A second mortgage is a loan that is secured against a property that already has an existing mortgage. It is considered “second” because it is subordinate to the first mortgage in terms of priority—meaning that if the homeowner defaults, the first mortgage lender gets paid first, and the second mortgage lender gets paid only after the first loan is settled.

Many lenders do not like or permit a second mortgage to be behind them. Lenders take on significant risk when offering mortgages and allowing a second mortgage behind their first mortgage can increase their exposure to potential losses.

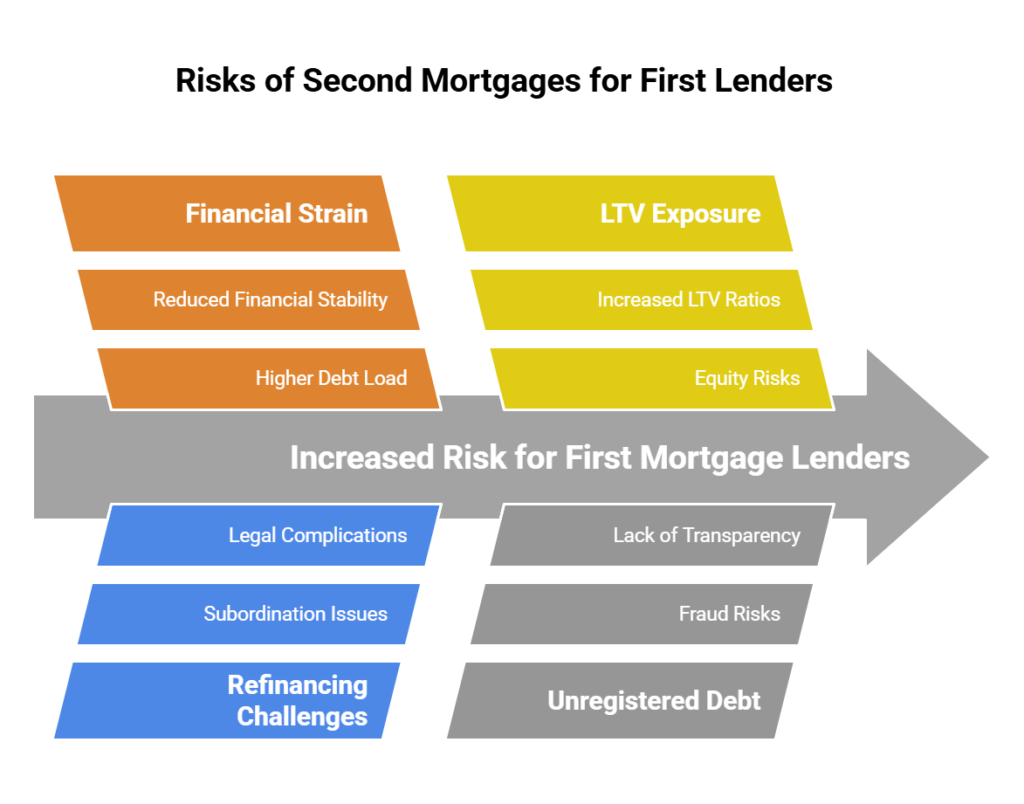

Let me share why many lenders do not allow second mortgages behind their first mortgage.

Increased Risk in Case of Default

Reduced Control Over the Borrower’s Financial Stability

Complications in Refinancing and Subordination Issues

Higher Loan-to-Value (LTV) Exposure

Potential for Increased Power of Sale

Risk of Fraud and Unregistered Debt

Lender-Specific Policies and Legal Clauses

Which Lenders are Most Likely to Prohibit Second Mortgages?

Which Lenders Typically Allow Second Mortgages?

Increased Risk in Case of Default

The biggest concern for a first mortgage lender is what happens if the borrower defaults. The first mortgage lender has the first claim on the property in a foreclosure or power of sale. If a second mortgage exists, it adds to the borrower’s debt load, making it harder for them to keep up with payments. If the home is sold under distressed conditions, there may not be enough equity to repay both mortgages. If home values decline, the second mortgage lender loses their security first, and the first mortgage lender may also face a loss.

Example:

A borrower has a home worth $500,000 and a first mortgage of $400,000. If they take out a second mortgage of $50,000, their total loan-to-value (LTV) increases to 90%.

- If the market drops and the home is now worth $450,000, foreclosure may not recover the full amount of the debt, increasing the lender’s risk.

