… A Strategic Look at LendHub’s Quick Equity-Based Loans

As an accountant or financial planner, you don’t get paid to react — you get paid to anticipate. You structure tax strategies, preserve capital, manage risk, and protect long-term wealth. But every now and then, a client calls with a short-term liquidity problem that doesn’t fit neatly into the long-range plan.

They don’t need a 25-year amortization.

They don’t want to break a 1.89% first mortgage.

They simply need capital — and they need it now.

That’s where LendHub’s Quick Equity-Based Loan program becomes a strategic tool rather than a last resort.

Below are the key areas I’ll explore:

The Strategic Role of Equity-Based Lending

How the Quick & Easy Structure Works

Understanding the Cost Crossover Point ($65K–$70K Explained)

Pricing, Rate Sensitivity & Total Cost Logic

Risk Controls and LTV Guidelines

Common Use Cases for Accountants and Financial Planners

Realtor Integration and Real-World Applications

Where This Product Fits — and Where It Doesn’t

The Strategic Role of Equity-Based Lending

You already know liquidity timing mismatches can destabilize otherwise sound financial planning.

Examples you’ve likely seen:

- CRA arrears threatening liens

- Capital gains payable before liquidity event closes

- Business receivables tied up

- Unexpected legal settlements

- Temporary cash flow compression

Traditional lending is slow. It requires full income documentation, appraisals, legal coordination, and underwriting layers.

LendHub’s Quick Equity program is different.

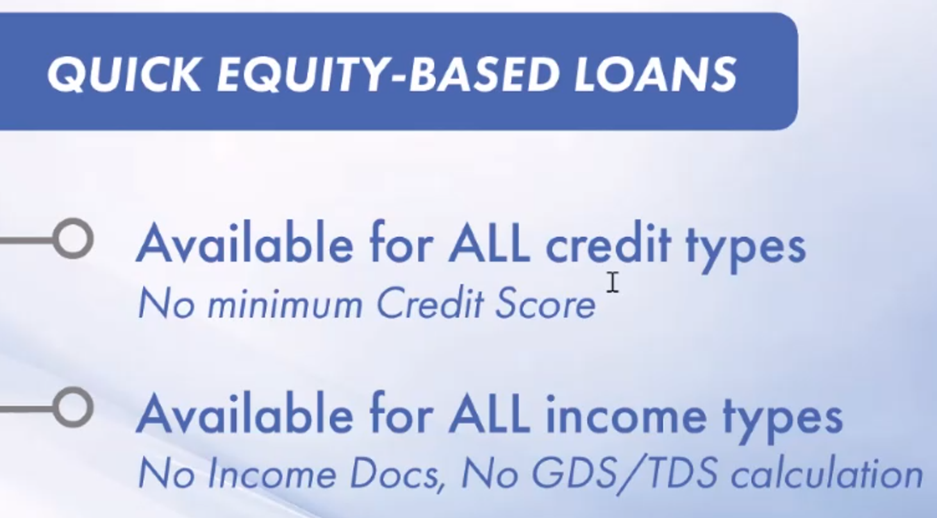

This is true equity-based lending:

