Securing a mortgage in Canada has long been an income-driven process. Lenders scrutinize pay stubs, tax returns, and employment history to determine whether a borrower qualifies. However, in today’s evolving financial landscape, assets play an increasingly significant role in strengthening a mortgage application.

For some, assets act as a compensating factor—bridging the gap where income alone might fall short. For others, particularly high-net-worth borrowers, assets can sometimes outweigh traditional debt service requirements, allowing for more flexible lending solutions. Understanding how different types of assets are assessed and leveraged in mortgage applications is critical for maximizing borrowing potential.

Understanding the Role of Assets in Mortgage Qualification

Do Assets Serve as Collateral for a Mortgage?

Types of Assets Considered in a Mortgage Application

The Impact of Assets on Mortgage Affordability and Loan Size

The Role of Net Worth in Mortgage Applications

Alternative Lenders and Asset-Based Mortgage Approval

Using Assets to Offset a High Debt Service Ratio

Asset Verification: Documentation Requirements for Mortgage Applications

Can Assets Be Used for a Down Payment?

Pledged Assets and Secured Mortgage Financing

Future Trends: Will Canadian Lenders Rely More on Assets ?

Understanding the Role of Assets in Mortgage Qualification

Mortgage lenders are primarily concerned with one thing: risk mitigation. Borrowers with substantial assets demonstrate a greater ability to withstand financial hardships, making them lower-risk clients.

Lenders distinguish between liquid and non-liquid assets when evaluating a mortgage application. Liquid assets, such as cash and investments, are preferred because they can be quickly accessed in case of payment difficulties. Non-liquid assets, such as real estate and business ownership, may strengthen a financial profile but cannot easily be converted to cash.

For mortgage providers, assets serve multiple purposes:

- Acting as a financial buffer in case of job loss or economic downturns

- Compensating for lower or fluctuating income streams

- Providing security for higher loan amounts

Do Assets Serve as Collateral for a Mortgage?

A traditional mortgage is a secured loan, meaning the property itself serves as collateral. If a borrower defaults, the lender has the legal right to foreclose and sell the home to recoup losses.

However, assets can be pledged as additional collateral in certain mortgage structures, particularly with:

- High-Net-Worth Mortgage Programs

- Investment-Based Lending (Leveraging Stocks & Bonds)

- Private Lenders Using Alternative Security Measures

In cases where an applicant lacks sufficient employment income, lenders may allow borrowers to pledge financial assets to enhance loan security. This is especially common among:

- Self-employed individuals with irregular cash flow

- Retirees with investment-heavy portfolios

- Real estate investors leveraging equity from other properties

Lenders do not typically seize additional assets unless explicitly agreed upon in a pledged asset mortgage.

Types of Assets Considered in a Mortgage Application

Lenders categorize assets into two primary groups: liquid and non-liquid. Each type plays a different role in reinforcing a borrower’s financial profile.

Liquid Assets: The Gold Standard in Mortgage Applications

Lenders prioritize liquid assets because they are readily accessible and can be used to cover mortgage payments in case of financial difficulties.

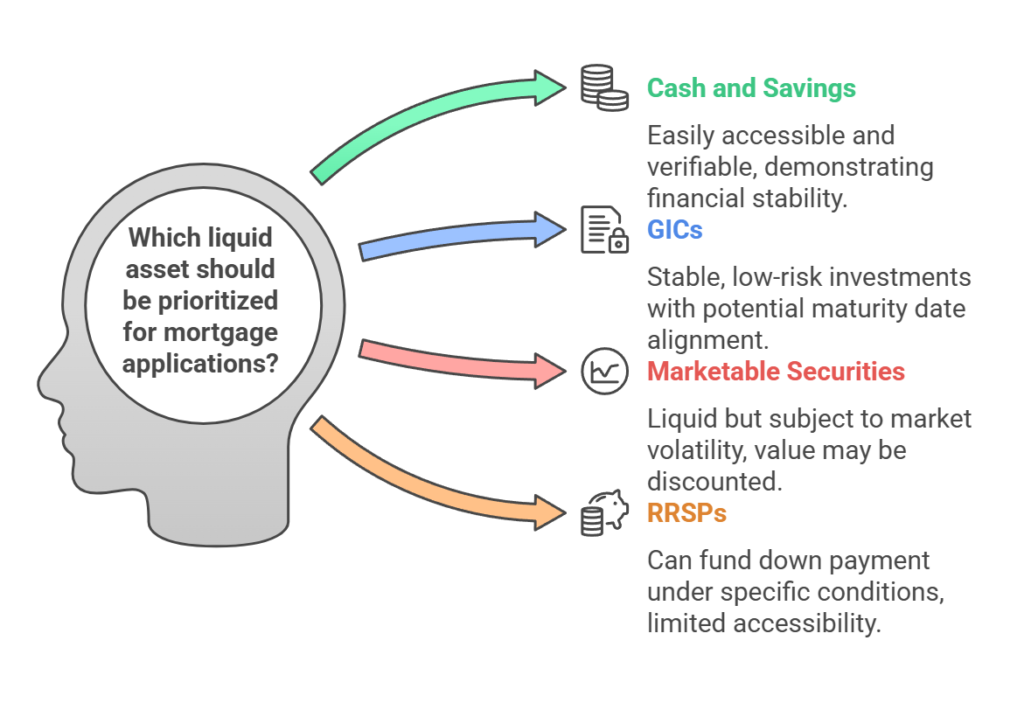

Cash and Savings Accounts

- Easily verifiable and immediately accessible funds

- Demonstrates financial prudence and stability

- Often required to show proof of down payment (must be in the account for at least 90 days)

Guaranteed Investment Certificates (GICs)

- Highly stable, low-risk investments

- Can be used as additional reserves for mortgage security

- If non-redeemable, lenders may require a maturity date that aligns with mortgage terms

Marketable Securities (Stocks, Bonds, ETFs, Mutual Funds)

- Valued for their liquidity, but subject to market volatility

- Lenders may discount their value due to fluctuating market conditions

Registered Retirement Savings Plans (RRSPs)

- Can be used under the Home Buyers’ Plan (HBP) to fund a down payment

- Limited in accessibility unless withdrawn under specific conditions

- Some lenders count a portion of RRSP holdings as financial strength

Non-Liquid Assets: Strengthening a Borrower’s Profile

While non-liquid assets are not immediately accessible, they can reinforce an applicant’s overall financial strength.