Reduced Control Over the Borrower’s Financial Stability

When a borrower takes out a second mortgage, it often indicates higher financial strain. Some borrowers take second mortgages to consolidate high-interest debt, but in some cases, this does not improve financial stability.

If a borrower takes out a second mortgage without informing the first lender, their risk profile increases without the lender’s knowledge.

Lender’s Concern: The first lender has no control over how much additional debt the borrower takes on, which could jeopardize their ability to make first mortgage payments.

Complications in Refinancing and Subordination Issues

If a borrower wants to refinance their first mortgage while a second mortgage exists, it creates a legal and financial challenge for the lender.

When a first mortgage is refinanced, the original loan is discharged, and the second mortgage automatically moves into first position unless a subordination agreement is signed.

The second mortgage lender must agree to subordination, and if they refuse, the first lender cannot regain first position. This can cause delays in refinancing and create administrative and legal burdens for the lender.

Example:

A borrower with a first mortgage from TD Bank and a second mortgage from a private lender wants to refinance.

- If the private lender refuses to sign a subordination agreement, the new first mortgage lender might decline the refinance.

- This can trap borrowers in higher-rate mortgages.

Higher Loan-to-Value (LTV) Exposure

Lenders prefer lower LTV ratios to minimize their risk. When a second mortgage is added:

- The combined LTV (first mortgage + second mortgage) increases.

- Higher LTV means less equity, and if property values decline, there is a greater risk of negative equity.

- Lenders may decline second mortgages if they push the total LTV beyond 80%.

Example:

A lender might be comfortable lending $400,000 on a $500,000 home (80% LTV).

If a second mortgage is added and pushes the total loan amount to $450,000, the lender may not allow it due to increased risk.

Mortgage Insurers Prohibit It

If a mortgage is insured by CMHC, Sagen, or Canada Guaranty, second mortgages are not permitted behind the insured loan.

- Insured mortgages are for borrowers with less than 20% down, meaning they already have high LTV.

- Allowing a second mortgage would increase the borrower’s leverage beyond 100% LTV in some cases, which is too risky.

Potential for Increased Power of Sale

Lenders want to avoid Power of Sale, which are costly and time-consuming.

If a borrower has two mortgages, they have two different lenders trying to collect on the property. If they default, the second mortgage lender may start foreclosure proceedings first, forcing a legal process that complicates things for the first mortgage lender.

This increases the likelihood of the borrower losing their home and the lender incurring losses.

Risk of Fraud and Unregistered Debt

Some lenders worry about borrowers taking unregistered second mortgages (e.g., private loans, vendor take-back mortgages) that don’t appear on title. This increases the borrower’s debt load without the first lender knowing.

If the borrower defaults, the lender may realize too late that the borrower had more debt than expected.

Lender-Specific Policies and Legal Clauses

Some lenders include a due-on-encumbrance clause in their mortgage contracts.

This clause prohibits the borrower from taking additional secured loans without the lender’s approval. If the borrower violates this clause, the lender could demand full repayment of the first mortgage immediately.

Which Lenders are Most Likely to Prohibit Second Mortgages?

- Big Banks (RBC, TD, Scotiabank, CIBC, BMO, National Bank) – Often require strict approval before allowing second mortgages.

- Monoline Lenders (First National, MCAP, RFA, Equitable Bank, Lendwise) – Some prohibit second mortgages due to refinancing complications.

- Mortgage Insurers (CMHC, Sagen, Canada Guaranty) – Do not allow second mortgages behind an insured first mortgage.

- Lenders with Low-Interest Rates – Some lenders only offer low rates if they hold the only mortgage on title.

Which Lenders Typically Allow Second Mortgages?

- Credit Unions – Often allow second mortgages, but may charge higher rates or require both mortgages to be held by them.

- Alternative (B) Lenders – More likely to permit second mortgages, but may impose higher LTV restrictions.

- Private Lenders – Almost always allow second mortgages but charge significantly higher rates (8%–15%).

READ MORE:

Understanding Subordination Agreements

Why Lenders Don’t Like Seconds

Summary

Not all lenders allow second mortgages behind them because it increases risk, reduces their control over the borrower’s finances, and complicates refinancing. While some institutional lenders are flexible, others have strict policies prohibiting second mortgages, particularly if the first mortgage is insured or high-ratio.

Before taking out a second mortgage, borrowers should:

- Check their lender’s policy on second mortgages.

- Understand the risks of higher LTV and foreclosure.

- Consider alternative lenders if their primary lender does not allow it.

A second mortgage can be a powerful financial tool—but only when used strategically within lender-approved guidelines.