… Get out from under those ridiculous interest charges

Debt rarely shows up as one big bad decision. More often, it’s a slow buildup—credit cards used during a tight year, a car loan layered on top, maybe a line of credit that never quite goes back to zero. Before long, a noticeable chunk of your monthly income is going toward interest, not progress.

Refinancing to consolidate debt is one of the most powerful—and most misunderstood—tools Canadians have to regain control of affordability. When used properly, it can simplify cash flow, lower interest costs, and create breathing room. When used at the wrong time or without understanding the limits, it can do the opposite. This article is about helping you understand what refinancing for debt consolidation really is, when it makes sense, and how to use it strategically.

Topics Covered in This Guide

Why is debt consolidation increasing?

How to consolidate your debt through refinancing

When should you consolidate debt through refinancing

Why does refinancing require you to break your mortgage?

What are the limits of consolidating debt through refinancing?

Using the Debt Consolidation Calculator to consolidate debt

Why fees and amortization must be looked at together

A story: when consolidation made sense—and when it didn’t

What is debt consolidation

Debt consolidation is the process of combining multiple debts into a single loan or structure. Instead of juggling several payments—each with its own interest rate, due date, and minimum—you roll them into one.

When done through refinancing, unsecured debts like credit cards, car loans, or personal loans are replaced with secured mortgage debt, which typically carries a much lower interest rate. The goal isn’t just simplicity—it’s reducing the cost of interest and improving cash flow.

Why is debt consolidation increasing?

Debt consolidation has become more common for a few key reasons.

First, the cost of living has risen faster than incomes for many Canadians. Even disciplined households have leaned on credit to bridge gaps.

Second, higher interest rates have made unsecured debt especially painful. A balance that once felt manageable at 12% feels very different at 20% or more.

Third—and this matters—many homeowners have built equity over time. As property values increased and mortgage balances declined, refinancing became a viable way to restructure debt more efficiently.

In short, people aren’t consolidating because they’re reckless. They’re consolidating because the math changed.

How to consolidate your debt through refinancing

Refinancing means replacing your existing mortgage with a new one that’s larger than your current balance. The additional funds are used to pay off other debts.

In practice, it looks like this:

First, determine how much equity is available in your home using the Home Equity Access Calculator.

Second, you decide which debts you want to eliminate—credit cards, loans, lines of credit, or other obligations.

Third, those balances are rolled into a new mortgage at a lower interest rate and longer amortization.

The result is fewer payments, lower interest costs on those debts, and a clearer monthly picture.

When should you consolidate debt through refinancing

Timing is everything. Refinancing to consolidate debt tends to work best when:

- You’re at or near mortgage renewal

- Interest savings outweigh fees and penalties

- Cash flow relief is a priority

- You plan to stay in the property long enough to benefit

It’s less effective when penalties are high, equity is limited, or the consolidation simply stretches debt longer without addressing spending habits. The right time isn’t universal—it’s situational.

Why does refinancing require you to break your mortgage?

Refinancing mid-term usually means breaking your existing mortgage contract. That’s because you’re changing its core structure—balance, amortization, or lender.

Your lender priced your mortgage based on the original terms. When those terms change, a mortgage penalty often applies. This is where many people get tripped up. The interest savings from consolidation can look great on paper—until the penalty is factored in.

That’s why penalty awareness isn’t optional. It’s foundational.

What are the limits of consolidating debt through refinancing?

Refinancing isn’t unlimited. Lenders impose clear boundaries.

Most traditional refinances are capped at 80% of the home’s value, including all mortgage balances. Credit profile, income stability, and property type also matter.

However, 80% is not a hard and fast rule. If you have a rural property (no municipal services) you’ll find most lenders cap your refinance at 65% of your appraised home equity. Under some government programs refinancing can go up to 95% but not for debt consolidation. Some Heavy Alternative lenders will go 80% for a higher interest rate but still a fraction of what a credit card would charge.

