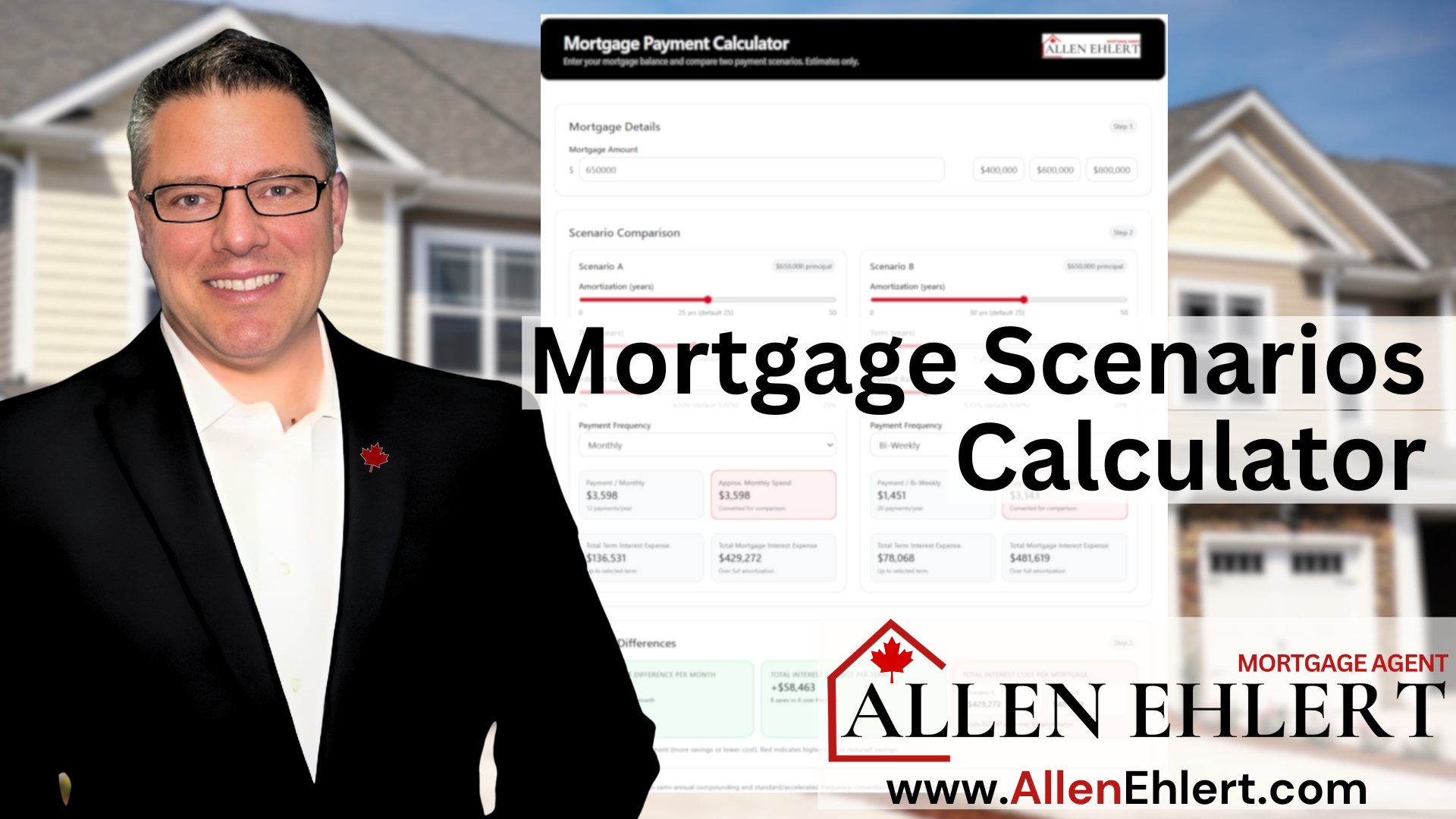

Mortgage Articles

Your Way to Your Best Life!

The Truth About “Limited Feature Mortgages”

We’ve all seen them — those ultra-low mortgage rates advertised by the big banks or online lenders. They’re tempting, no doubt about it. Who doesn’t want to save a few bucks on interest? But here’s what you might not realize: those “basic,” “no-frills,” or “limited feature” mortgages come with some fine print that can cost you more down the road than you save upfront.

How Maternity Leave Impacts Your Mortgage

If you’re thinking about buying a home, refinancing, or renewing your mortgage and there’s a baby on the horizon, you might be wondering how maternity or paternity leave fits into the picture. The truth? Lenders love stability — and nothing signals “change” quite like stepping away from your full-time salary to focus on your family, even temporarily.

Smart Ways to Pay Off Credit Card Debt

Smart Ways to Payy off Credit Card Debt. If you’re staring down a mountain of credit card debt — say $60,000 or so — you’re not alone. Between rising living costs, high interest rates, and a few life curveballs, it doesn’t take much for balances to spiral out of control. When that happens, most people start thinking, “Maybe I should just use my home equity to wipe this out.”

