…. Market Rent Appraisals in Mortgages

More homebuyers today rely on rental income to qualify for mortgages. If you’re one of them, you’ll often need a market rent report or rent letter to “prove” that income to the lender.

So allow me to go over:

- When and why lenders ask for market rent evidence

- How to decide which report to order (flowchart included)

- Typical costs for each level of report

- What each report contains

I’ll also cover lender rules (e.g. signed lease vs projected rent, and legal vs illegal suites) and common delays – plus a pre-order checklist. Along the way I’ll give you a real-life example and practical tips so you can handle rent appraisals.

When & Why Market Rent Reports Matter

Decision Flowchart: Which Report to Order

When & Why Market Rent Reports Matter

Imagine your buyer is counting on renting out the basement suite (or a roommate’s rent) to qualify. Lenders know rental income can boost your GDS/TDS ratios, but they want proof – especially if no formal lease is in hand. You can use rental income in your mortgage application, but lenders require hard evidence. With a signed lease, many lenders will accept 50–100% of that rent in the income calc. But if no lease exists, expect a request for a market rent appraisal (or at least a rent letter) to verify the amount. For example, one bank states: “Market rent appraisal is required for all applications using rental income”. In short, if rental income matters, plan on documenting it.

Historically, market rent reports were rare, but since the 2018 stress-test (B-20) many borrowers have gotten creative about rental income. This means appraisers now often get standalone tasks: “What’s the market rent for this property?” instead of (or in addition to) doing a full value appraisal. If your mortgage application needs to include rent to qualify, be ready, most lenders (especially monolines and banks) may only allow a certain percentage of rent or require specific proof.

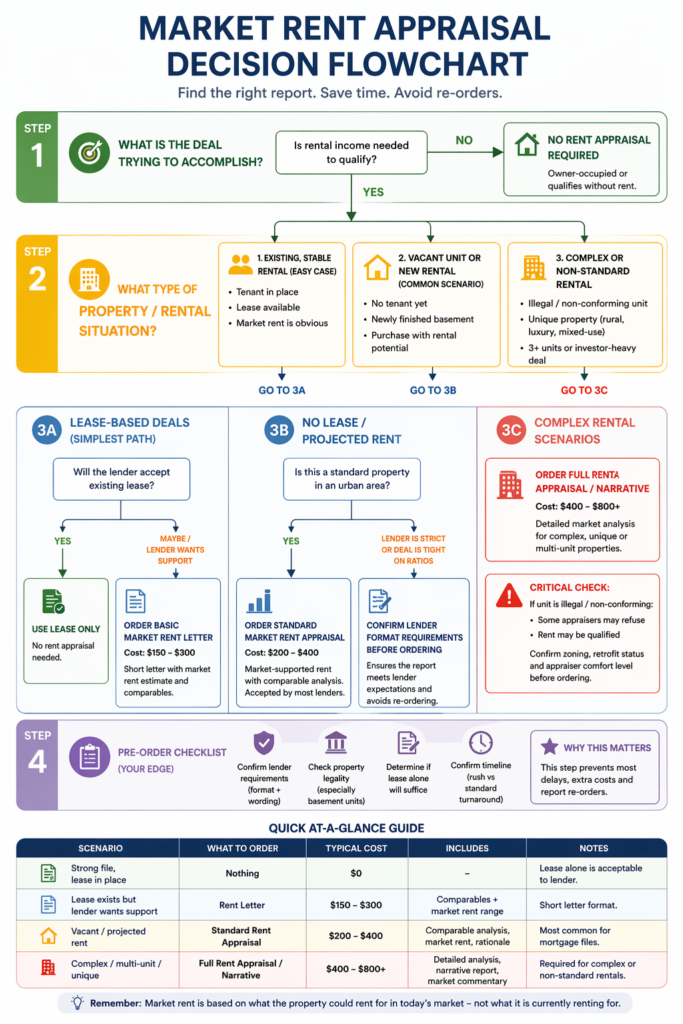

Decision Flowchart: Which Report to Order

Here’s my decision flowchart to pick the right path. It starts with “does your borrower need rental income?” and ends at “no report needed” or one of the report options. The arrows show how property type and lender rules steer you to no report, a simple rent letter, a standard appraisal, or a full narrative appraisal.

In words: if no rental income is needed (rent in “your back pocket” just for cash flow), then skip the report altogether. If income is needed, identify the situation:

- Tenant-occupied with lease: If there’s a formal lease and the lender will accept it, you may not need any extra report (just provide the signed lease and move on). If the lender still wants a report (for example, it counts only 50% of lease or wants an independent check), order a quick rent letter as a first step.

