Sarah, age 37, lives in Ottawa, Ontario, and works as a retail manager earning $48,000 annually ($4,000 monthly gross income). She is a single mother with two young children, renting an apartment at $1,800 per month. Her financial situation has worsened significantly over the past two years.

How Sarah Fell Into Financial Hardship

When Should Bankruptcy Be Considered?

Why Bankruptcy Makes Sense for Sarah

Sarah’s Path Forward After Bankruptcy

How Sarah Fell Into Financial Hardship

Sarah previously managed her finances well, maintaining minimal debt. However, several unexpected life events led to mounting debt:

- Job Loss and Income Reduction: Sarah lost her previous job due to store closure. She was unemployed for five months, exhausting her savings and relying heavily on credit cards and a personal line of credit to pay essential expenses like rent, groceries, and utilities.

- Medical Expenses: Her younger child developed a serious medical condition requiring ongoing therapies and medications not fully covered by her employer’s limited insurance plan, leading to additional debt accumulation.

- High-Interest Debt: With credit card balances rapidly growing, Sarah resorted to payday loans to cover monthly bills, causing her debt levels to escalate dramatically.

Current Financial Snapshot

| Debt Type | Balance Outstanding | Monthly Minimum Payment |

| Credit Card #1 (19.99% interest) | $9,500 | $285 |

| Credit Card #2 (22.99% interest) | $6,700 | $201 |

| Personal Line of Credit (10%) | $12,000 | $250 |

| Payday Loans (avg. 390% APR) | $3,000 | $600 (bi-weekly rollover fees) |

| Income Tax Arrears | $4,500 | n/a (CRA demands full repayment) |

| Student Loan (over 10 years old) | $7,000 | $125 |

| Total Debt | $42,700 | $1,461 monthly (minimum) |

Income & Expenses:

- Monthly Net Income (after taxes/deductions): $3,200

- Total Monthly Living Expenses: Rent ($1,800), groceries and household expenses ($700), utilities ($200), childcare ($400), transportation ($250) = $3,350 total monthly expenses.

Sarah’s monthly obligations ($1,461 debt payments + $3,350 living expenses = $4,811) exceed her monthly net income ($3,200), creating a monthly shortfall of $1,611.

Financial Consequences Faced by Sarah:

- Her debts continue to grow rapidly due to compounded interest, penalties, and fees.

- Debt collectors regularly call and threaten legal action, garnishment of wages, and property seizures.

- Anxiety and stress levels have severely impacted her mental health and family life.

Evaluating Sarah’s Options

Sarah has three options available to her:

- Debt Consolidation Loan

- Credit Counselling/Debt Management Plan

- Consumer Proposal

Debt Consolidation Loan

Sarah was declined for a debt consolidation loan due to high debt-to-income ratio and damaged credit score (550).

Credit Counselling/Debt Management Plan

Sarah sought advice from a credit counsellor but was unable to afford the proposed payments due to insufficient disposable income.

Consumer Proposal

Sarah considered a consumer proposal, but after consulting a Licensed Insolvency Trustee (LIT), realized her disposable income was insufficient to offer creditors a viable repayment proposal that they would likely accept.

Given that alternatives were not practical or financially feasible, bankruptcy emerged as the most reasonable choice for Sarah.

What is Bankruptcy?

Bankruptcy is a legal proceeding under the Bankruptcy and Insolvency Act (BIA) intended to relieve individuals or businesses who cannot pay their debts by legally discharging eligible debts. It provides protection against creditors, allowing you to rebuild your financial future.

