Articles

10 Big Benefits of Going Variable

Variable Mortgages. If you’ve ever surfed—or even watched someone surf—you know it’s all about balance. You don’t fight the wave; you ride it. That’s exactly what it feels like to hold a variable-rate mortgage. Sure, the water can get choppy, but if you’ve got good footing, it can take you further, faster, and often cheaper than the safer route.

Canadian Land Transfer Tax Calculator

Land Transfer Tax Calculator: Buying a home in Canada is a thrilling adventure — whether it’s a downtown condo, a family home in the suburbs, or a cabin near the lake. But between deposits, inspections, and closing paperwork, there’s one cost that often catches buyers off guard: the Land Transfer Tax (LTT).

Home Carrying Cost Calculators

… Understanding Carrying Costs: The Unsung Hero of Smart Homebuying When most people think about buying a home, they focus on one number—the price tag. But seasoned buyers, realtors, and mortgage professionals know that the real story lies beneath the surface. The...

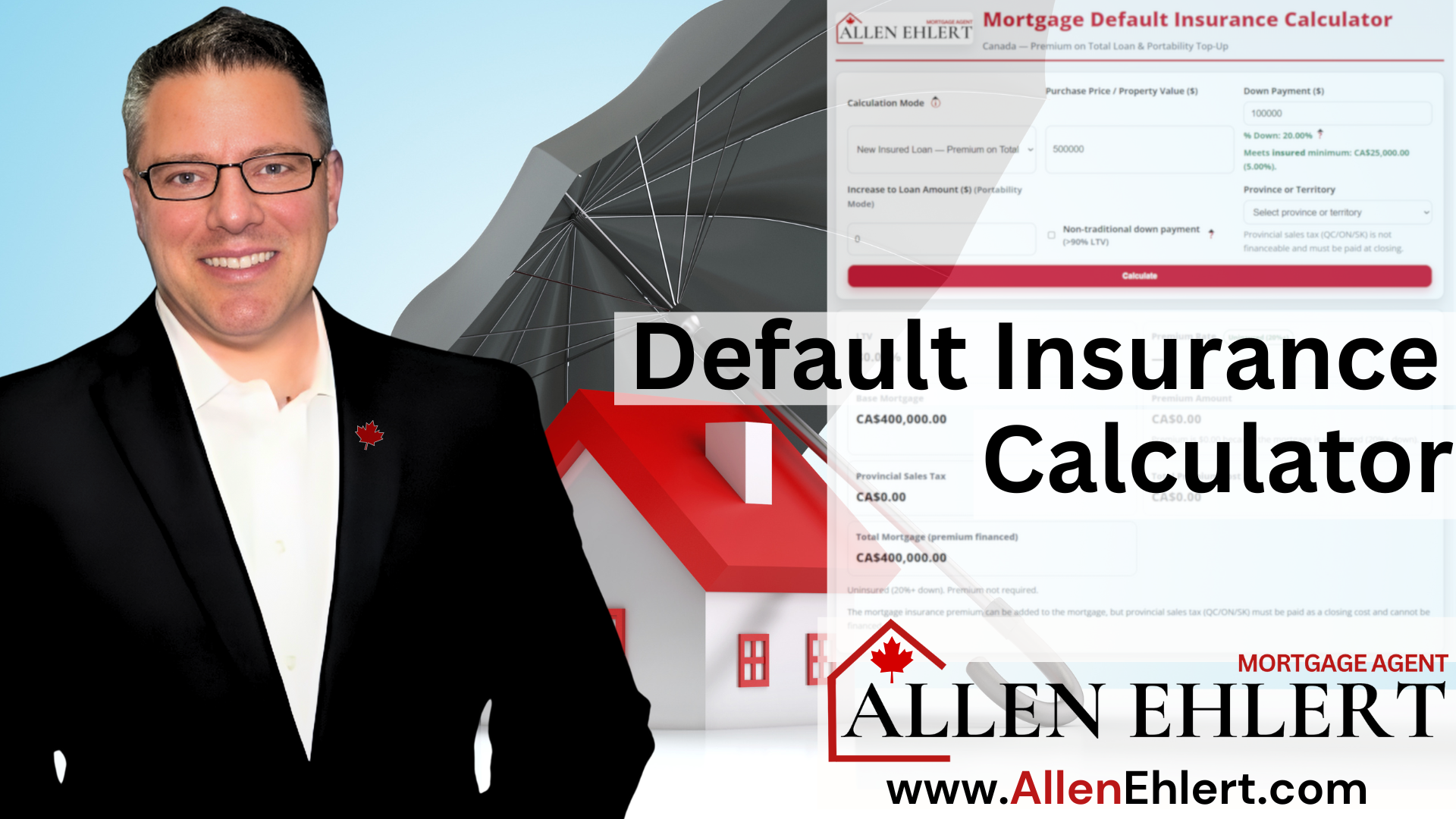

Mortgage Default Insurance Calculator

Mortgage Default Insurance Calculator: Buying a home in Canada can feel like stepping into a maze of numbers, acronyms, and fine print — but it doesn’t have to. Whether you’re a first-time buyer or a seasoned investor, understanding how default insurance works is key to knowing your real costs and options.

Canadian Closing Costs Calculator

Canadian Closing Costs Calculator: Buying a home is one of those life-changing moments that’s equal parts thrilling and nerve-wracking. Between scrolling listings, making offers, and imagining your first morning coffee in the new kitchen, it’s easy to overlook one key detail — closing costs. These aren’t the fun, HGTV-type parts of buying a home, but they’re essential.

The Networking Myth

The Networking Myth: As a mortgage agent working alongside realtors, accountants, and financial planners, I see this disconnect every day. Talented professionals doing everything “right,” yet wondering why referrals feel harder to come by. The issue isn’t effort or skill. It’s that the rules of social engagement—and therefore business growth—have changed.

