Bankruptcy is a legal proceeding under the Bankruptcy and Insolvency Act (BIA) intended to relieve individuals or businesses who cannot pay their debts by legally discharging eligible debts. It provides protection against creditors, allowing you to rebuild your financial future.

Who Declares Bankruptcy in Canada?

Decision to Declare Bankruptcy

Who Declares Bankruptcy in Canada?

The typical individual who files for bankruptcy in Canada tends to share several common demographic and economic characteristics. While bankruptcy affects people across diverse backgrounds, the Office of the Superintendent of Bankruptcy (OSB) regularly provides statistical profiles highlighting trends among bankrupt individuals.

Age: The most common age group filing bankruptcy is typically between 35 to 50 years old. This group represents individuals facing peak financial responsibilities, such as mortgages, childcare, educational expenses, and aging parents.

Gender: Bankruptcy filings are fairly evenly split between men and women, but slightly more men historically file for bankruptcy in Canada. However, recent trends show an increasing proportion of female filers due to changing economic circumstances.

Marital and Family Status: Many individuals who file bankruptcy are married or separated, frequently dealing with financial pressures stemming from family changes like divorce, separation, or single parenthood.

Occupation and Employment: Individuals declaring bankruptcy often hold mid-level jobs or work in fields such as retail, hospitality, construction, transportation, or administrative positions. They are typically employees earning modest to average salaries rather than high-income professionals or business executives.

A significant number are self-employed or operate small businesses that have experienced economic setbacks or market disruptions.

Debt Level and Type: Typical bankrupt individuals carry substantial unsecured debt, averaging between $40,000 and $70,000, predominantly in credit card debt, personal lines of credit, payday loans, and income tax arrears.

Most lack significant assets or hold assets below provincial exemption limits, providing little protection from creditors.

Reasons for Bankruptcy: Common reasons cited for bankruptcy include:

- Job loss or income reduction

- Divorce or family breakdown

- Medical emergencies or disability

- Poor financial management or high-interest debt accumulation

- Failure of small businesses or economic downturns affecting income

Geographic Distribution: Bankruptcy filings are most common in urban or suburban areas with higher living costs, such as Toronto, Vancouver, Montreal, and Calgary. However, smaller cities and rural areas can also see significant bankruptcy filings due to localized economic difficulties.

Decision to Declare Bankruptcy

A Licensed Insolvency Trustee (LIT) would typically recommend or decide to pursue bankruptcy in Canada when it’s clearly the most appropriate and effective solution for addressing overwhelming financial hardship. Bankruptcy is chosen when alternatives, such as consumer proposals or debt management plans, are not viable or suitable.

- Specific circumstances could include:

