… A Sustainability Planner to Stress‑Test Your Retirement Plan

You can look at a reverse mortgage and think, “Sweet—cash from my house, no payments, I stay put.” And honestly… that part is true. But here’s the twist: the real question isn’t whether you can get the money—it’s whether the plan holds together over 10, 15, or 25 years once interest compounds, life gets more expensive, and the house still needs constant upkeep.

That’s exactly why I built the Reverse Mortgage Sustainability Planner (also called the Reverse Mortgage Budgeting Planner on my site): to move the conversation beyond “How much can I borrow?” and into the far more useful question: “Is this financially sustainable for the long haul?”

Topics covered in this article:

Why a Reverse Mortgage Needs a Sustainability Test

What the Reverse Mortgage Budgeting Planner Models

Your Prep Work: Gather the Numbers

Running Your First Scenario in the Planner

Stress-Testing: Preparing for Trouble

How Advisors and Clients Put This Into Practice

Why a Reverse Mortgage Needs a Sustainability Test

A reverse mortgage is a loan secured against your home. You can borrow against your equity and you’re typically not required to make regular payments while you live in the home, but interest and fees are added to the balance—so what you owe tends to grow over time.

That’s not “good” or “bad.” It’s just math.

Here are the sustainability pressure points the planner is designed to reveal:

Interest compounding and rising balances. The Financial Consumer Agency of Canada explains it clearly: lenders add interest costs to the reverse mortgage balance, meaning the total amount you owe increases over time.

Ongoing homeowner obligations. A reverse mortgage doesn’t replace the real-world cost of owning a home. You still need to keep up with property taxes, insurance, and maintenance—requirements that show up in consumer regulator guidance and lender program descriptions.

Loan repayment triggers. Reverse mortgages are generally repaid when you sell, move out, the last borrower passes away, or if you default on terms (like not maintaining the home or staying current on required costs).

So the point of a sustainability test is simple:

You’re not just trying to “unlock equity.” You’re trying to avoid waking up ten years from now with a plan that quietly became brittle—especially if housing prices flatten, rates stay high, or your monthly cash flow gets squeezed.

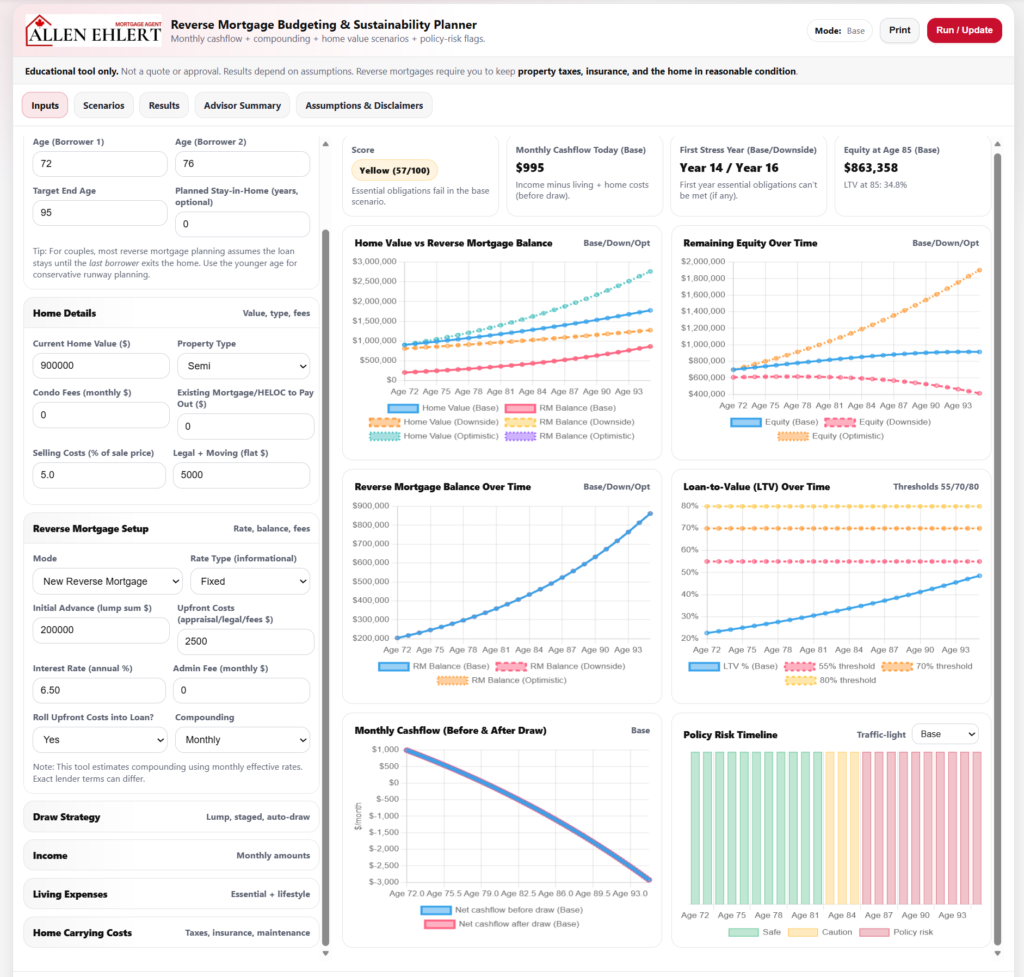

What the Reverse Mortgage Budgeting Planner Models

Most reverse mortgage tools answer one narrow question: How much can I get?