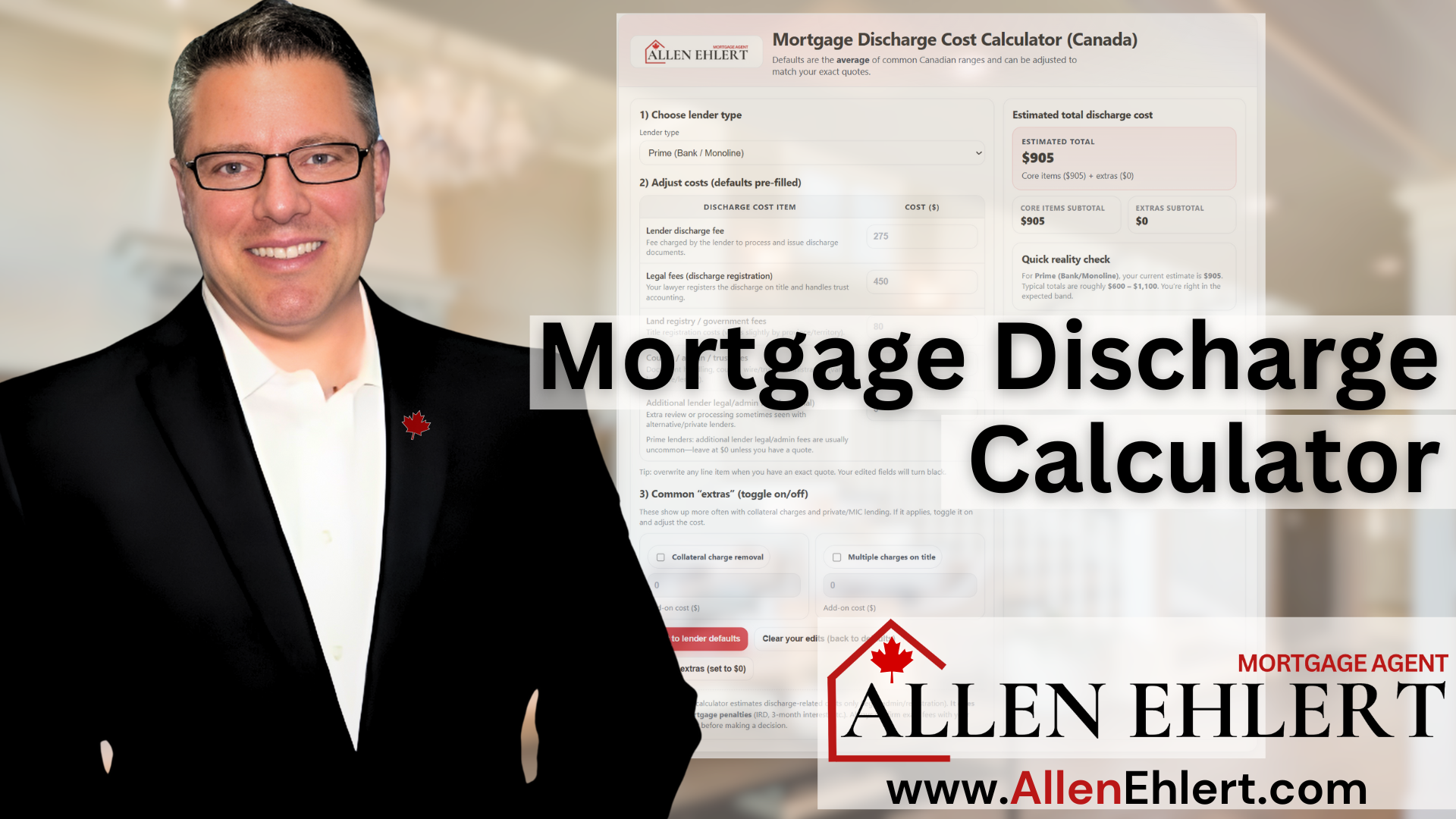

How to Use My Mortgage Discharge Cost Calculator

Mortgage Discharge Calculator: This tool is designed to help you see—clearly and early—what it actually costs to remove a mortgage from title, based on the type of lender you’re dealing with. Whether you’re refinancing, switching lenders, selling a property, or restructuring debt, knowing these numbers in advance puts you back in control.

Non Resident Tax Rebates (NRST, NRPDTT, BC PNP, etc.)

Foreign Buyer Tax Rebates (NRST, NRPDTT, BC PNP): When you first arrive in Canada, buying a home feels like crossing the finish line of a marathon—only to realize there’s another race waiting at the starting line: understanding the taxes, rebates, and programs that affect newcomers. One of the biggest hurdles foreign buyers face in Ontario is the Non-Resident Speculation Tax (NRST)—a hefty 25% charge on residential property purchases by non-residents.

Why My Pre-Approval Is Better

Pre Approval: When you’re getting ready to buy a home, that pre-approval letter feels like a badge of honour — proof that you’re serious, qualified, and ready to make your move. But here’s what most buyers (and most realtors) don’t realize: not all pre-approvals are created equal.

Why You Need a Mortgage Agent

Mortgage Agent. Buying a home isn’t just a purchase—it’s a leap into the next chapter of your life. And with rates swinging, rules tightening, and mortgage options multiplying faster than smartphone models, you deserve someone who’s dedicated to you and no one else. That’s where a mortgage agent steps in—your advocate, your strategist, your buffer against costly mistakes.

Stop Scrolling Realtor.ca