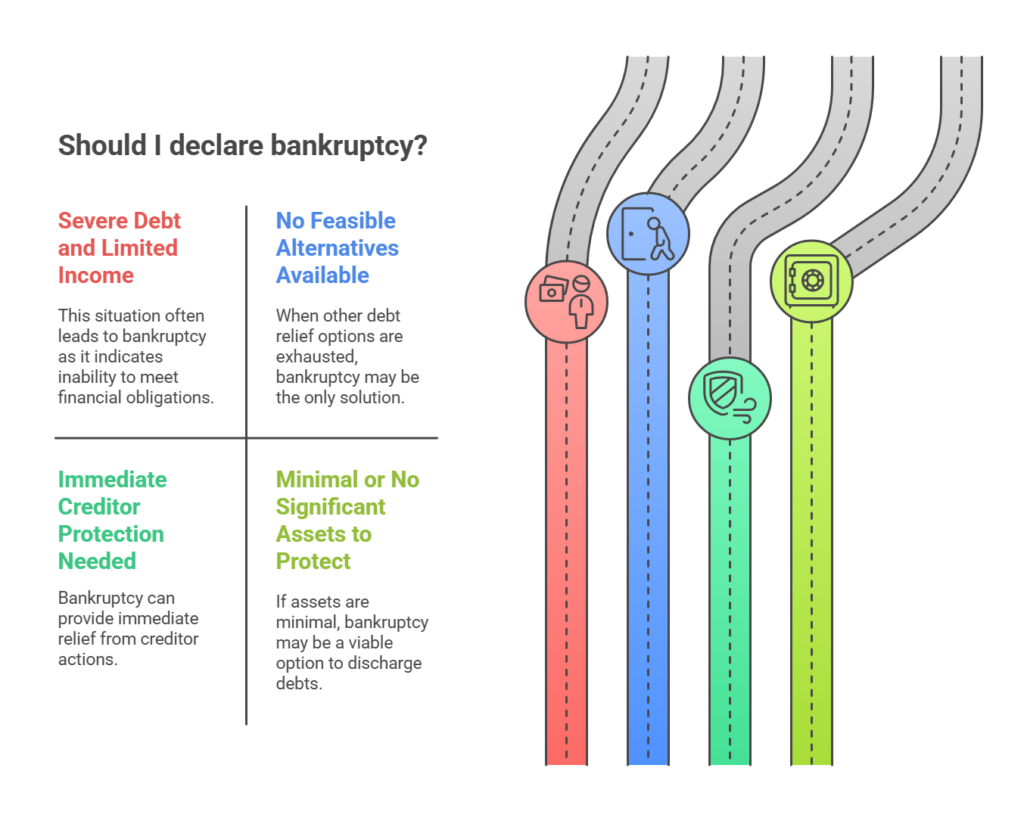

- Severe Debt and Limited Income

- No Feasible Alternatives Available

- Need for Immediate Creditor Protection

- Minimal or No Significant Assets to Protect

- High Debt-to-Income Ratio

- Severe Financial Distress and Mental Health Impact

- You Have Substantial Debts Eligible for Discharge

- Previous Debt-Relief Attempts Failed

Severe Debt and Limited Income

Bankruptcy is recommended when your total debts significantly exceed your income, making it impossible to repay even a reduced portion through a consumer proposal or other structured repayment options. If your income barely covers essential living expenses, bankruptcy often becomes the most practical solution.

No Feasible Alternatives Available

If the LIT determines that you cannot realistically afford a consumer proposal (which requires manageable monthly payments) or a debt management plan (which requires full debt repayment), bankruptcy is recommended. This typically occurs when creditors are unlikely to accept a consumer proposal due to insufficient repayment capacity.

Need for Immediate Creditor Protection

When facing severe creditor actions, such as wage garnishments, bank account seizures, legal judgments, or intense collection pressures, a LIT may recommend bankruptcy because filing provides immediate and strong legal protection, called a stay of proceedings.

Minimal or No Significant Assets to Protect

Bankruptcy may be recommended if you have few assets, or if your assets fall below provincial exemption limits, meaning you’d likely lose little or nothing by filing for bankruptcy. With minimal assets to protect, bankruptcy becomes less impactful compared to other alternatives.

High Debt-to-Income Ratio

If your debts are so high relative to your income that a consumer proposal repayment amount would not be approved by creditors, bankruptcy becomes the best available option. This scenario commonly occurs when unsecured debts (credit cards, payday loans, lines of credit) vastly outweigh your disposable income.

Severe Financial Distress and Mental Health Impact

In situations where debt significantly impacts your mental and emotional health, causing severe stress or anxiety, the LIT may recommend bankruptcy. Bankruptcy quickly relieves overwhelming financial pressures, allowing you to stabilize emotionally, mentally, and financially.

You Have Substantial Debts Eligible for Discharge

An LIT will recommend bankruptcy if your debts primarily consist of dischargeable unsecured debts, such as credit cards, unsecured loans, lines of credit, payday loans, and income tax arrears. Bankruptcy can legally discharge these debts after the bankruptcy process, offering a true fresh start.