- No GDS/TDS calculations

- No income documentation

- Decision driven primarily by LTV

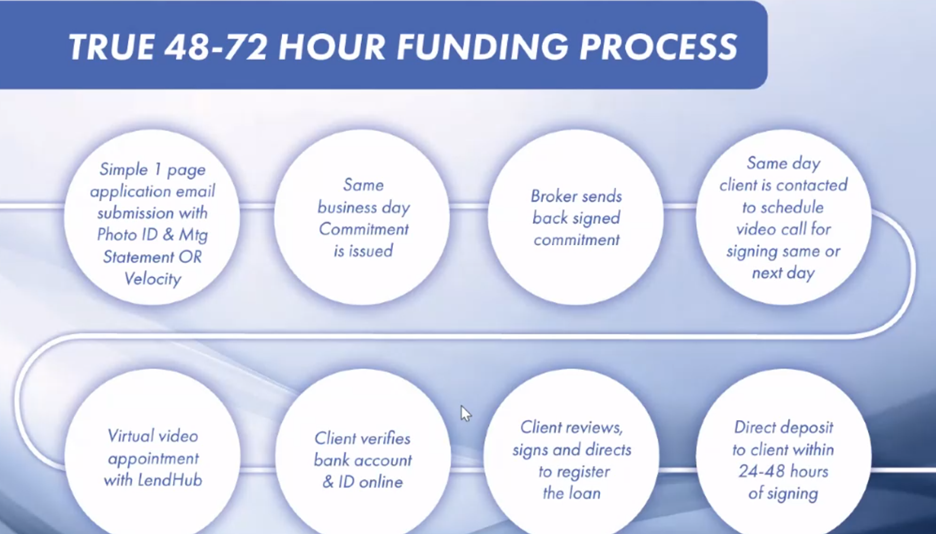

- Funding in approximately 48–72 hours

If the equity is there, capital can move quickly.

For you, that means solving short-term pressure without dismantling long-term architecture.

How the Quick & Easy Structure Works

Mechanically, this is a private mortgage product designed for speed.

Key structural features:

- Loan amounts up to approximately $100,000 net

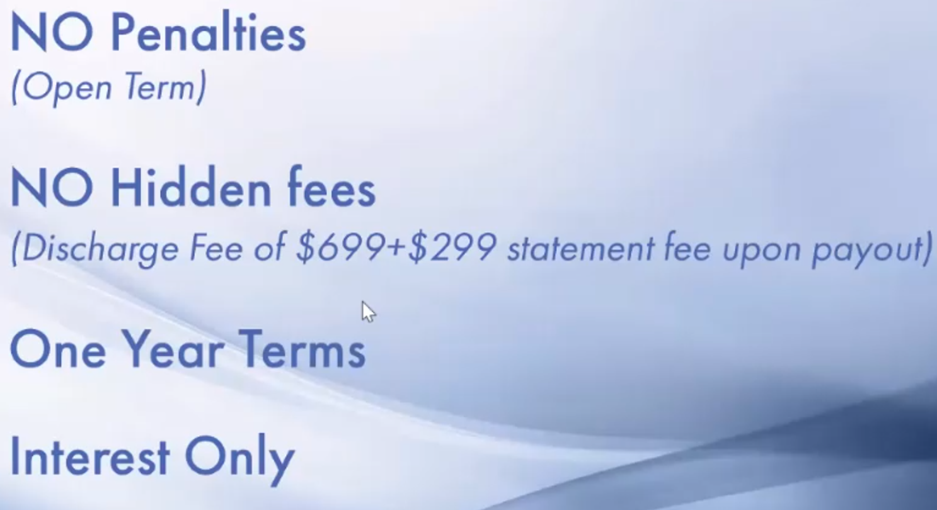

- Maximum gross advance around $115,000

- 12-month interest-only term

- Fully open (no prepayment penalties)

- No appraisal (uses AVMs)

- No legal process through external law firms

- No lender insurance requirement

Funds are deposited directly into the borrower’s account once documentation and identity verification are complete.

There is no traditional two-lawyer closing. No waiting on appraisal reports. No back-and-forth with title insurers.

It’s streamlined by design.

Understanding the Cost Crossover Point ($65K–$70K Explained)

Now let’s address the most important nuance for financial professionals — the cost crossover point.

LendHub’s Quick Equity structure charges:

- 10% total lender fee (6% lender / 4% brokerage referral)

- Flat admin fee (~$999 + HST)

- No legal fees

- No appraisal cost

Traditional private lending, by comparison, usually includes:

- Lender fee (often 2–3%, with a minimum)

- Broker fee (1–2%)

- Two lawyers

- Appraisal

- Registration costs

Here’s the key insight:

Legal and appraisal costs are largely fixed. They don’t shrink just because the loan is smaller.