How to Write Off Mortgage Interest in Canada

Unlock tax benefits by learning how to write off your mortgage interest in Canada. Follow my guide for smart tax deductions and relief strategies.

Comparing Co-Signor and Guarantor

In Ontario, Canada, the obligations to pay when a mortgage payment is missed differ between a guarantor and a co-signer. Understanding the differences between these roles can help clarify the responsibilities involved in guaranteeing or co-signing a mortgage.

How Much Does an Appraisal Cost in 2025

The process of determining the fair market value of a property plays a crucial role in real estate transactions, mortgage refinancing, and insurance purposes. If you’re looking to buy, sell, or refinance a property, understanding the cost of a home appraisal is essential.

Don’t Get Your HELOC There!

Don’t get your HELOC there! It seems logical. You know the bank, they know you, and it feels easier to keep everything under one roof. But just because something’s convenient doesn’t mean it’s smart. When it comes to tapping your home equity, the bank that holds your mortgage might not actually give you the best deal — or the most flexibility.

How Canada’s Prime Rate Impacts You

Explore how Canada’s Prime Rate affects your mortgage, investments, and savings. Stay informed and manage your finances with confidence.

5 Smart Ways to Save on Legal Fees

5 ways to save on legal fees: Buying a home (or refinancing one) is exciting — but when you add up land transfer tax, legal fees, and all the little “extras,” it can feel like death by a thousand cuts. One of the most common questions I get as a mortgage agent is: “Allen, how can I save on legal fees?”

Home Equity to Pay Off Debt Doesn’t Add Up

Debt Consolidation: Using your home equity to clear debt doesn’t always make sense. Sometimes, after factoring in mortgage penalties, fees, and timelines, what seems like the smart move can end up costing more than doing nothing at all.

Understanding Mortgage Bona Fide Sales Clause

Explore the essentials of a Mortgage Bona Fide Sales Clause and its impact on your property transactions in Canadian real estate.

How Much are Legal Fees?

Legal Fees: Buying a home in Canada is a huge milestone — but it can also feel like a never-ending list of fees, forms, and fine print. One of the most common surprises for homebuyers is legal fees. You know you need a lawyer, but what exactly are you paying for? And why do some mortgages come with higher legal costs than others?

Does Size Really Matter?

When it comes to mortgages, people often obsess over interest rates, terms, and approval criteria — but one question flies under the radar until it suddenly becomes a problem:

“Does the size of the home matter to the lender?”

Credit Score and Your Mortgage

Understand how your Credit Score affects mortgage rates in Canada and learn ways to enhance it for better loan terms.

Non-Resident Speculation Tax

Understand the Non-Resident Speculation Tax and its impact on Ontario’s real estate market. Find out if you’re affected and how to comply.

Property Appraisal Process

Discover how the property appraisal process can ensure accurate real estate valuation for your investments in Canada. Learn appraisal essentials today.

Understanding Second Mortgages

There’s a lot of buzz out there about second mortgages. You hear about people using them to pay off debt, help kids buy homes, or fund renovations. They sound like a simple solution — and sometimes they are. But second mortgages aren’t just a financial hack you pull out of thin air. They come with rules, restrictions, and some real fine print that’s easy to overlook.

Reverse Mortgage to a Second Dream Home

A reverse mortgage is often assumed to be a reactive option for a senior homeowner in financial need, but it’s not always the case. In fact, there are situations when a reverse mortgage can be used proactively to unlock financial opportunities.

Struggling Financially as a Senior

As a senior, it seems nothing gets any easier … especially when it comes to money. Everything gets more expensive all the time. Bills go up, taxes go up… things can get very scary! You are lucky if you have a pension, but most of those don’t keep up with today’s inflation and cost of living. It doesn’t seem fair to have worked so hard your entire life only to struggle right to the end.

Appraisal Institute of Canada (AIC)

In Canada, the primary professional body that oversees home appraisals is the Appraisal Institute of Canada (AIC). The AIC sets the standards and regulations for the appraisal profession across the country.

How I Vet Mortgage Documents to Protect Your Deal

Let’s be real — in real estate, everyone plays a role. The realtor sells the dream, the lawyer protects the paperwork, but when it comes to vetting the financials, that’s where I step in. As a mortgage agent, it’s my job to protect the integrity of the deal before it ever reaches a lender’s underwriter. I’m the one who spots the inconsistencies, asks the awkward questions, and makes sure that everything adds up — literally and figuratively.

Reverse Mortgage: Cushion Against Inflation

When the cost-of-living spikes, many workers can rely on salary increases to keep pace, while retired public servants with indexed pensions may also be somewhat protected. Retirees with pensions that aren’t inflation-adjusted have more cause for concern; however, if...

The Deal Breakers: Unacceptable Property Types

You’ve found the “perfect” property — it’s quirky, unique, maybe even a little outside-the-box. You’re already mentally arranging furniture and planning summer BBQs… and then your mortgage agent drops the bomb: “The lender won’t finance it.”