Previous Debt-Relief Attempts Failed

If you’ve already unsuccessfully attempted informal debt settlement, debt consolidation, or credit counselling without improvement, bankruptcy may be the best remaining option to achieve real and lasting financial relief.

A Licensed Insolvency Trustee recommends bankruptcy when it clearly represents the best practical solution given your specific financial circumstances. While impactful, bankruptcy provides comprehensive debt relief, strong legal protection, and a clear path to financial stability and recovery.

Other Debt Relief Solutions

In Canada, besides bankruptcy, there are several effective debt-relief options available to individuals struggling with overwhelming financial burdens. Each option addresses unique financial situations, providing clear paths to financial recovery.

- Consumer Proposal

- Debt Management Plan (DMP)

- Debt Consolidation Loan

- Debt Settlement (Informal Settlement)

- Credit Counselling

- Budgeting and Financial Planning

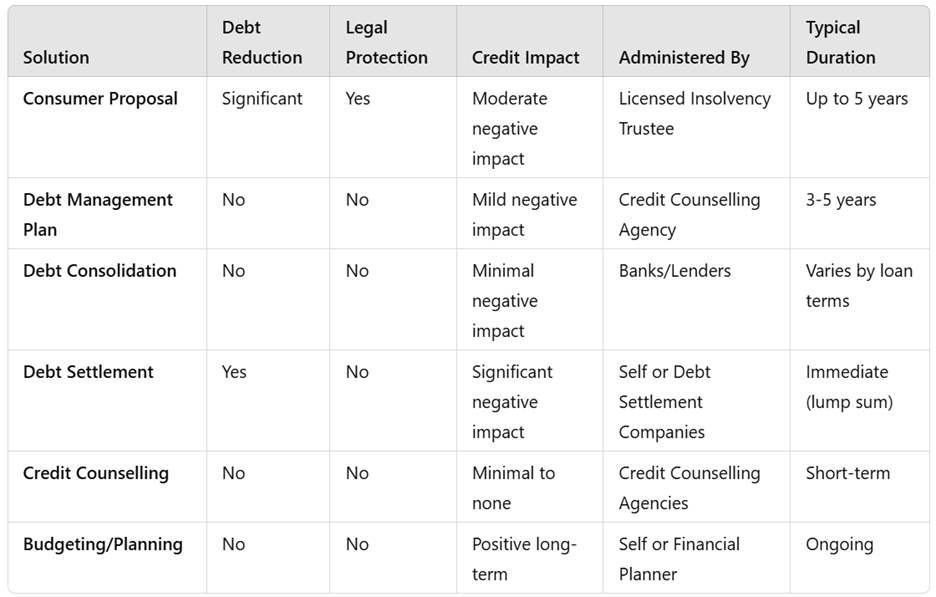

Consumer Proposal

A consumer proposal is a legally binding agreement between you and your creditors that allows you to pay back a reduced portion of your debts over a structured period (up to five years).

Key Features:

- Significant debt reduction (often 30% to 50% of original debts).

- Immediate legal protection from creditor actions.

- Managed exclusively by a Licensed Insolvency Trustee (LIT).

- Suitable if you have steady income and some ability to repay debts.

- Less severe impact on credit rating compared to bankruptcy.

Debt Management Plan (DMP)

A debt management plan involves consolidating multiple unsecured debts into one affordable monthly payment, typically facilitated by a non-profit credit counselling agency.

Key Features:

- Full repayment of debts but usually with reduced or eliminated interest.

- Informal creditor cooperation (no legal protections).

- Monthly payments based on affordability.

- Less negative credit impact compared to bankruptcy or consumer proposal.

- Financial education and budgeting support provided by credit counselling.

Debt Consolidation Loan

A debt consolidation loan involves taking out a single new loan (often at lower interest rates) to repay multiple high-interest debts, consolidating them into one manageable monthly payment.