- No current tenant (vacant or planning a roommate): You’ll need an appraisal of the potential rent. For a typical home or condo, a standard rent appraisal is usually enough.

- Complex deal: If the property has multiple units (duplex/triplex) or unusual features, or the lender is very strict, go straight to a full narrative appraisal.

In practice, many deals end up needing at least a quick rent letter or a basic appraisal. If you skip this step and hope the lender takes 100% of projected rent, you risk a nasty surprise in underwriting. Always start the conversation by asking “Will we need to document rent?” – better to plan ahead than scramble later.

Real-Life Example

Meet Jen and Mike. They’re buying a 3-bedroom home with a basement suite. Jen’s brother is moving in, and they promise about $1,200/month rent (split 50/50 with the brother). Jen provides a sample lease (brother pays $600 per month to her). But the lender will only count 50% of that $1,200 since the unit is “non-market” family rental. Plus, the lease was handwritten.

Unfortunately, you need to deliver more proof. Since it’s tenant-occupied but the lender only offsets 50%, you decide to get a rent letter (see 3A) to justify the higher amount. You gather comps and tell an appraiser: 2-bedroom basement suites in the neighbourhood rent for $1,100–1,300. The appraiser (after a quick desktop check) returns a letter confirming “$1,200 ±$100” is fair market rent. You pass this to the underwriter. In the end, the lender agrees to count $600 (50%) of rent, plus they give a little more confidence. Jen and Mike close with no rent issues – all because the right report was ordered at the right time.

This story shows the flow: tenant in place → lease only covers part of lender requirement → rent letter supports the number. In other cases, the condo might be vacant, or a client might only plan to find a tenant. Then you’d have skipped the lease step and gone straight to an appraisal quote based on local listings (i.e. jump to the “vacant/new” branch in the flowchart).

Report Types & Pricing

Not all rent reports are created equal. You generally see four “levels”: nothing, a Rent Letter (Addendum), a Standard Rent Appraisal, or a Full Narrative Appraisal. Their costs and depth vary:

| Report Type | Ontario Cost Range | Typical Contents | Inspection & Photos | Market Commentary | Validity | When to Use / Lender Fit |

| No Report | $0 (none needed) | N/A | N/A | N/A | N/A | When rental income isn’t used. (Just qualifying on salary.) |

| Rent Letter / Addendum | $150–$300 (basic) | Short letter or simple form (e.g. Market Rent Addendum) with a few comparable rents and a rent estimate. | Desktop-only (no site visit); may include 1–2 exterior photos if any | Brief summary of rental market in area; may be very concise. | ~30–60 days or “as of date” on letter | When one unit or room (owner-occupied w/tenant), small gap to cover, and lender will accept form report. Good for quick deals or 50% rent offsets. |

| Standard Rent Appraisal | $200–$400 (mid) | Formal appraisal form or short report with detailed comparable rents (usually 3–5 comps), plus adjustments and analysis. | Possibly a drive-by inspection; often no interior visit (so no interior photos). Exterior photos of subject and comps typically included. | Includes some market trends or notes on supply/demand; supports final rent conclusion. | Typically valid ~60–90 days (depending on lender, some say 90 days). | When unit is vacant or lease not covering lender’s needs. Suitable for standard condos, houses with basement, condo rental offsets. |

| Full Narrative Appraisal | $400–$800+ (higher) | Comprehensive report. Includes full property description, high-level details, and an extensive rental comparables data set. May also cover value and rent if a combined appraisal. | Usually a full on-site inspection (interior photos, floorplan) plus photos of comps. | In-depth market discussion (supply/demand, legal issues, etc.); multiple scenarios (e.g. rent range vs best use). | Often valid 90 days or more (90–180 days). | Used for multi-unit properties, legal basement suites, or strict lenders. Also if you want highest credibility (e.g. CMHC insured deals or complicated deals). |

Note: All prices are estimates based on industry norms. For reference, one older mortgage industry source mentioned $50–$100 for a simple rent letter (prices have risen since), and full appraisals in Toronto commonly run $700–$1,500 for home value (not even counting rent). In practice, expect a typical single rent letter around a few hundred dollars, and a full narrative could approach $1,000 in busy markets.

Report Inclusions & Validity

Regardless of type, every market-rent report should follow appraisal standards (CUSPAP). That means comparables, analysis, and transparency of data. The appraiser will describe the property (bedrooms, bathrooms, legal status, any suite features) and then select similar rentals (“comps”) in the area. For example, factors like neighbourhood, condition, and unit size are matched as closely as possible. The appraiser then shows what those comparables rent for today and why your property’s rent fits in that range.

