Your present home doesn’t meet your current needs, and now it’s time to move to your next home. Bridge financing is an important part of that transition. It allows you to have possession of both houses for a short time, so you can move painlessly, and set up your new home the way you want it.

It’s a challenge to smoothly move from one home to another. There are a lot of things that can go wrong. Sometimes there’s a snag because the house insurance certificate was late because the broker was ill. Or maybe your moving truck pulls up to your new home only to discover the seller’s mover didn’t show up and the house is still full of all their stuff. When moving out of one home and into another on the same day, it is almost a miracle if things pull off without a hitch. Having bridge financing in place can ensure the sale of your home and the purchase of your next happens in a way that doesn’t blow up the sale. Bridge financing can give you the ‘wiggle room’ you need to keep your move a happy one.

With bridge financing, you can get your new home ready for you. Paint rooms, steam carpets, clean ducts, make adjustments, do small renovations …. whatever you need to make your new home your own before moving in. It is so much easier to get these things done without any furniture being in the way.

Bridge financing can even help you with that age-old decision, do I buy first, or do I sell first? In a world of tight housing supply and limited options, it is easier to sell than it is to buy the house you really want. Using bridge financing, you can focus on getting that difficult-to-find house you want, knowing you’ll have extra time to sell yours if you need it.

Bridge financing is a short-term loan designed to help you buy a new property before selling your current one. It’s a crucial tool for Canadian homeowners facing the buy-sell dilemma. By using your current home’s equity, you can secure a down payment for your new home.

In Canada’s fast-paced housing market, bridge loans are gaining traction. They usually last up to 120 days and are provided by big banks and lenders nationwide. This financing option is perfect for making quick moves in markets where time is of the essence.

Key Takeaways

- Bridge financing helps buy a new home before selling your current one

- Enables a smoothe real estate transaction by allowing some ‘wiggle’ room

- Enables you to prepare your new home while still living in your old home

- It’s a short-term loan lasting up to 120 days (longer with exceptions) in Canada

- Most lenders of all kinds (monoline lenders, MICs, Banks, etc.) offer bridge loans

- Uses equity from your current home for a new down payment

- Particularly useful in competitive real estate markets

Understanding Bridge Financing in Canadian Real Estate

Bridge financing is key in the Canadian real estate market. It offers temporary capital to homeowners during the gap between buying a new property and selling the old one. Let’s dive into bridge loans and their role in Canada.

What is bridge financing?

Bridge financing is a short-term loan that gives you quick funds when buying a new home before selling the current one. It’s like a financial bridge, letting you make a strong offer on your dream home without waiting for the sale of your current property.

How bridge loans work in the Canadian market

In Canada, bridge loans last from 30 to 120 days. Lenders typically offer this type of financing based on the equity in your current home and the expected proceeds from its sale.

Since your current home has equity, it can be used as collateral for the bridge loan. The lender will consider the value of your current home and the anticipated sale price when determining the amount you can borrow. This can provide the necessary funds to complete the purchase of your new home before your current one is sold.

It’s important to note that bridge financing often comes with higher interest rates and fees compared to traditional mortgages, as it is intended to be a short-term solution. Additionally, lenders may require a firm sale agreement for your current home before they approve the bridge loan, though some may be more flexible depending on your financial situation and the market conditions.

To proceed, you’ll need to work with a mortgage agent to discuss your specific situation, the terms of the bridge financing, and any other requirements.

Typical terms and conditions of bridge loans

Bridge loans in Canada have certain terms and conditions:

- Loan amounts of $500,000 are common but can be much higher (loan amount is price difference between the 2 homes)

- Usually has a minimum loan amount (e.g. $10,000)

- Mortgage must be present. Can’t do a bridge where both homes are purchased ‘free and clear’

- Interest rates are usually higher than traditional mortgages (Prime plus a premium)

- Repayment is typically due upon the sale of your current property

- Some lenders may require additional collateral

| Feature | Bridge Loan | Traditional Mortgage |

|---|---|---|

| Term Length | 15-120 days | 1-30 years |

| Interest Rate | Prime + 1.5% to 3% | fixed or variable |

| Approval Process | Faster | Longer |

| Purpose | Short-term financing | Long-term home ownership |

Knowing about bridge financing can help you make smart choices in the Canadian real estate market. Bridge loans and mezzanine financing are not as common as traditional mortgages. Yet, they offer valuable solutions for certain real estate situations.

The Advantages of Using Bridge Financing

Bridge financing is a powerful tool for Canadian homebuyers. It makes buying a home smoother and more competitive. This type of project finance helps you in the real estate market.

Unlocking equity from your current home

Bridge loans let you use your home’s equity before it sells. You can then make a down payment on a new property without waiting. Your lender gives you short-term funds to bridge the gap between homes.

Flexibility in home buying and selling timelines

Bridge financing gives you more time in your real estate deals. You don’t have to sell your current home before buying a new one. This is key in fast markets where timing is crucial.

