I often hear the same question from clients: “What really happens if I go over my credit limit?” The truth is, going over your credit limit can feel like a small mistake in the moment—but it can have lasting effects on your financial health, especially your credit score. In today’s economic climate, with affordability stretched thin, many Canadians find themselves leaning on credit more than ever. But understanding what happens when you cross that invisible line is key to staying in control.

What Is Your Credit Limit—and Why Does It Matter?

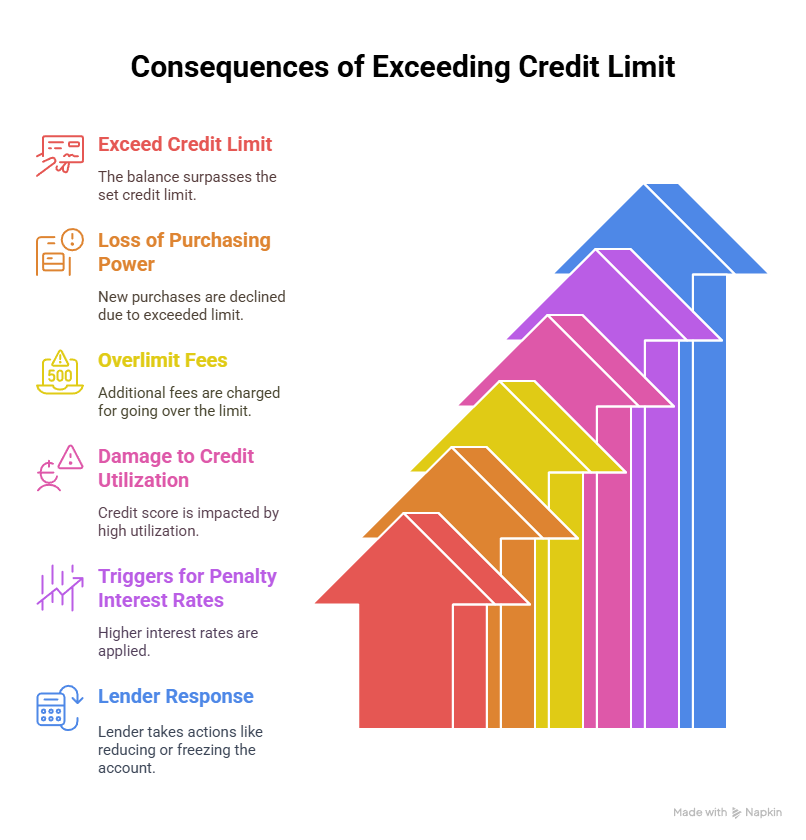

What Happens When You Go Over the Limit?

What to Do If You’ve Gone Over Your Limit

How to Prevent It from Happening Again

What Is Your Credit Limit—and Why Does It Matter?

Your credit limit is the maximum amount your credit card issuer has approved you to borrow at any given time. That number is based on your credit history, income, debt levels, and overall financial profile. Think of it as a trust line: staying within it suggests you’re managing your credit well. Exceeding it raises red flags—not only with your lender but also with credit scoring agencies.

What Happens When You Go Over the Limit?

Going over your limit means that your outstanding balance—whether through purchases, interest charges, or fees—has surpassed the threshold your lender set. For example, if your card has a $10,000 limit and you accumulate $10,200 in charges and interest, you are now over the limit. Here’s what that can trigger:

Loss of Purchasing Power

Most credit cards will automatically decline new purchases once your balance exceeds your limit. This can be inconvenient, especially in an emergency, or embarrassing at the checkout.

Overlimit Fees

Many credit card providers charge an overlimit fee, typically between $25 and $50. This fee is added to your balance, increasing your debt and making it harder to get back below your limit.

Damage to Your Credit Utilization Ratio

Your credit utilization—the percentage of your available credit that you’re using—is one of the most important factors in your credit score. It accounts for about 30% of your total score.

- Ideally, you should keep your utilization below 30% of your limit.

- Over 50% starts to raise concerns with lenders.

- Exceeding 100% utilization, as you do when you go over your limit, is seen as a serious risk factor.

High utilization signals that you may be financially overextended, even if you’re making minimum payments on time. This can cause a significant drop in your credit score—sometimes as much as 50 to 100 points, depending on your overall profile.

Triggers for Penalty Interest Rates

Going over your limit, especially more than once, can lead your lender to apply a higher penalty interest rate on your balance. This makes it even harder to pay off your debt and can turn a short-term slip into a long-term struggle.

Lender Response and Restrictions

Some lenders may take additional actions:

- Reduce your overall credit limit

- Freeze your account temporarily

- Close your account entirely

These actions reduce your available credit, which in turn worsens your credit utilization ratio and can further hurt your score.

Additional Credit Score Risks

Going over your limit doesn’t just affect the card in question. It can:

- Lower your overall credit score, impacting your ability to qualify for a mortgage, loan, or even a rental.

- Lead to reductions in credit limits on your other cards if other lenders view your profile as risky.

- Stay on your credit report for months, even if you bring the balance back under the limit quickly.

What to Do If You’ve Gone Over Your Limit

Don’t panic. The most important thing is to act quickly:

- Stop using the card immediately to prevent further penalties.

- Make a payment right away to bring the balance back under your limit.

- Contact your card issuer to explain the situation—they may waive the fee, especially if it’s your first time.

- Review your budget and spending habits to prevent a repeat.

How to Prevent It from Happening Again

Here are a few best practices to avoid exceeding your limit in the future:

- Set up automatic balance alerts through your banking app.

- Monitor your balance weekly or even daily if you’re close to your limit.

- Make multiple payments per month to keep your balance in check.

- Request a credit limit increase before you need it, not after.

- Keep your credit utilization below 30% to maintain a healthy credit profile.

Summary

Exceeding your credit limit isn’t a financial catastrophe, but it is a warning sign. It’s a moment that calls for a pause, a plan, and a little perspective. Whether it happened because of an unexpected expense, an oversight, or a tough month, the most important thing is how you respond. With the right actions and awareness, you can regain control of your credit and move forward with confidence.