- Comparable Rents: Nearly all market rent reports list at least 2–5 similar properties with current rents. (No need for comparable sales prices – we’re focusing on rental market data only.)

- Inspection & Photos: In a standard appraisal, the appraiser usually drives by and takes some exterior shots, but may not require interior access (since rent is an “income” question more than condition). A full narrative often includes an interior inspection of the subject and photos to “prove” the suite exists.

- Market Commentary: A good report will mention local rental conditions: vacancy rates, demand for suites, and any quirks (like pet-friendly vs no-pet). Simpler rent letters might skip this, but narrative reports often discuss overall trends.

- Conclusion & Validity: The report concludes with a rent range or single rent value (e.g. “$1,200 ±$50 per month”). It should clearly date this conclusion (“as of May 2026”). Lenders typically require the report to be quite recent – most accept 60–90 days old[4]. Check each lender’s cutoff (e.g. Shinhan says 90 days). If the deal closes after the report expires, be prepared to order an update or a new letter.

Lease vs. Projected Rent

One common headache is whether the rent is documented (lease) or just planned. Here’s how “lease vs projected” usually works:

- Tenant & Lease: If the unit already has a tenant paying market rent, the signed lease is strongest evidence. Many lenders will accept 100% of that lease income (some only 50%, depending on bank) without any appraisal. Example: a client shows a 1-year lease at $1,500/mo – the lender can count this in your income. Still, some lenders (or deals) want an independent check to be sure the rent is truly market. In that case, a quick rent letter or addendum is often enough. Bottom line: always provide the lease first and see if the underwriter is happy.

- No Lease / New Rent: If the unit is currently vacant or no formal lease exists, never guess the rent. Lenders will almost certainly require a market rent appraisal. Even if the client says “I’ll try to get $1,300”, you need an objective opinion. Many brokers treat a signed lease with tenant as step 1, and only go to a rent appraisal if the lender says “we still need more”.

- Lender Policies Vary: Some lenders allow you to count a portion of projected rent if it’s been historically collected (e.g. you collected rent for the past 12 months). Others insist on only what’s contractual or appraised. Always check the details! For example, CMHC used to allow 50% offset for vacant suites but 100% for continuous income.

In short: lease = easiest; no lease = appraisal. If you skip getting the rent report when you needed it, you’ll end up revisiting the underwriting. Don’t leave rent as “wishful thinking”.

Legal vs. Illegal Suites

This is critical: Prime lenders won’t (legally can’t) count rent from an illegal suite (but many Alternative lenders will… for a higher interest rate).

Appraisers and banks assume any rental income used for qualification comes from a conforming unit. The appraisal associations have made this crystal-clear: no appraiser is allowed to provide a market-rent opinion for a non-conforming/illegal suite. In practical terms, if your basement or basement kitchen isn’t up to code or permitted by the municipality, the appraiser will refuse to include its rent – and the lender will refuse to count that income.

With Prime lenders (banks, credit unions, monoline lenders) and insured mortgages through institutions like Canada Mortgage and Housing Corporation, Sagen, and Canada Guaranty, the expectation is clear. The suite must be legal and conforming. In this environment, if the suite is not legal, it effectively does not exist from a lending perspective.

However, when you move into the Alternative and Private lending space, the approach becomes more flexible. Many Alternative and Private lenders will allow rental income from non-legal suites, but they do so with adjustments that reflect the increased risk. This often includes applying a rental income haircut, where only a portion of the rent—commonly between 50% and 80%—is used for qualification. In addition, these lenders typically impose lower loan-to-value limits, often capping financing around 75% to 80%, and place greater emphasis on the overall equity position, the borrower’s exit strategy, and the marketability of the property. In this context, the rental income is considered, but it is treated as higher-risk income rather than fully reliable income.

The appraisal process can become more nuanced in these situations. As a result, rental income may need to be supported through alternative means such as comparable rental listings, lease agreements, or detailed broker notes rather than relying solely on a formal rent appraisal conclusion.

This usually means the client will need more equity in the property, and the lender will not rely as heavily on that income when assessing qualification.

Ultimately, the key takeaway is that prime lending typically requires legal suites, alternative lending introduces flexibility, and private lending allows even more flexibility, often at a higher cost.

Turnaround & Common Pitfalls

When all this hits the fan, it’s usually one of a few avoidable issues:

- Incomplete Submissions: The top cause of delay is paperwork. Make sure the appraiser (and lender) have all the details: correct address, suite layout, number of bedrooms, basement features, etc. If the appraiser needs 3 months of condo fee receipts or a lease copy and you only gave 1 month, that stalls them. Double-check that the rental income numbers in the application match what you tell the appraiser. Consistency matters.