There are also practical limits. Consolidating debt shouldn’t turn short-term spending into permanent debt without a plan. The goal is relief and structure—not just kicking the can down the road.

Understanding these limits upfront prevents disappointment later.

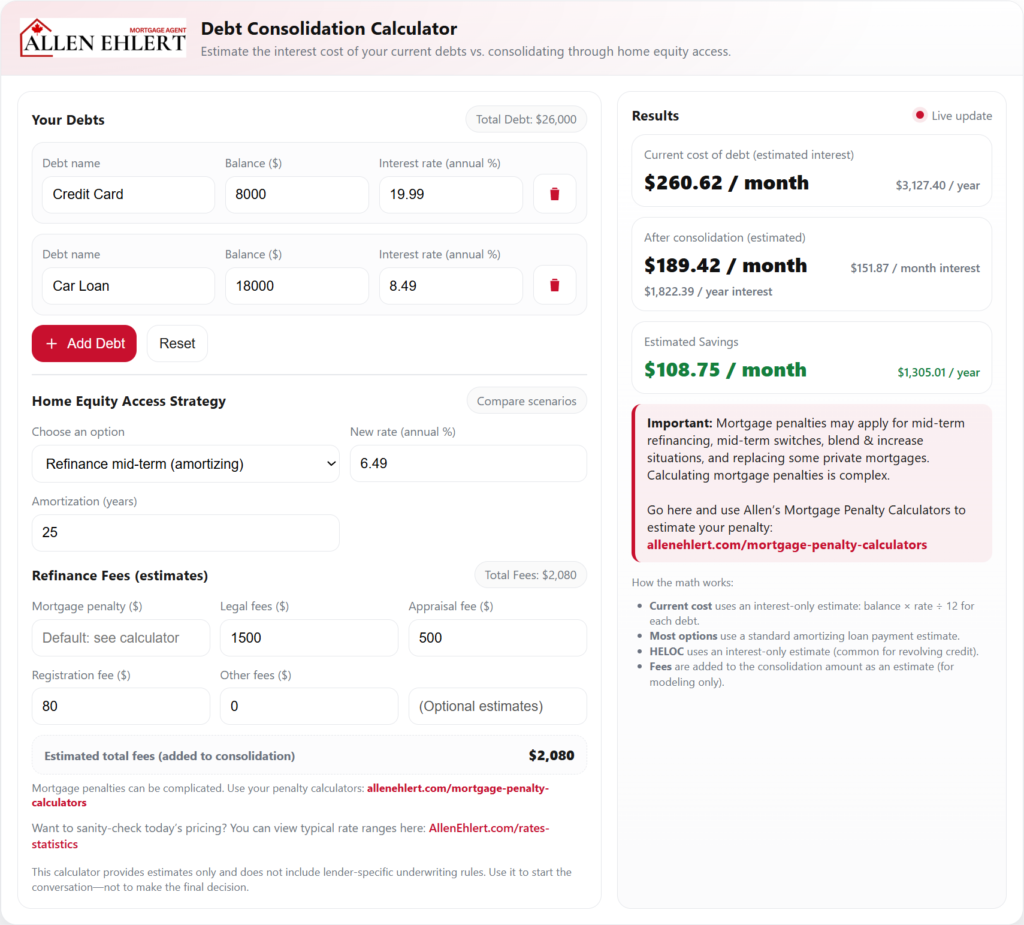

Using the Debt Consolidation Calculator to consolidate debt

Below is an expanded, drop-in section you can insert directly into your article under “Using the Debt Consolidation Calculator to Consolidate Debt.”

It keeps the same narrative, expert tone and goes deep on fees and 25-year amortization, which are the two areas most Canadians misunderstand.

Using the Debt Consolidation Calculator to consolidate debt

The real value of the Debt Consolidation Calculator isn’t that it spits out a number—it’s that it forces you to confront the full cost of restructuring debt. Rates matter, yes. But fees, penalties, and amortization choices often matter more than people realize.

Let’s walk through how to interpret what the calculator is showing you, starting with fees, then amortization.