Get a Mortgage Agent first: Most people start their homebuying adventure exactly backwards. They hop onto Realtor.ca, fall in love with a gorgeous kitchen, picture their dog in the backyard, and then—usually with a little dread—they think, “Okay… how do we actually pay for this and what can we afford?”

Need a Mortgage? Start Here.

Need a Mortgage? Start Here: Buying a home—especially your first—can feel like stepping into a world where everyone else seems to have the rulebook but you. Rates, lenders, documents, jargon… it’s enough to make anyone feel like they’re drinking from a firehose. But when you follow the right steps in the right order, everything becomes clearer, calmer, and surprisingly empowering.

Protect Your Mortgage

Mortgage Protection Insurance: Buying a home, especially your first home is one of those big, life-defining moments. You and your partner have been budgeting, working with your mortgage agent, hunting down listings, talking to realtors, and imagining what that first night in a place that’s finally yours will feel like. But beneath all the excitement, there’s a quieter, more grown-up question that every couple needs to ask—“If something unexpected happens, can we not lose this home we worked so hard for?”

Understanding Contributory Income

Contributory Income: Every once in a while, a mortgage file comes along that makes you smile—not because it’s easy, but because you know exactly what lever to pull to make the deal work. Contributory income is one of those levers. It’s the quiet, seldom-talked-about income source that can turn a “maybe” into a confident “yes,” especially when buyers are stretched, ratios are tight, or affordability feels like a moving target. And if you’re a realtor guiding clients or a borrower trying to qualify, understanding how contributory income works is like unlocking a hidden chapter in the rulebook.

