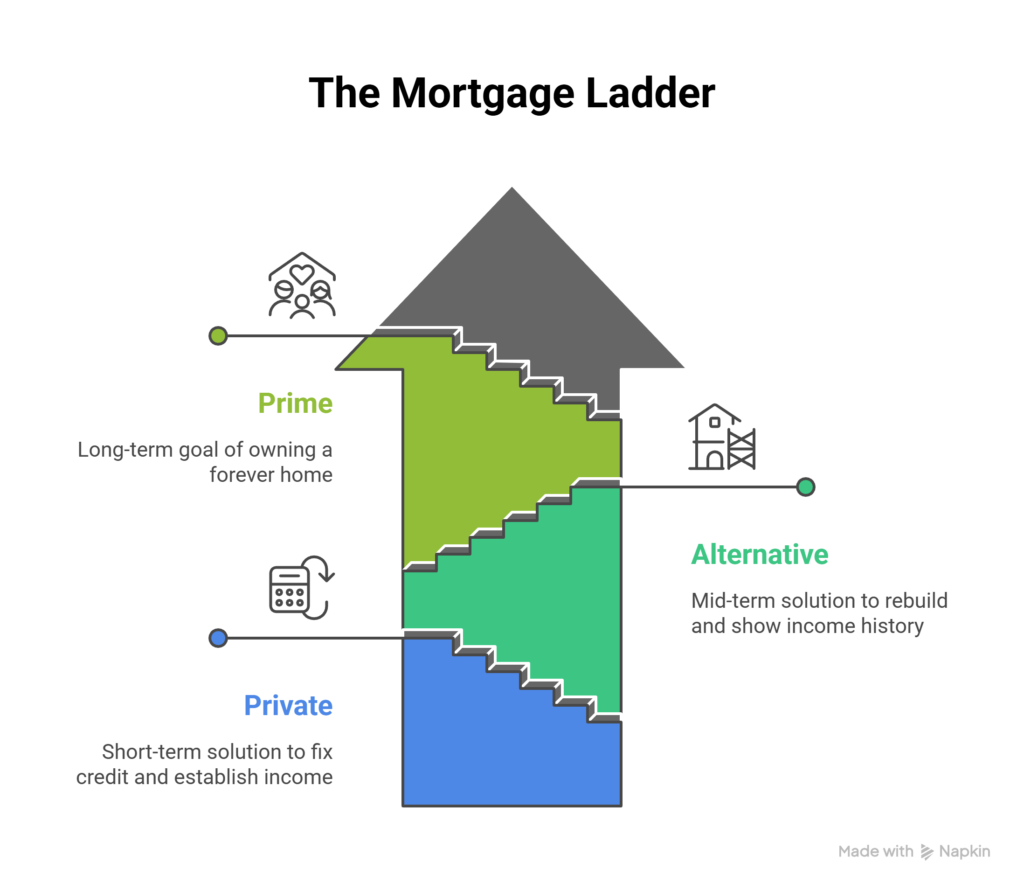

… From Private to Alternative to Prime

Life doesn’t always unfold in neat, predictable steps. Sometimes you get bruised credit after a divorce, sometimes your business income doesn’t show well on paper, and sometimes the bank just flat-out says “no.” That’s when the mortgage ladder comes into play: starting where you are, even if that’s at the bottom rung, and climbing steadily toward prime lending.

As a professional mortgage agent, my role isn’t just to place you in a mortgage. It’s to help you move up the ladder — from private, to alternative, to prime. Because the truth is, no one wants to keep paying higher rates forever. The goal is always to climb.

Here’s what I’ll cover:

The Role of Alternative (B) Lending

Private Lending: The Safety Net

How Long Should You Stay on Each Rung?

Storytime: John and Maria’s Climb

Putting This Into Practice (for Realtors & Clients)

What Is Prime Lending

When we talk about prime lending, we’re talking about the lenders who offer the very best rates and terms to clients with solid credit, documented income, and manageable debt ratios. Prime lenders aren’t just the big banks — they also include monoline lenders (mortgage-only institutions) and, in many cases, credit unions.

- Big Banks: RBC, TD, Scotiabank, BMO, CIBC, National Bank. These guys are federally regulated and must follow OSFI’s B-20 stress test, which means you have to qualify at the greater of the contract rate + 2% or 5.25% (whichever is higher). They’re safe, stable, and cheap — if you fit their box.

- Monoline Lenders: Companies like First National, MCAP, RFA, Merix, and CMLS. They don’t have branches, chequing accounts, or credit cards — just mortgages. They distribute only through brokers like me. Monolines are still prime lenders, and often they have more flexible features than the banks, like lower penalties and more competitive rates.