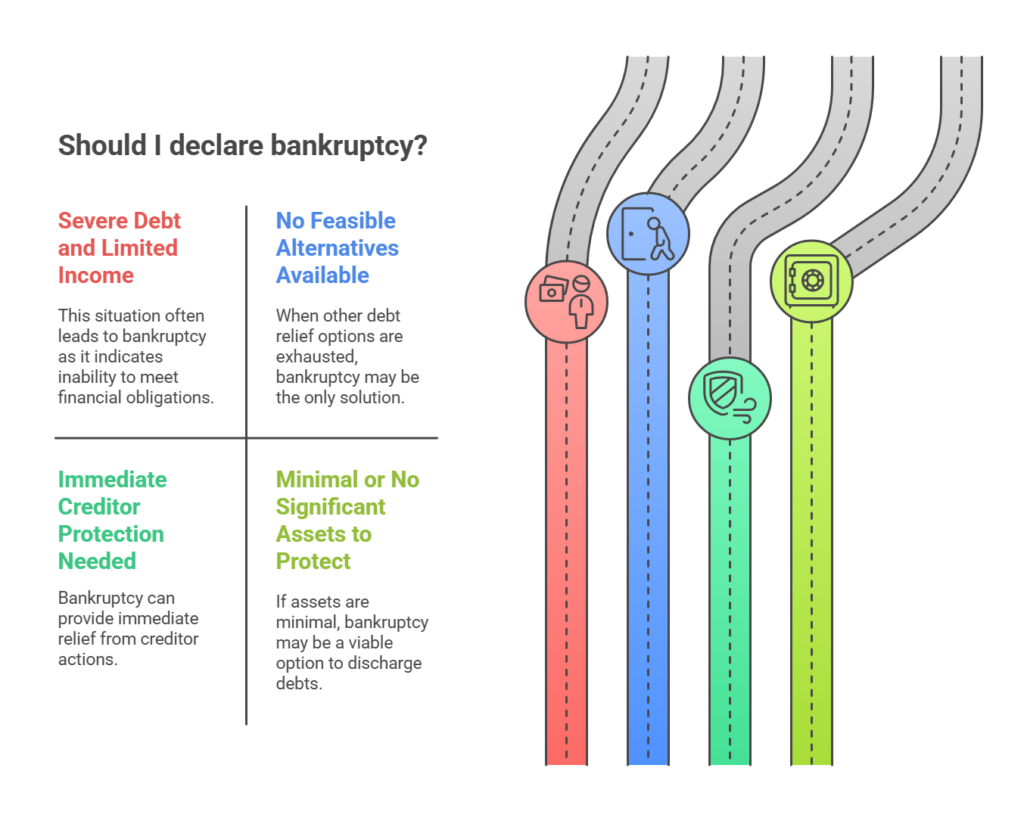

When Should Bankruptcy Be Considered?

Bankruptcy is considered when:

- You have unmanageable debts, significantly exceeding your ability to pay.

- You’re consistently unable to meet monthly obligations.

- Creditors are taking or threatening legal actions.

- Other debt-relief measures, such as consolidation, consumer proposals, or informal negotiation with creditors, have proven ineffective.

Why Bankruptcy Makes Sense for Sarah

Bankruptcy makes sense for Sarah for the following reasons:

- Immediate relief through a stay of proceedings, halting creditor calls, wage garnishments, and collection activities.

- Eligible debts (credit cards, payday loans, line of credit, income tax arrears, and older student loan) would be eliminated upon discharge.

- Her exempt assets (furniture, clothing, modest vehicle valued below provincial exemption limits, RRSP savings excluding recent contributions) remain protected.

- Monthly payments in bankruptcy (surplus income payments) will likely be modest, affordable, and substantially lower than her current obligations.

- Bankruptcy includes financial counselling sessions, providing Sarah valuable budgeting and financial management skills to avoid future debt problems.

- After approximately 9 to 21 months (first bankruptcy scenario), Sarah will be discharged, giving her the fresh financial start she desperately needs.

Sarah’s Path Forward After Bankruptcy

After discharge, Sarah can start to rebuild her credit by responsibly managing secured credit cards or loans.

Her reduced financial strain after bankruptcy significantly improves Sarah’s mental well-being, family stability, and long-term financial outlook.

Bankruptcy, while impactful on her credit rating, provides Sarah a structured, legally protected process to responsibly clear debts she otherwise cannot manage.

Summary

For Sarah, bankruptcy isn’t a failure—it’s a strategic, professionally guided decision enabling her to regain financial stability and begin building a secure financial future for herself and her children. This detailed scenario illustrates a realistic situation in which bankruptcy in Canada serves as the most responsible and effective solution for someone overwhelmed by debt.