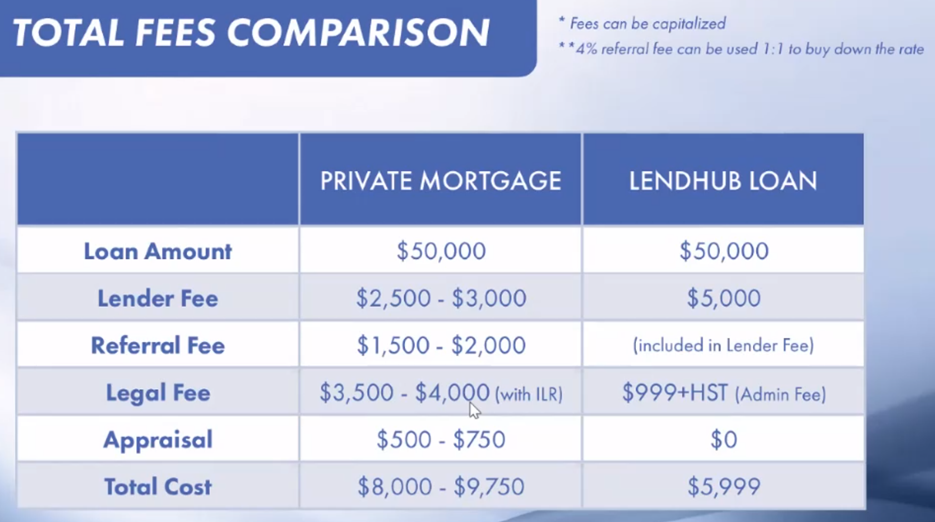

Example: $50,000 Loan

Traditional private:

- Lender fee: ~$2,500 minimum

- Broker fee: ~$1,500–$2,000

- Legal fees: ~$3,500–$4,000

- Appraisal: ~$600

Total cost: $8,000–$10,000

LendHub Quick Equity:

- 10% fee = $5,000

- Admin ≈ $1,000

- No legal, no appraisal

Total ≈ $6,000

At $50,000, LendHub is typically cheaper — and significantly faster.

Example: $70,000 Loan

Traditional private:

Still often around $8,500–$10,500 because many costs remain fixed.

LendHub Quick Equity:

- 10% = $7,000

- Admin ≈ $1,000

- Total ≈ $8,000

Now we reach parity.

Example: $100,000 Loan

LendHub Quick Equity:

- 10% = $10,000

- Admin ≈ $1,000

- Total ≈ $11,000

At this level, traditional private lending may sometimes become more competitive strictly on percentage cost — but it will be slower and more administratively intensive.

What “Up to $65K–$70K” Really Means

When I say the product is particularly attractive “up to roughly $65,000–$70,000,” I’m referring to this crossover point.

Below that range:

- LendHub is often cheaper in total cost.

- It is materially faster.

- It avoids transactional friction.

Above that range:

- Costs may be similar or slightly higher.

- The differentiator becomes speed and simplicity.

This is not a hard cutoff. It’s a practical economic crossover.

For smaller liquidity needs, traditional private lending can feel like using a sledgehammer to hang a picture frame.

This product is built for precision.

Pricing, Rate Sensitivity & Total Cost Logic

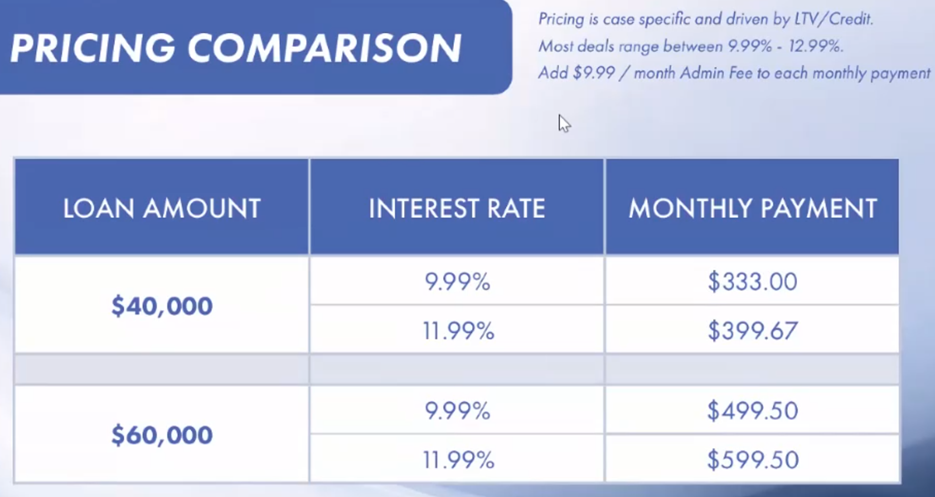

Rates typically range between:

- 9.99% and 12.99%, depending on LTV and credit

Clients will fixate on rate. You already know to shift the discussion toward total cost of borrowing and duration.