Understanding the fees: the part most people underestimate

One of the biggest mistakes Canadians make when thinking about refinancing to consolidate debt is focusing only on the new interest rate. The calculator deliberately breaks out fees because fees are the friction in the system—they’re what separate a good idea from a bad one.

Here’s what each fee represents and why it matters.

Mortgage penalty

If you refinance mid-term, you’re changing the deal you originally signed. That almost always triggers a mortgage penalty. This could be:

- Three months’ interest

- An interest rate differential (IRD)

- Or, in some cases, a blended calculation

The calculator doesn’t guess your penalty—it prompts you to think about it and directs you to my mortgage penalty calculators for a reason: penalties can erase savings fast if they’re ignored.

Legal fees

Refinancing is a legal transaction. A lawyer (or notary, depending on province) has to discharge the old mortgage and register the new one. Legal fees are usually predictable, but they still matter because they’re either paid out-of-pocket or added to the mortgage balance.

Appraisal fee

Lenders need to confirm the property’s value when you refinance. Even if you’re confident in the value, the lender still needs their own validation. Appraisals are common, and while they’re a one-time cost, they directly affect the total amount you’re rolling into the mortgage.

Discharge and registration fees

When a mortgage is removed from title, there’s often a discharge fee. When a new mortgage is registered, there’s a registration fee. These are smaller line items, but the calculator includes them because real decisions are made on net outcomes, not rounded assumptions.

Other fees

This is the catch-all category for things that vary by file—title insurance, rush fees, administrative costs. The calculator doesn’t assume them away; it gives you space to model them.

Why this matters:

When you add fees to the consolidation, you’re not just paying them—you’re often financing them. That means they affect your interest cost over time, not just on day one.

Why the Debt Consolidation Calculator uses a 25-year amortization

The 25-year amortization isn’t accidental. It reflects how most refinances are structured in Canada and highlights the trade-off between cash flow relief and long-term cost.

Here’s what a longer amortization does—and doesn’t—do.

What a 25-year amortization does

- Lowers the monthly payment

- Improves short-term affordability

- Creates immediate cash flow relief

This is often exactly what someone consolidating debt needs. If high-interest payments are choking cash flow, the first priority is breathing room.

What a 25-year amortization does not do

- It does not magically eliminate debt faster

- It does not mean you’ll pay less interest over your lifetime

- It does not replace good financial habits

The calculator uses 25 years to show the structural impact of refinancing. You can always choose to make extra payments later. You can’t undo unaffordable payments today.

Why fees and amortization must be looked at together

This is where most online advice falls apart.

A refinance with a great rate but heavy fees might look attractive—until you spread those fees over 25 years. Conversely, a refinance with modest fees and a slightly higher rate might produce better real-world results.

The calculator forces these elements into the same frame:

- Debt balances

- Interest rates

- Fees

- Amortization

When you see them together, the decision becomes clearer—and calmer.

A quick example: how the calculator reframes the decision

Imagine two scenarios:

One option shows a lower rate, but once penalties and fees are added, the calculator shows Estimated Extra Cost.

Another option shows a slightly higher rate, but fewer fees and no penalty, resulting in Estimated Savings.

Without a calculator, most people chase the first option. With the calculator, they choose the second—and sleep better.

That’s not math. That’s insight.

For Financial Planners and Accountants

If you work with clients on cash flow, tax efficiency, or long-term planning, you already know this reality: debt is often the silent saboteur. It doesn’t always show up as a crisis, but it quietly undermines otherwise sound financial plans. That’s exactly where my Debt Consolidation Calculator is designed to support your work.

Let me explain how I see planners and accountants using it in practice.

Turning abstract debt advice into concrete numbers

You’ve likely told clients some version of, “We need to get this high-interest debt under control.” The challenge is that advice can feel abstract until the numbers are visible.

The calculator allows you to:

- Quantify the true interest cost of unsecured debt

- Show, in dollars, how credit cards and personal loans are eroding cash flow

- Shift the conversation from behaviour to structure

Instead of debating spending habits, you’re walking clients through what the debt is actually costing them every month and every year.