- Credit Unions: In Ontario, Meridian, Alterna, Libro, and FirstOntario are prime lenders too. The big difference? They’re provincially regulated, so they don’t legally have to follow B-20 for uninsured mortgages. This gives them wiggle room on qualification — for example, they might approve a deal that a federally regulated bank declines because of stress test ratios. For insured mortgages, though, credit unions still follow insurer rules (CMHC, Sagen, Canada Guaranty).

Example:

- If you’re a salaried nurse with great credit and little debt, any prime lender — bank, monoline, or credit union — will want your business.

- If you’re self-employed and just miss the B-20 stress test at a bank, a credit union may still green-light your deal.

- If you want a great rate but don’t care about having a branch, a monoline lender may give you the best option.

The Role of Alternative (B) Lending

Alternative lenders — often called B lenders — are institutions like certain trust companies (Home Trust, Community Trust, etc.), Schedule II banks (Haventree Bank, Equitable Bank, etc.) and some provincially regulated credit unions that operate with more flexibility than the banks and monolines.

They’re designed for borrowers who don’t quite fit the prime box, such as:

- Self-employed individuals whose taxable income is too low on paper.

- Recently divorced clients relying on new support payments.

- Borrowers with slightly bruised credit.

What sets them apart:

- Willingness to use stated income or bank statement programs.

- Higher tolerance for debt service ratios (often up to 50–55%).

- Ability to accept new support agreements or creative income sources.

- A more common-sense approach to underwriting, looking at the overall story.

The trade-off is that rates are 1–2% higher than prime lenders, and there is usually a one time lender fee and broker fee. But remember, this is a bridge to help you qualify today while working toward a return to prime lending and lower rates tomorrow.

Example: You’re a contractor who reports $40K taxable income after deductions, but your true cash flow is closer to $90K. A bank or monoline says “no,” but an alternative lender can approve you based on a stated income program. For many self-employed people, it is cheaper to go with the higher mortgage rate than to hand over 50% of their income to the CRA in taxes. In this example, the bank says your income is $40k, so you don’t qualify for much. But an alternative lender accepts your income as $90k, so you qualify for a lot more. And there often is no stress test with an alternate lender, so you qualify for even more still.

Private Lending: The Safety Net

Private lenders such as mortgage investment corporations (MICs) — are the safety net at the bottom of the ladder. They’re asset-based lenders who care more about your equity than your income or credit. Consider them the ‘lender of last resort’.

The terms are short (usually 1 year but often 6 months or less), rates are higher (7–12%+), and lender and broker fees apply. But they’re invaluable when you need a fast, flexible solution. I know some private lenders that can lend in just a few hours. The key here is having a clear exit strategy — private lending is never meant to be long-term.

Example: You’re separating from your spouse and need to buy them out, but you have no income history of spousal support yet. A private lender will get the deal done today, and once the support payments are seasoned, we climb you back up to alternative or prime.

How Long Should You Stay on Each Rung?

- Private: Ideally 12 months or less. Just enough time to fix credit, establish income, or finalize your separation.

- Alternative: Usually 1–3 years. Enough time to rebuild, file stronger tax returns, or show a longer income history. However, in some cases, you may choose to stay in Alternative.

- Prime: This is the end goal — your forever home for lending. Once you’re here, you want to stay as long as possible.

Storytime: John and Maria’s Climb

John and Maria ran a small catering business. During COVID, their credit took a hit, and they fell behind on taxes. When they separated, Maria wanted to keep the house but couldn’t qualify at a bank.

Step one: we placed her with a private lender for 12 months, which gave her time to clean up the debts and show spousal support payments on record.

Step two: after a year, we refinanced into an alternative lender, who accepted her stated income.

Step three: two years later, her financials looked strong enough to move back to a prime lender at a rock-bottom rate.

She climbed the ladder — and kept her home.

Putting This Into Practice (for Realtors & Clients)

- For Realtors: Don’t assume a buyer is dead in the water because a bank declined them. If you know their story, I can often place them with an alternative or private lender, helping them buy today while working toward prime tomorrow.

- For Clients: If you’ve been told “no,” remember — it just means “not yet.” With the right strategy, we can use a step-by-step approach to move you up the ladder.

Allen’s Final Thoughts

Mortgages aren’t a one-shot deal — they’re a journey. Sometimes that journey starts on the bottom rung of the ladder, with a private lender. Sometimes you’re midway on the alternative step. And sometimes you’re lucky enough to jump right to prime.

Wherever you start, my job as your mortgage agent is to help you climb. I’ll map out the exit strategy, set the timeline, and guide you step by step until you reach the prime rates and terms you deserve.

If you’re a client worried about where you stand — or a realtor with buyers who’ve hit a wall with the banks — let’s talk. Together, we’ll find the right rung, and we’ll start climbing.