- Slow Borrower Docs: The appraiser may want bank statements, photos, or signed authorization from the borrower. If the client drags feet on sending these, the clock stops.

- Booking Appraisers: In high-demand markets or summer months, appraiser availability can be tight. Plan on 1–2 weeks for a standard rent report (though some are faster). A “rush” fee can speed things up if the client needs funds in a hurry.

- Payout Statement Delays: (This one isn’t rent-specific but often happens in switch refinances.) If you’re closing at a new lender, getting the existing lender’s payout statement on time is critical. A stale payout can push the closing date and upset the timing of your rent report validity. Always request the payout simultaneously and chase it up.

- Lender Last-Minute Changes: Occasionally, lenders ask for a higher-level report at the last minute. For example, an underwriter might say “Actually, we want a full narrative, not just the form” three days before closing. You can’t control this if you didn’t confirm up front. To avoid it: confirm exactly what the lender expects before you order. If in doubt, err on the side of a more complete report (especially if the deal is tight).

Pre-Order Checklist

Before I order an appraisal, I run through this list to avoid surprises:

- Check Rental Use Policy: Confirm with the lender how they count rental income. Can they use 100% of lease, or only 50%? Do they require a report if the unit is occupied?

- Verify Suite Legality: I’ll ask you if the suite is a legally permitted unit. If you’re not sure, I’ll strongly advise you to check with a contractor or municipality. If it’s illegal, I may need to change lenders or restructure the deal.

- Gather Basics: Compile property info (address, beds/baths including suite, basement finish details). Get any current lease or rent roll, even if verbal. I’ll check for any rules or condo by-laws affecting rental.

- Lender Format Requirements: Some lenders have their own rent report form (market rent addendum on the appraisal form). I’ll ask if a simple “Rent Letter” PDF is OK, or if it must be on a specific appraisal form. This avoids having to redo it.

- Compare Appraisers: Identify 2–3 local appraisers who do rent reports. Ask about their fees and turnaround. (We saw $150–$800 ranges.) See if one of our brokerage’s in-house partners offer quick rent letters.

- Budget & Pay: Ensure you are ready to pay for the appraisal (mandated by many lenders). I’ll explain that cost upfront. Clarify who orders it (broker or borrower) and how payment is arranged.

- Flag Urgency: If the closing date is tight, I’ll let the appraiser know the deadline. I’ll also notify the lender to expect the report, so they don’t treat it as a “mystery” back-ordered condition.

- Track and Follow Up: Once ordered, I’ll follow up. Confirm receipt. If the appraiser needs clarification, facilitate it. And make sure the final report gets to me and the underwriter promptly.

Running through these steps “to-do style” can save days.

Allen’s Final Thoughts

At the end of the day, rental income can be a game-changer in qualifying borrowers, but only if you handle it carefully. As a mortgage agent, my job is to make this process smooth for you. Here’s how I do it:

- Education: I explain early on that renting a suite isn’t just free money – it has rules. I spell out that we’ll need documentation (lease or appraisal), which helps manage everyone’s expectations.

- Lender Match: I pick the lender that fits the deal. Some banks are rent-friendly (they accept basement income easily) while others are more conservative. Knowing the lender matrix (and who requires full appraisals) is part of my value-add.

- Referrals & Coordination: I’ve got a list of qualified appraisers who understand market rent reports. I hand-pick one based on the deal’s needs. I handle the ordering and fees so my client can focus on moving, not chasing appraisers.

- Inspection Prep: I advise clients on making the rental space presentable (even if they’re not home). Good photos or a clean suite can make the report stronger.

- Follow-Through: I track that report like a hawk. If the appraiser emails questions, I loop the borrower in. Once it’s done, I deliver it to the lender and answer any clarifications. I also reconcile it with the mortgage figures (if the rent is slightly lower than promised, maybe renegotiate a rate or down payment).

- Communication: I use plain language. For example: “Your basement isn’t legal yet, so we won’t count that $1000 in rent – we should plan as if it’s just you two.” Or: “We’ll get a $200 rent letter to back up your numbers. It’s like a quick fact-check on the rent.” Keeping it jargon-free avoids client anxiety.

The flowchart, tables and story above give you the nuts and bolts of market rent appraisals. This should prevent last-minute surprises. Remember: getting the right rent report at the right time is often a no-brainer solution that saves loans from falling apart. If you need any help – whether it’s ordering the report, or interpreting the results – that’s what I’m here for.