Why Honest Mortgage Docs Matter

Getting a mortgage isn’t like applying for a gym membership. It’s not about looking good on paper for five minutes—it’s about proving you can carry the weight for the next twenty-five years. Lenders aren’t just handing out keys to anyone who asks. They need to trust that what you’re telling them is the truth: your income, your savings, your credit, and your job are all what you say they are.

Funding Your Retirement: Reverse Mortgage

A reverse mortgage is a timeless financial tool that can be useful for many seniors who own their home. While it may not be the first option that comes to mind, it can be a viable strategy for homeowners even though interest rates have risen.

A Commitment Isn’t a Guarantee

You’ve done everything right—you got pre-approved, made your offer, provided every bank statement and pay stub under the sun. The lender issues a written mortgage commitment and you think, “Phew, we’re done.” Not so fast. A lot of homebuyers (and even some seasoned realtors) mistake a commitment letter as some kind of iron-clad promise. It’s not.

Reverse Mortgages and the Affluent Retiree

Reverse mortgages are an often misunderstood or overlooked financial tool. One critique is that a reverse mortgage may reduce the inheritance a senior can leave to their family, but that is not always the case. In fact, in some cases, a reverse mortgage may be a...

Your Mortgage Refinance Options

A few years ago, you purchased your home. At the time, you secured a mortgage that was suitable for your financial situation. However, as time goes on, things change, interest rates are not the same and your own financial situation is different; maybe better, maybe...

Reverse Mortgage: Independent Legal Advice (ILA)

A reverse mortgage is offered to Canadians 55 years of age and older and is of particular interest to homeowners who want to access a portion of their home equity for a wide variety of reasons including to fund their retirement years, purchase a second home, cottage, or rental property, to help children purchase a home, to address unexpected expenses, and much, much more.

How Long to Get a Written Mortgage Commitment

You’ve got the house. The offer’s accepted. You’ve told your family, picked out paint colours, and maybe even started scoping out where the Christmas tree’s going to sit. But now comes the part that isn’t quite as exciting but is absolutely crucial — locking down your written mortgage commitment.

What Happens When the Mortgage Falls Apart?

It’s one of the scariest “what if” scenarios in real estate: the buyer waives the financing condition, the deal goes firm, and then… BAM! The lender says, “Sorry, we can’t fund this anymore.” Suddenly, everyone’s scrambling—buyers, sellers, agents, lawyers—and what started as a celebration becomes a nightmare of deposits, lawsuits, and finger-pointing.

Understanding ‘Approval’ Terminology

If you’ve ever been through the mortgage process, you’ve probably heard people throwing around words like pre-qualification, pre-approval, commitment, and funding like they’re all interchangeable. Spoiler alert: they’re not. And if you don’t understand the difference, you could find yourself in hot water right when you’re trying to buy your dream home.

Strive: Rental Property Lender

As a licensed mortgage agent committed to helping Canadians build long-term wealth through real estate, I make it a priority to introduce my clients to lenders who think beyond rigid formulas — lenders who understand the unique needs of rental property investors. One such lender making a name for itself across Canada is Strive.

Doing the Financial Work

You’ve got a lot on your plate—family, work, keeping the house in one piece—and then a mortgage renewal letter shows up. At first glance, it feels like a gift: a quick signature and you’re done for another five years. But here’s the thing—that first offer from your lender? It’s almost never their best. They’re betting you won’t question it. They’re counting on you not wanting to “do the financial work.”

Ultimate Canadian Spousal Buy Out Calculator

When those relationships end, the emotional toll is heavy—but the financial questions can hit just as hard. Who gets the house? How much is one partner entitled to? Can one partner afford to buy the other out without selling the family home?

That’s where Allen Ehlert’s Ultimate Canadian Spousal Buy Out Calculator comes in. It’s designed to take some of the mystery—and stress—out of a separation by giving you the numbers you need to move forward. Whether you’re divorcing or separating as common-law partners, this calculator helps you figure out exactly what a buyout looks like.

Non-Resident Speculation Tax Rebate

Foreign buyers who have paid the 25% Non-Resident Speculation Tax (NRST) may be eligible for a full rebate if they meet specific residency, employment, or education requirements within a set period. The Ontario government provides these rebates to encourage long-term...

Spousal Buyout Mortgages: Start Fresh

A spousal buyout mortgage is a smart solution that lets one spouse keep the home, refinance the mortgage, and pay out the other spouse’s equity.

Featured Publications

Articles

- Extended Amortizations and Hypothetical Calculations

Office of the Superintendent of Financial Institutions (OSFI) - Minimum Qualifying Rate for Uninsured Mortgages

Office of the Superintendent of Financial Institutions (OSFI) - Residential Mortgage Underwriting Practices and Procedures

Office of the Superintendent of Financial Institutions (OSFI) - Guideline on Existing Consumer Mortgage Loans in Exceptional Circumstances Financial Consumer Agency of Canada

Book: “The Program”

- Part 1 – Building Your Down Payment

- Part 2 – Mortgage Payoff Strategies

- Part 3 – Building Wealth Through Real Estate