Understanding Shelter Costs

Shelter Costs: If you’ve ever felt like lenders were speaking a different language when they talk about “shelter costs,” you’re not alone. Clients often look at me like I’m explaining astrophysics when I break down why lenders assign a shelter cost—even when a borrower is living in their parents’ basement and paying nothing more than a smile and a promise to take out the garbage.

10 Ways Urbanization Impacts Real Estate Prices

Urbanization trends significantly impact real estate prices due to a variety of interconnected factors: Increased Demand in Urban Areas Limited Supply in Dense Areas Changing Lifestyles and Preferences Infrastructure and Amenities Economic Opportunities Investment...

Smallest Mortgage You Can Get

Smallest Mortgage: Ever wonder how small a mortgage can actually be? Maybe you’ve nearly paid off your home and want to pull out a little equity for renovations, or you’re buying a modest rural property that doesn’t cost much. You might be surprised to learn that lenders in Canada do have minimum mortgage amounts—and they vary depending on the lender, the property, and even the province.

Transferring the Family Cottage

Transferring Cottages: Explore the essentials of transferring your family Cottage in Canada with ease. Understand tax implications, adjusted cost base, and more.

Call a Mortgage Agent FIRST!

Call a Mortgage Agent First: You’ve finally decided—it’s time to buy a home. Maybe you’ve been scrolling through Realtor.ca late at night, dreaming about that perfect place with the big backyard or a condo downtown near your favourite coffee shop. It’s exciting, no doubt. But before you call your best friend’s realtor or start booking showings, let’s hit pause.

10 Benefits of Choosing Fixed

Fixed Mortgages: Let’s face it—choosing a mortgage can feel like standing at a financial crossroads with a blindfold on. Do you gamble on a variable rate, hoping the market stays friendly, or do you lock into a fixed rate and sleep peacefully at night knowing exactly what your payment will be?

Time to Lock It In

Fixed Mortgage vs Variable Mortgage: If you’ve been sitting on the fence wondering whether to go fixed or variable with your next mortgage, you’re not alone. Every client, from first-time buyers to seasoned investors, faces that same moment of decision—do you take the guaranteed calm of a fixed rate, or do you play the market with a variable? The answer isn’t the same for everyone, but timing plays a huge role. And right now, as we reach the tail end of a rate-cutting cycle, the stars may be aligning for fixed-rate mortgages.

The History of Credit Cards

The History of Credit Cards: From Retail Tabs to Digital Wallets Credit is not new. Long before banks, apps, and plastic cards, merchants extended credit to trusted customers based on personal relationships. But the story of how that informal trust evolved into the...

Why Many Banks Provide Bad Service

Average Handling Time, Bad Bank Service, When was the last time you called your bank’s customer service line? If you’re like most Canadians, it wasn’t exactly a warm, fuzzy experience. You were probably shuffled around, put on hold, and when you finally spoke to a representative, they couldn’t wait to get you off the phone. Sound familiar? It’s not that the people answering don’t care—it’s that the system they work under is built to prioritize the bank’s bottom line, not your financial well-being.

Consumer-Directed Finance Is Almost Here

Consumer Directed Finance: Let’s be real—getting a mortgage in Canada can sometimes feel like dragging a sack of bricks uphill. Between pay stubs, NOAs, bank statements, and all the back-and-forth emails, it’s no wonder many clients feel stressed before the real house hunt even begins. But what if I told you there’s a new way coming that could cut through the red tape, give you more control, and make the whole process smoother?

Canadian Home Carrying Cost Calculators

Canadian Home Carrying Cost Calculator: You’ve found the dream home: open-concept kitchen, backyard for summer BBQs, maybe even a finished basement for movie nights. The mortgage payment looks doable. But here’s the kicker: just because you can afford the payment doesn’t mean the bank will agree.

5 Reasons AI Can’t Replace the Mortgage Agent

We live in a world where you can ask ChatGPT to write an essay, plan your meals, or even draft your wedding vows. So it’s no surprise some people wonder: “Why can’t I just use AI to get mortgage advice?”

Here’s the truth: AI can crunch numbers, give you general information, and even explain mortgage terms in plain English. But when it comes to actually securing the right mortgage—navigating lender rules, strategizing for your future, and advocating on your behalf—AI just doesn’t cut it. That’s where a professional mortgage agent like me comes in.