On a $50,000 loan:

The difference between 10% and 12% interest is roughly $1,000–$1,200 annually.

If the client saves $2,000–$3,000 in legal and appraisal costs — and exits in six months — the math becomes compelling.

This is not about rate shopping.

It’s about transactional efficiency.

Risk Controls and LTV Guidelines

Risk mitigation is handled through conservative LTV structure:

- Up to 70% province-wide

- Up to 75% in GTA/urban areas (with stronger credit)

- 65% for high-rise condos

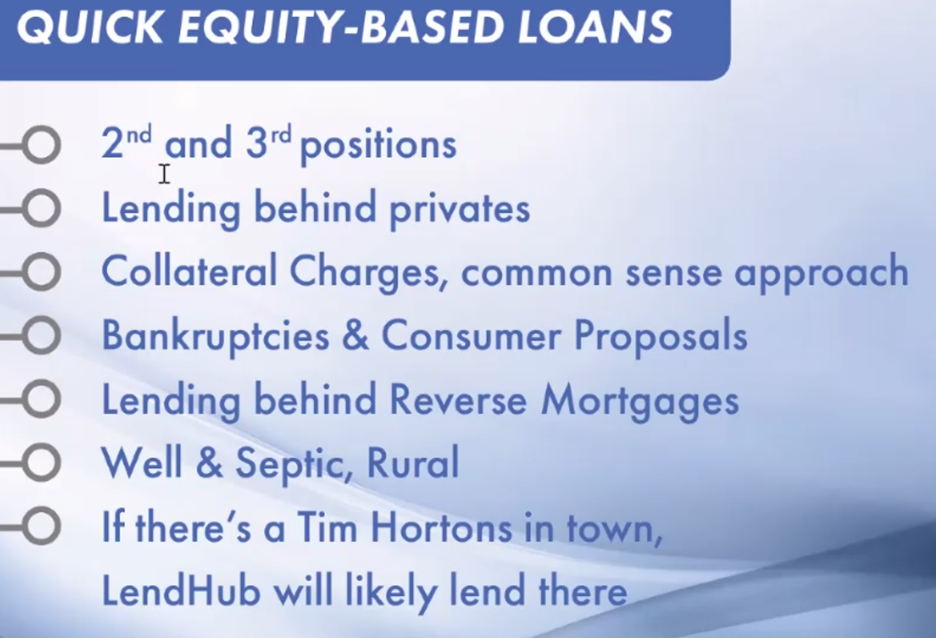

- Reduced LTV in second/third positions

They will lend:

- In second and third position

- Behind reverse mortgages

- On rural properties

- Across Ontario

Lower LTV = greater flexibility.

Equity cushion is the core protection mechanism.