Bridging the gap between balance sheets and real cash flow

As planners and accountants, you live in financial statements, tax returns, and projections. Mortgages and consumer debt live in the client’s lived reality—monthly payments and stress levels.

This tool connects those worlds. It helps you demonstrate:

- Why a client who earns well still feels cash-constrained

- How interest expense limits saving, investing, and tax planning

- Why restructuring debt can be a prerequisite—not a distraction—from good planning

It lets you sequence advice properly: stabilize cash flow first, then optimize.

Reframing home equity as a planning lever—not a temptation

Home equity conversations can be uncomfortable. Used poorly, equity access looks like encouraging leverage. Used properly, it’s a risk-management and restructuring tool.

The calculator allows you to show clients:

- When using equity reduces overall financial risk

- How consolidating debt can lower default and stress risk

- Why timing (renewal vs mid-term) matters more than chasing rates

It keeps the conversation disciplined and professional, not emotional.

Making penalties and fees visible before they become mistakes

One of the biggest blind spots outside mortgage specialization is penalties. Clients often assume refinancing is frictionless.

The calculator forces those realities into the discussion:

- It flags when mortgage penalties may apply

- It incorporates legal, appraisal, and discharge costs

- It directs clients to penalty calculators instead of assumptions

That protects both your client and your professional credibility.

Supporting better tax and investment outcomes

From your perspective, interest expense is dead weight. Reducing it can:

- Free up RRSP, TFSA, or corporate investment capacity

- Improve debt-service ratios ahead of future borrowing

- Reduce reliance on high-interest, non-deductible debt

The calculator gives you a way to show how debt restructuring can support tax and investment strategies rather than compete with them.

Answering the question clients always ask: “Should we do this now?”

You hear it all the time.

By modeling:

- Refinancing mid-term versus at renewal

- Penalty versus no-penalty scenarios

- Different amortizations and fee structures

You can give grounded advice like:

“This doesn’t make sense today—but it probably will at renewal.”

That kind of clarity builds trust and reduces reactive decision-making.

Using a neutral, third-party visual tool

Debt is emotional. Clients can become defensive or overwhelmed quickly.

A calculator changes the dynamic. Instead of telling clients what they should do, you can say:

“Let’s look at what happens if we do this—and what happens if we don’t.”

That neutrality keeps conversations collaborative and productive.

Where I fit into your process

My goal isn’t to step on your role—it’s to complement it.

Once a strategy looks promising, I step in to:

- Validate lender feasibility

- Confirm penalties and fees

- Structure the mortgage correctly

- Ensure the consolidation aligns with the broader plan you’ve built

That way, your advice stays strategic, and the execution is handled correctly.

The bottom line

My Debt Consolidation Calculator gives you a practical way to bring mortgage realities into financial planning and accounting conversations—without having to become a mortgage expert yourself.

It turns debt from a vague concern into a structured, solvable problem.

And when advisors work from the same framework, clients win.

A story: when consolidation made sense—and when it didn’t

I once worked with a couple who wanted to refinance immediately to wipe out credit card debt. On the surface, the numbers looked promising. Once we added the mortgage penalty, the savings disappeared.

Instead of forcing the move, we planned ahead. We used the calculator to model the same consolidation at renewal. No penalty. Same debts. The outcome flipped from neutral to meaningfully positive.

Same goal. Different timing. Completely different result.

Allen’s Final Thoughts

Refinancing to consolidate debt isn’t about hiding problems—it’s about restructuring reality. When interest costs are draining cash flow, structure matters. Timing matters. And understanding the trade-offs matters most of all.

As a mortgage agent, my role is to help you see the full picture: penalties, limits, lender rules, and long-term impact. Whether refinancing now, waiting for renewal, or choosing a different strategy altogether, the goal is the same—stronger affordability and fewer surprises.

The tools and calculators start the conversation. I’m here to help you turn that information into a smart, confident plan.