Strengthening your offer in competitive markets

In competitive markets, bridge loans give you an advantage. You can make offers that don’t depend on selling your current home. This makes your offer as strong as cash offers, helping you get your dream home.

| Benefit | Impact |

|---|---|

| Quick approval | Faster than traditional mortgages |

| Access to equity | Immediate funds for down payment |

| Non-contingent offers | Stronger position in bidding wars |

| Extended move-in timeline | Time for renovations before occupancy |

Bridge financing can change the game in your home buying journey. It gives you the financial edge you need in the Canadian real estate market. Talk to your mortgage lender to see if it’s right for you.

Bridge Financing: Costs and Considerations

Bridge financing can be a big help when buying and selling homes in Canada. But, it’s important to know the costs. Bridge loans have higher interest rates than regular mortgages. You might pay rates that are Prime plus 2% to 3%.

Lenders charge a one-time setup fee, which can be $400 to $500. Legal fees can add another $200 to $300. For bigger loans or longer terms, there might be more costs.

| Cost Type | Typical Range |

|---|---|

| Interest Rate | Prime + 2% to 5% |

| Setup Fee | $250 – $500 |

| Legal Fees (if applicable) | $200 – $300 |

Think about the need to sell your current home fast. If you don’t, you might end up paying two mortgages at once. This could be tough on your finances if not managed well.

Before choosing bridge financing, think about the costs versus the benefits. It’s smart to talk to a financial advisor. They can help you see if this option fits your plans for buying and selling homes.

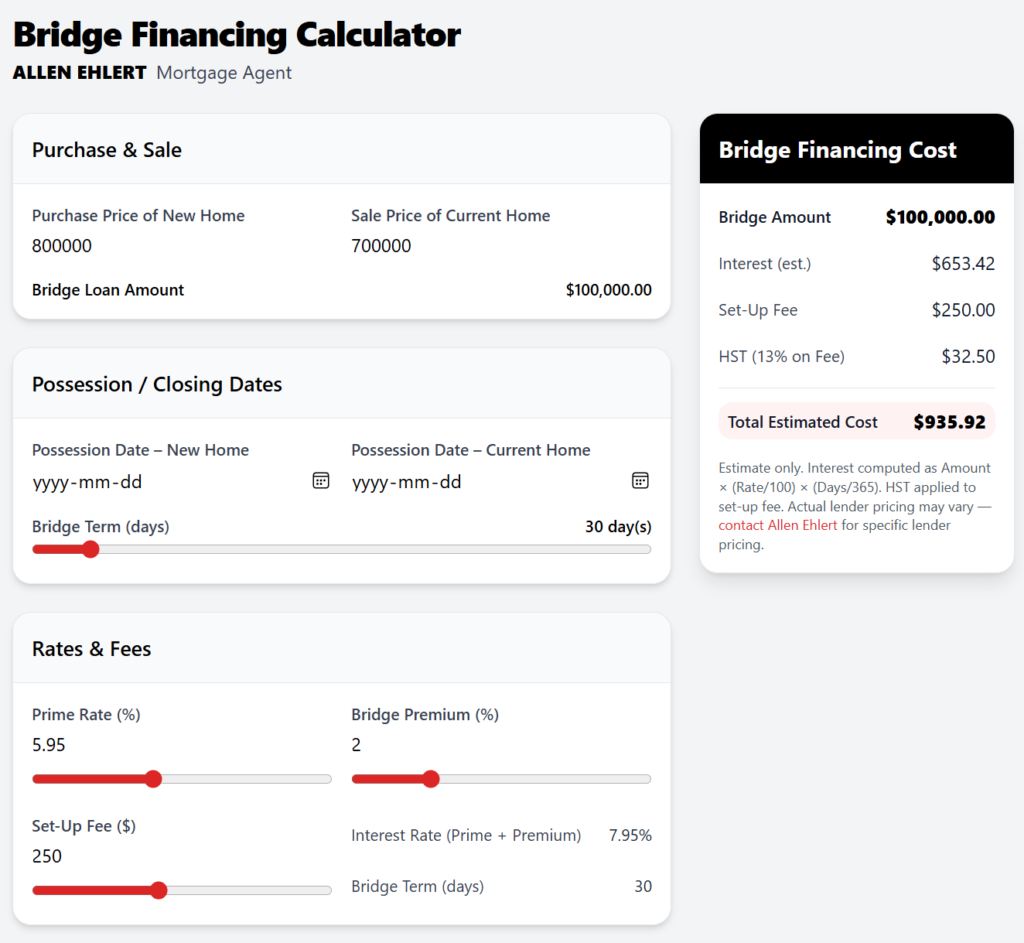

Bridge Financing: Example

In Canada, let’s look how you calculate a bridge loan where you are buying one house for 900,000, taking possession October 1 and selling a house for $800,000 leaving possession November 1 where prime rate is 7%

To calculate a bridge loan in Canada, you need to consider the amount needed to bridge the gap between the purchase of the new house and the sale of the current house, along with the interest rate and the duration of the loan.