This planner answers the grown-up question: How does the whole strategy behave over time?

The Sustainability Planner integrates the pieces that actually drive long-term outcomes, including:

- Your income (like CPP, OAS, pensions, and investment income)

- Your living expenses

- Property taxes, insurance, utilities, and maintenance

- Reverse mortgage interest compounding

- Home appreciation (or depreciation)

- Draw strategies (lump sum, staged, or “cover the shortfall”)

- Downside stress scenarios

Then it models what happens month by month, so you can see the trajectory—not just a snapshot.

That matters because reverse mortgages aren’t “set it and forget it.” How you take the money (lump sum vs. installments) can materially change costs. For example, the Financial Consumer Agency of Canada notes that taking a full lump sum means paying interest on the full amount right away, and if you don’t use it immediately, it can be an expensive way to borrow.

So the planner isn’t trying to impress you with a big number. It’s trying to protect you from a plan that only works on a sunny-day spreadsheet.

Your Prep Work: Gather the Numbers

If you want the planner to give you a result you can trust, you’ve gotta feed it real inputs. Not perfect—just real.

Here’s what you want in front of you before you start clicking around:

Your income picture (net, not fantasy). Include predictable income streams and any portfolio withdrawals you actually plan to take. The planner is designed for the “fuller picture” approach—income + expenses + housing obligations all together.

Your non-negotiable monthly costs. Think: groceries, car, medications, subscriptions, grandkid gifts—whatever is truly part of your life. (No judgment. If hockey tickets are essential to your sanity, we can call them essential.)

Your home carrying costs. Property taxes, insurance, utilities, condo fees if applicable, and realistic maintenance. Regulators and lenders both emphasize that homeowners must continue paying required housing costs and keeping the home in good shape.

Your home value and mortgage balance. Reverse mortgages are commonly expressed as a percentage of appraised value. Government consumer guidance describes a typical “up to 55%” structure (though some programs can go higher).

Your timeline assumptions. This is underrated. Are you planning to stay in the home “forever”? Or do you think you’ll be there forever, but there’s a decent chance you move in 8–12 years? Reverse mortgages are often repaid when you sell, move out, or the last borrower passes away—so time horizon matters.

Quick gut-check: if you’re missing a number, don’t freeze. Use a conservative estimate, run it, then refine. Planning is iterative—You adjust as you go.

Running Your First Scenario in the Planner

This is the “first run” I recommend—because it keeps you from going down a rabbit hole.

First, enter your baseline reality: income, lifestyle expenses, and home carrying costs (taxes/insurance/utilities/maintenance). The planner is built specifically to integrate this full picture instead of isolating the reverse mortgage.

Second, enter your home and mortgage details (home value, any existing mortgage balance you’d want paid off, and your expected time horizon in the home). Reverse mortgage payoff timing matters because repayment is generally triggered by sale, moving out, or death of the last borrower.

Third, choose a draw strategy that matches your real-world goal: – If the goal is debt cleanup, you may model a larger upfront draw (but remember: lump sums can mean paying interest on funds you aren’t using yet).

– If the goal is monthly lifestyle support, model staged draws or periodic advances (consumer guidance notes many lenders offer different payout methods, including regular payments). [8]

Fourth, set your “Base” scenario assumptions (home growth and reverse mortgage interest). Be conservative. The planner exists to stand up to scrutiny, not to make you feel warm and fuzzy.

Fifth, run the model and look at the Results dashboard before you tinker. You want to understand what the baseline is doing.

Sixth, only after you understand baseline behaviour, add the “Downside” scenario (more on this below) and re-run.

Seventh, write down what changed and why. The planner gives you the visibility; the win is interpreting it and using it to make decisions.

Reading the Results Dashboard

Results dashboards can feel like cockpit controls if you’re not used to them. Here’s how you read it without getting overwhelmed.

Start with sustainability, not “maximum cash”

A reverse mortgage isn’t “free money.” Interest is added to the balance and compounds, which increases what’s owed over time.

Your first question in Results should be: Does this stabilize your monthly life—or just postpone a problem?

Watch the relationship between home value and loan balance

This is the heart of equity planning. Some lenders emphasize protections like “no negative equity” (never owing more than fair market value at sale) as a product feature.

But even if you never go “underwater,” a fast-growing balance can still shrink what’s left for future flexibility or your estate.

Look at cash flow before vs. after the reverse mortgage draw

This is where the planner earns its keep: it forces you to separate a structural cash flow issue (your income can’t support your costs), from a liquidity solution (using home equity to plug a predictable gap)

Consumer guidance notes that how funds are received (lump sum, partial upfront + later advances, or regular payments) can affect costs and outcomes.

Use the risk timeline mindset

Even if you don’t obsess over every chart, you want a clear sense of when things get tight. Reverse mortgages can default if required obligations aren’t met.