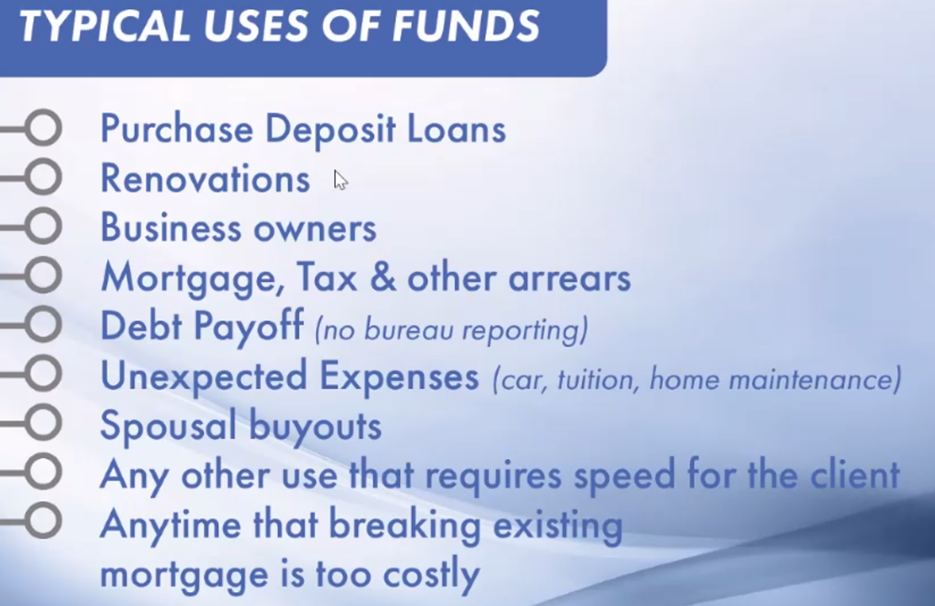

Common Use Cases for Accountants and Financial Planners

CRA Arrears

Property tax or CRA arrears can be paid directly. This prevents escalation into liens or forced collections.

Capital Gains Timing Gaps

Client owes tax but liquidity event hasn’t closed yet. Bridge, then exit.

Business Owner Cash Flow Compression

Inventory purchase, payroll timing, receivables delay. Solve the gap without refinancing the primary mortgage.

Preserving a Low First Mortgage Rate

Breaking a low-rate mortgage for a small cash need can trigger significant penalties. A short-term second avoids that disruption.

Credit Rehabilitation

Use private funds to eliminate unsecured debt. Improve beacon. Transition back to institutional financing.

Realtor Integration and Practical Applications

Realtors often face time-sensitive challenges:

- Deposit funding

- Pre-list renovations

- Unique rural properties

- Bridge scenarios

If a seller needs $30,000 to update a property before listing, waiting three to four weeks for a refinance can cost opportunity.

With this structure, funds can land within days. Renovations completed. Property sells at higher value. Loan repaid.

Strategic leverage, not reckless borrowing.

A Real-World Illustration

A self-employed contractor faced a receivable delay from a commercial client. Payroll was approaching. The accountant didn’t want to disrupt the client’s low first mortgage rate.

We structured a conservative LTV second under the Quick Equity program. Funds arrived within three days. Payroll was met. Receivable cleared 90 days later. Loan repaid early — no penalty.

Balance sheet preserved. Long-term structure intact.

That’s how this product should be used — as a temporary bridge, not permanent leverage.

Where This Product Fits — and Where It Doesn’t

This is not:

- A long-term financing solution

- A wealth accumulation strategy

- A substitute for structured institutional lending

It is:

- A short-term liquidity bridge

- A timing solution

- A capital access tool

- A transactional efficiency mechanism

Used properly, it protects the broader plan.

How to Implement Strategically

If you’re advising a client:

First, evaluate equity cushion and confirm conservative LTV.

Second, define a clear exit event (sale, refinance, receivable, maturity).

Third, assess total cost versus alternative structures.

Fourth, coordinate timing to minimize interest duration.

Fifth, integrate the decision into the broader financial plan.

Discipline is key.

Allen’s Final Thoughts

As accountants and financial planners, you’re building durable financial frameworks. Sometimes those frameworks need short-term liquidity reinforcement — not demolition.

LendHub’s Quick Equity product is not about stretching leverage. It’s about preserving stability when timing misaligns.

Below roughly $65,000–$70,000, the cost structure is often more efficient than traditional private lending. Above that range, speed and simplicity become the deciding factors.

My role is to help you determine:

- Whether the LTV is appropriate

- Whether the exit strategy is realistic

- Whether traditional private or institutional refinancing is better

- How this fits into the client’s broader capital structure

Think of me as your capital structure specialist. You manage tax efficiency and long-term wealth. I ensure liquidity tools are deployed intelligently.

When liquidity can’t wait, strategy matters more than speed alone.

And that’s where I can support you — thoughtfully, precisely, and with your client’s long-term interests front and center.