Key Features:

- Simplifies debt repayment into one monthly installment.

- Potentially lowers interest rates and monthly payments.

- Maintains and can even improve credit rating if managed responsibly.

- Typically requires good credit or sufficient collateral.

- Does not involve creditor negotiation or debt reduction

Debt Settlement (Informal Settlement)

Debt settlement involves negotiating informally with individual creditors to repay a reduced amount of your outstanding debt, usually as a lump-sum payment.

Key Features:

- Negotiated lump-sum repayments at significantly reduced amounts.

- No guaranteed creditor acceptance.

- No legal protection from creditors during negotiation.

- Can negatively impact credit score significantly.

- Suitable if you have available funds to settle immediately.

Credit Counselling

Credit counselling offers professional financial guidance, budgeting advice, and personalized plans to manage your finances and repay debts effectively.

Key Features:

- Personalized budgeting and debt-management strategies.

- Often includes financial literacy and money-management education.

- Can lead to enrollment in debt management plans.

- Limited direct creditor negotiation; primarily advisory role.

Budgeting and Financial Planning

Improving your personal budgeting and financial planning practices can sometimes resolve debt issues without formal agreements or legal intervention.

Key Features:

- Ideal for less severe debt situations.

- Focused on disciplined spending, expense management, and savings.

- No impact on credit rating (positive long-term financial behavior).

- Does not reduce debts but helps prevent future debt accumulation.

Summary

Bankruptcy and Your Mortgage

Securing a mortgage after bankruptcy is challenging but not impossible. Most mainstream lenders consider applicants who’ve declared bankruptcy as higher-risk borrowers, often resulting in stricter conditions and higher interest rates.

While some lenders will pay out current consumer proposals, CRA taxes, and spousal buyouts, they will not pay out bankruptcy discharges.

Note: Some lenders will not lend to people who have been bankrupt or had consumer proposals previously.

Waiting Period

Most traditional lenders, such as banks, typically require at least two years following the discharge of a bankruptcy before considering a mortgage application. There are alternative lenders who will consider clients who are discharged from bankruptcy for a minimum of 12 months with re-established credit.

Alternative lenders or private mortgage lenders might be more flexible but usually offer higher interest rates and fees due to perceived higher risk.

Requirements Post-Bankruptcy

To qualify for a mortgage post-bankruptcy, lenders typically expect to see:

- A stable income and employment history

- Consistent rebuilding of credit (secured credit cards, personal loans)

- Evidence of improved financial management (regular payments, reduced debt load, healthy budgeting practices)

- A sizeable down payment (often 20% or more) to offset lender risk

Summary

Bankruptcy is a legal process under Canada’s Bankruptcy and Insolvency Act designed to provide relief to individuals or businesses unable to repay their debts. It offers immediate protection from creditors and a structured way to discharge eligible debts, enabling individuals to rebuild their financial stability.

Bankruptcy is typically recommended by a Licensed Insolvency Trustee (LIT) when other options, like consumer proposals or debt management plans, are not suitable. Circumstances leading to bankruptcy include severe debt with limited income, an immediate need for creditor protection, minimal assets to protect, a high debt-to-income ratio, significant mental and emotional distress due to debt, substantial debts eligible for discharge, or previous unsuccessful debt-relief efforts.

Alternative debt relief solutions in Canada include consumer proposals, debt management plans, debt consolidation loans, informal debt settlement, credit counselling, and personal budgeting and financial planning. Each option caters to specific financial situations, ranging from structured debt reduction to informal negotiation and education-focused approaches.

Securing a mortgage after bankruptcy is challenging but achievable. Traditional lenders typically require at least two years post-bankruptcy discharge, whereas alternative lenders may offer more flexibility with shorter waiting periods but higher interest rates. To qualify for a mortgage post-bankruptcy, lenders look for stable income, re-established credit, improved financial management practices, and a sizeable down payment to mitigate risk.