So a good Results read is basically:

“Do I stay comfortably above the line, or am I skating toward thin ice?”

Stress-Testing: Preparing for Trouble

Here’s the truth: base-case planning is where retirees get sucker‑punched.

The downside scenario isn’t there to scare you. It’s there to answer:

If things don’t go perfectly… do you still stay housed and stable?

A realistic downside stress test usually pushes on the big levers:

- Slower home appreciation (or a flat market for years)

- Higher interest rates / higher borrowing costs (reverse mortgage rates are typically higher than conventional mortgage or HELOC rates)

- Inflation in property taxes, insurance, and maintenance (the stuff you must keep paying)

Now here’s where it gets interesting for financial planners and investment professionals.

There’s research showing that including home equity as part of a retirement funding strategy—often accessed via a reverse mortgage credit line—can reduce the probability of “portfolio exhaustion,” especially when withdrawals are coordinated around down markets (drawing on home equity after negative portfolio performance instead of selling investments at a loss).

Is that automatically right for you? Not necessarily. But it’s exactly the kind of “what-if” that your downside planning is meant to reveal:

- If markets get ugly early in retirement, do you have a liquidity backstop?

- If housing goes sideways, do you still have enough equity runway?

- If rates stay higher, does the plan still behave?

You’re basically building a plan that can take a punch and stay standing.

How Advisors and Clients Put This Into Practice

This planner is a bridge tool—it helps mortgage strategy and financial planning stop living in separate silos.

A story that shows how this plays out in real life

Let’s say you, a financial planner (or advisor) are working with a couple—call them Dave and Marlene.

They’re both retired. Income is okay, but not amazing. Their house is worth a lot (welcome to Canada), and their monthly costs have crept up with taxes, insurance, and—because life happens—some health and support expenses.

They’re considering a reverse mortgage because they’re tired of squeezing the budget and don’t want to sell the home.

So you run the planner.

In the base scenario, a staged draw covers the monthly shortfall without draining their investment account. They feel relief—like they can breathe again.

Then you flip to the downside:

- Home growth is weaker

- Borrowing costs are higher

- The monthly gap widens

And boom—you see the real insight: the plan might still work, but only if they reserve enough cash flow to stay current on taxes, insurance, and maintenance, because those are non-negotiables tied to staying in good standing.

So Dave and Marlene don’t abandon the reverse mortgage idea. They refine it.

They decide to:

- Reduce discretionary spending slightly (tiny change, big impact)

- Structure draws to avoid taking too much too early (because lump sums can be expensive if unused)

- Keep an explicit “housing obligations buffer”, so they don’t accidentally default on the boring-but-deadly stuff

That’s what good planning feels like: less hype, more control.

How financial planners use this in practice

A planner can use the tool to sanity-check whether a reverse mortgage supports the retirement income plan without quietly creating a long-term leverage problem. That’s especially useful because many Canadians are “house rich, cash poor,” and home equity is a real part of the retirement conversation.

Common planner workflows look like:

- Testing whether home equity withdrawals can reduce investment drawdowns during poor markets (a theme in retirement research literature)

- Comparing reverse mortgage cash flow support vs. downsizing or HELOC strategies

- Translating “equity” into a sustainable spending plan that protects lifestyle and avoids nasty surprises later

How other professionals use this in practice

Accountants and tax-focused advisors often care about timing: when you draw funds, whether you’re selling assets, and how to sequence cash flow so you’re not triggering unnecessary taxes. A key baseline point is that money received as a loan isn’t taxable income.

Estate planners care about the estate impact: reverse mortgages can reduce remaining equity, and the loan plus accrued interest is repaid when the home is sold or from proceeds when the plan ends.

And for you as the client? The practical benefit is clarity: you’re seeing the trade-offs before you commit.

Allen’s Final Thoughts

A reverse mortgage isn’t just a borrowing decision—it’s a long-term sustainability decision. Interest compounds because it’s added to the balance, costs can be higher than traditional borrowing, and you still have to keep up with taxes, insurance, and maintenance to stay in good standing.

And that’s exactly why the Sustainability Planner exists: it combines your income, expenses, home carrying costs, interest compounding, and downside scenarios into one month-by-month view—so you can pressure-test reality, not best-case marketing.

Now, here’s where I come in. My job isn’t to shove you toward the biggest loan amount and call it a day. My job is to help you build the cleanest, safest strategy—whether that ends up being a reverse mortgage, a HELOC, downsizing, refinancing, or a hybrid plan.

When you’re ready, I can support you by:

- Interpreting your planner results

- Comparing lender options, including advance methods, legal requirements, and protections like no-negative-equity features

- Coordinating with your financial planner, accountant, and lawyer so everyone’s rowing in the same direction

- Helping you structure a draw strategy that matches your real goal—debt relief, monthly cash flow support, renovations, or building a contingency buffer.

Bottom line: you don’t have to figure out this maze alone. Bring me your numbers (even if they’re rough), run the planner, and we’ll turn it into a plan you can actually live with—confidently, calmly, and with your eyes wide open.