Here are the steps to calculate the bridge loan:

1. Determine the Amount of the Bridge Loan: The bridge loan amount is the difference between the purchase price of the new home and the expected sale price of the current home.

Bridge Loan Amount = Purchase Price of New Home – Sale Price of Current Home

For our scenario:

Bridge Loan Amount = $900,000 – $800,000 = $100,000

2. Determine the Duration of the Bridge Loan: The duration of the bridge loan is the time between the possession date of the new home and the possession date of the current home.

Duration = Possession Date of Current Home – Possession Date of New Home

For our scenario:

Duration = November 1 – October 1 = 31 days

3. Calculate the Interest on the Bridge Loan: The interest is calculated based on the prime rate and the duration of the loan. The formula for the interest on the bridge loan is:

Interest = Bridge Loan Amount X ( Prime Rate / 100) X ( Duration in days / 365 )

For our scenario:

Prime Rate = 7%

Interest = $100,000 X ( 7 / 100) X ( 31 days / 365)

Interest (approx.) = $594.25

So, the bridge loan amount is $100,000 and the interest for the 31-day period costs approximately $594.25.

Qualifying for Bridge Financing in Canada

Getting bridge financing in Canada means meeting certain criteria. Your credit score is very important in the application process. Lenders look at your financial health and the value of your current property to decide if you’re eligible.

Eligibility Requirements for Borrowers

To get bridge financing, you need a good credit score, usually over 700. They also check your debt-to-income ratio. A lower ratio means you’re more likely to get approved. The value of your current home is also crucial. Most lenders want a lot of equity before they give you the loan.

Documentation Needed for Application

Applying for bridge financing means you’ll need to provide some documents:

- Firm sale agreement for your current property

- Purchase agreement for your new home

- Proof of income (pay stubs, tax returns)

- Bank statements

- Mortgage statements

Lenders Offering Bridge Financing Options

Most lenders offer bridge financing. Here are some current offerings (subject to change and borrower qualifications):

| Lender | Max Loan Amount | Interest Rate | Term Length |

|---|---|---|---|

| TD Bank | $250,000 | Prime + 4% | Up to 120 days |

| Merix | $200,000 | Prime + 2% | Up to 90 days |

| Scotiabank | $300,000 | Prime + 5% | Up to 90 days |

| Strive | $250,000 | Prime + 5% | Up to 120 days |

Most lenders apply loan fee (approximately $250 – $500 depending on the lender) to the interest charge.

Presently, the most common interest charge is the Prime rate of the lender plus 2%.

Remember, terms and conditions can change. It’s smart to look around and compare offers from different lenders to find the best bridge financing for you.

Conclusion: Navigating Your Move with Confidence

Bridge financing is a strong tool for Canadian homeowners facing property changes. It helps you in the competitive real estate market. It lets you buy your dream home while selling your current one.

Bridge loans offer flexibility that changes the game in your move. They make buying and selling easier, especially in fast markets. This financial help is key for quick decisions.

Planning is key when making financial choices. Think about the costs and risks versus the benefits. See how bridge financing fits into your financial plan. This way, you make choices that match your long-term goals in the Canadian real estate market.

A successful move is more than just changing homes. It’s about making smart financial moves for the future. With the right bridge financing, you can move with confidence. This turns a stressful process into a smooth and rewarding one.

FAQ

What is bridge financing?

Bridge financing is a short-term loan. It helps homeowners buy a new property before selling the old one. It uses the equity in the current home for a down payment on the new property.

How do bridge loans work in Canada?

In Canada, bridge financing is a short-term loan. It gives homeowners cash to buy a new home before selling the current one. It covers 90 days to 12 months. Lenders need a firm sale agreement for the current property.

What are the typical terms and conditions of bridge loans?

Bridge loans have higher interest rates than regular mortgages, usually Prime + 2% to 3%. Loan amounts of $500,000 are common for 120 days. Terms and conditions vary by lender.

What are the advantages of using bridge financing?

Bridge financing has many benefits for Canadian homebuyers. It lets homeowners use their current home’s equity for a down payment. This flexibility helps buyers make strong offers in competitive markets. It also gives time to improve the new home before moving in.

What are the costs and considerations of bridge financing?

Bridge loans in Canada have higher interest rates than regular mortgages, often Prime + 2% to 3%. There are also one-time fees of $400-$500 and legal fees of $200-$300. For loans over $200,000 or longer than 120 days, lenders might put a lien on the property, adding more legal costs.

What are the eligibility requirements for borrowers seeking bridge financing?

To get bridge financing in Canada, borrowers usually need a good credit score (650) and a low debt-to-income ratio.

What documentation is needed for a bridge financing application?

You’ll need a firm sale agreement for your current property and a purchase agreement for the new home.

Which lenders offer bridge financing options in Canada?

Major Canadian banks like TD, CIBC, Scotiabank, RBC, and BMO provide bridge financing. Some lenders might offer bridge loans without a firm sale agreement. However, this usually means higher rates and fees from B-lenders or private lenders.