Ultimate Canadian Closing Costs Calculator

The Ultimate Canadian Closing Costs Calculator. This tool doesn’t just spit out a random number—it walks through all the hidden (and not-so-hidden) expenses that come with buying a home in Ontario. It accounts for the type of buyer you are, the kind of mortgage you’re getting, and every little adjustment in between.

“What’s Your Lowest Rate?”

Lowest Rate: If you’ve ever called a mortgage agent and led with the question, “What’s your lowest rate?”, you’re in good company — it’s probably the most common question in our industry. And honestly, I get it. Rates are tangible. They’re plastered all over billboards, bank websites, and radio ads.

Canada’s Ultimate Home Purchase Price Calculator

Purchase Price Affordability Calculator: Buying a home is exciting—no doubt about it. But let’s be honest: it’s also one of the biggest financial decisions you’ll ever make. The million-dollar (well, sometimes literally) question is, “How much house can I actually afford?” That’s where my Purchase Price Affordability Calculator comes into play.

Loan-to-Value’s Mortgage Impact

When you’re house hunting, refinancing, or even just thinking about tapping into your home equity, there’s one little number that keeps popping up: Loan-to-Value (LTV). It sounds technical—and it is—but once you get it, you’ll see why lenders, insurers, and even private investors obsess over it. And here’s the kicker: your LTV doesn’t just decide if you qualify, it directly impacts the rate you’ll pay.

Who’s Behind Those Appraisals?

If you’ve ever been knee-deep in a mortgage deal and heard terms tossed around like desktop appraisal, drive-by appraisal, or full appraisal, you might wonder—who exactly is doing these things? Is there some wizard behind the curtain pulling numbers out of thin air? Not quite. Behind every appraisal type is a different process, and more importantly, a different professional or tool driving the outcome.

A Mortgage is a Simple Loan

Mortgage is a simple loan: If you’ve ever said or heard someone say, “A mortgage is a mortgage,” you’re not alone. On the surface, it seems simple: you borrow money to buy a home, pay it back with interest, and that’s that. But here’s the truth — a mortgage isn’t just a loan. It’s a complex financial instrument built on layers of policy, risk analysis, and economics that would make most people’s heads spin.

10 Reasons Getting a Mortgage Is Hard

If you’ve ever applied for a mortgage and thought, “Why do they need so much paperwork?” or “Didn’t I already send that?”, you’re not alone. Mortgage underwriting — the process where lenders decide whether to approve your mortgage application — can feel like a black hole of requests, reviews, and head-scratching delays. But there’s a good reason for it.

Not an Exit Strategy

Not an Exit Strategy: If you’re considering—or already sitting in—a private mortgage, you’ve likely heard the term “exit strategy” tossed around. Maybe your mortgage agent mentioned it. Maybe your lawyer flagged it. Maybe you nodded and moved on without really knowing what it means.

Check Your Smoke and CO Detectors

You know that saying, “an ounce of prevention is worth a pound of cure”? Nowhere does that ring truer than when we’re talking about smoke and carbon monoxide detectors. These small, often-overlooked gadgets are the unsung heroes of every home. But here’s the kicker: too many homes across Canada still have outdated or improperly wired detectors, and that’s a recipe for disaster.

Marriage, Mortgage, Title, Death & Divorce

This article aims to shed light on the nuanced dynamics of property division in Ontario through multiple scenarios.

Mortgage Application: Paying Support

Learn how paying child and or spousal support impacts your mortgage application and your tax situation.

Featured Publications

Articles

- Extended Amortizations and Hypothetical Calculations

Office of the Superintendent of Financial Institutions (OSFI) - Minimum Qualifying Rate for Uninsured Mortgages

Office of the Superintendent of Financial Institutions (OSFI) - Residential Mortgage Underwriting Practices and Procedures

Office of the Superintendent of Financial Institutions (OSFI) - Guideline on Existing Consumer Mortgage Loans in Exceptional Circumstances Financial Consumer Agency of Canada

Book: “The Program”

- Part 1 – Building Your Down Payment

- Part 2 – Mortgage Payoff Strategies

- Part 3 – Building Wealth Through Real Estate

Get a free subscription to “The Mortgage Insider” containing rate updates and financial strategies!