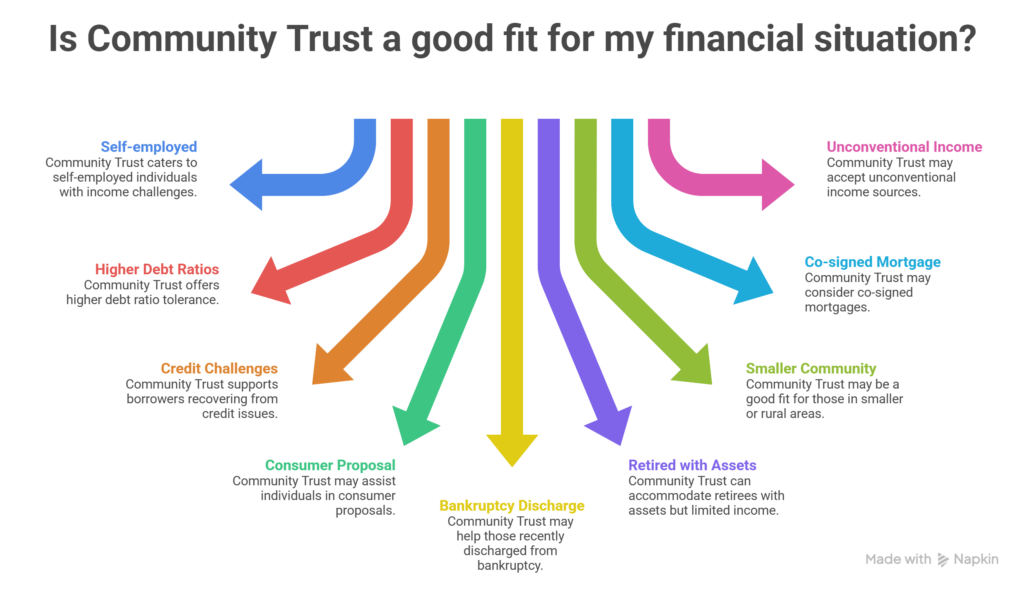

Who Community Trust Is Best For

Community Trust may be a good fit if you are:

- Self-employed or business-for-self

- Carrying higher debt ratios

- Recovering from credit challenges

- In a consumer proposal

- Recently discharged from bankruptcy

- Retired with assets but limited income

- Living in a smaller or rural community

- Co-signed on someone else’s mortgage or loan

- Using unconventional income sources

They are designed to help borrowers who don’t qualify with traditional lenders.

How Much Can You Qualify For?

Higher Debt Service Flexibility

Most lenders cap your total debt payments at around 44–48% of your income.

Community Trust:

- Standard limit: 50%

- High credit program: up to 60% (if you have strong credit)

This can make the difference between qualifying and being declined.

If You’re Self-Employed

Community Trust offers flexible options:

- 12-month bank statement programs

- Use of accountant letters (instead of full financials in some cases)

- Net income focus for incorporated borrowers

- Add-backs for depreciation and amortization

If your income fluctuates or doesn’t look strong on paper, they may still be able to structure something workable.

If You’ve Had Credit Issues

Community Trust can consider:

- Active consumer proposals (up to 70% loan-to-value)

- Mortgage arrears (case-by-case)

- Multiple bankruptcies (with explanation)

- No credit history (using alternative credit like rent + utilities)

They focus on the story behind the credit, not just the score.

If You’re Retired or Asset-Rich

One of their most unique programs is their “Net Worth” option.

If you have sufficient liquid assets (RRSPs, TFSAs, savings, mutual funds):

- You may qualify without traditional income ratios

- Assets must cover mortgage payments and taxes for the term of the mortgage

- Maximum 65% loan-to-value

This is especially helpful for retirees or clients between jobs.

If Someone Helps You With Payments

Community Trust allows two powerful options:

1. Contributory Income

If someone lives with you and contributes to expenses:

- Their income can help you qualify

- They do not need to be on title

- Ratios must remain under 50%

2. Removing Co-Signed Debt

If you co-signed for someone else:

- Provide proof they are making the payments

- That debt can be removed from your qualification

- This can significantly improve approval odds

Very few lenders allow this.

Rental & Investment Properties

- Up to 6 total properties allowed

- 90% rental income offset

- 35-year amortization available (in some cases)

- High-rise condos capped at 75% loan-to-value

They also ignore properties held in corporations (holdcos) when qualifying you personally — which is helpful for seasoned investors.

Flexible Income Sources Accepted

Community Trust may accept:

- Child tax benefits

- Disability income

- Foster income

- Foreign pensions

- Rental income

- Crypto proceeds (fully documented)

- Gold proceeds (with proper documentation)

They do not typically use car or housing allowances.

Lending in Smaller Communities

Community Trust is comfortable lending in towns and smaller markets where some lenders restrict approvals.

They can go up to 80% loan-to-value in many secondary markets, depending on credit strength.

What to Expect

- Rates are typically higher than major banks (this is an alternative lender).

- Lender fees apply.

- Documentation matters — a clear explanation of your situation is key.

- Turnaround times are improving and generally competitive.

This is a structured alternative solution — not a last resort, but not prime banking either.

Is Community Trust Right for You?

Community Trust works best when:

- You need flexibility.

- Your income doesn’t fit traditional underwriting.

- You are rebuilding or restructuring.

- You have strong assets but limited income.

- You need a bridge back toward prime financing.

For many borrowers, it becomes a stepping stone lender — helping you restructure today so you can qualify with a major bank later.