Real Estate Holdings

- Increases net worth and financial credibility

- Can be leveraged through home equity loans or secured lines of credit

- Lenders favor borrowers who own multiple properties with low outstanding mortgage balances (blanket mortgages are available with alternative and private lenders)

Business Equity and Ownership

- Important for self-employed applicants, but challenging to value

- Lenders may consider business financial statements to determine worth

- Borrowers may need a shareholder agreement and tax returns as proof of ownership

Vehicles, Collectibles, and Precious Metals

Generally not accepted unless they are pledged as secured assets. High-value collectibles (art, classic cars) require formal appraisals. Precious metals (gold, silver) may be used in alternative lending scenarios

Life Insurance with Cash Surrender Value

Some lenders accept life insurance cash value as an asset. Can be borrowed against for down payments or closing costs. Not all lenders recognize life insurance as a liquid asset

The Impact of Assets on Mortgage Affordability and Loan Size

The presence of substantial assets can enhance mortgage eligibility in several ways:

- Increase borrowing power – Lenders may approve a larger mortgage amount if the borrower has strong asset reserves.

- Offset lower income – If income is modest but assets are significant, some lenders allow exceptions to traditional debt service ratios.

- Improve mortgage terms – High-net-worth borrowers may qualify for better interest rates and reduced down payment requirements.

Borrowers with strong assets but lower income verification may benefit from net worth mortgage programs.

The Role of Net Worth in Mortgage Applications

For high-net-worth individuals, lenders may prioritize assets over income when assessing mortgage applications.

What Qualifies as High Net Worth?

- $150,000+ in liquid assets (varies by lender)

- Real estate holdings with significant equity

- Investment portfolios with stable long-term value

Net Worth Mortgage Programs

- Designed for borrowers with significant assets but lower income

- Offered by private banks, alternative lenders, and wealth management institutions

- Typically have higher down payment requirements but lower income documentation needs

Alternative Lenders and Asset-Based Mortgage Approval

For borrowers struggling with traditional income requirements, B-lenders and private lenders offer more flexible asset-based approvals.

B-Lenders – Accept more diverse income and asset sources, including investment accounts, rental properties, and business equity.

Private Lenders – May approve a mortgage based solely on net worth rather than income verification.

These lenders cater to:

- Self-employed individuals with fluctuating income

- Retirees with large investment portfolios but limited active income

- Newcomers to Canada with significant overseas assets

Using Assets to Offset a High Debt Service Ratio

Lenders calculate debt service ratios to determine affordability. Borrowers with high debt levels may struggle to qualify—unless they have substantial assets.

Gross Debt Service (GDS) and Total Debt Service (TDS) Ratios

- GDS: Mortgage-related expenses should not exceed 39% of income

- TDS: Total debts should not exceed 44% of income

Some lenders adjust these limits for borrowers with high net worth. Assets can serve as a mitigating factor, allowing more flexibility in ratio calculations.

Asset Verification: Documentation Requirements for Mortgage Applications

Lenders require proof of assets to consider them in mortgage approvals. Standard documentation includes:

- Bank Statements (90 Days Minimum) – Verifying liquid assets

- Investment Account Summaries – Confirming marketable securities and GICs

- Property Valuation Reports – Establishing real estate equity

- Business Financials – For self-employed applicants leveraging company assets

Can Assets Be Used for a Down Payment?

Yes, but lenders impose strict requirements on down payment funds:

- Must be in the borrower’s possession for at least 90 days

- Lenders require proof of origin for large deposits

- Borrowed down payments must be secured by another asset

Some borrowers use:

- Investment withdrawals (stocks, mutual funds, RRSP Home Buyers’ Plan)

- Selling tangible assets (cars, jewelry, etc.)

Pledged Assets and Secured Mortgage Financing

A pledged asset mortgage allows borrowers to use investments or other assets as security instead of liquidating them.

- Investment Portfolios as Collateral – Borrowers can pledge stocks, bonds, or GICs to secure better mortgage terms.

- Margin Loans Against Securities – High-net-worth borrowers may use leveraged investment loans instead of selling assets.

This strategy is most common among:

- Wealthy investors seeking tax efficiency

- Business owners avoiding cash flow disruption

Future Trends: Will Canadian Lenders Rely More on Assets for Mortgage Approvals?

The Canadian mortgage landscape is evolving, with a growing emphasis on net worth over traditional income metrics.

- Private banks and alternative lenders increasingly cater to asset-rich borrowers.

- More lenders are integrating “wealth-based” mortgage underwriting models.

- Self-employed and non-traditional income earners are benefiting from asset-based lending solutions.

Summary

While income remains the cornerstone of mortgage approvals in Canada, assets play an equally critical role in strengthening a borrower’s profile. From cash reserves to investment portfolios, well-documented assets can enhance loan eligibility, improve mortgage terms, and compensate for lower or variable income.

Key takeaways:

- Lenders prefer liquid assets but recognize non-liquid holdings in net worth calculations.

- High-net-worth mortgage programs offer more flexibility for asset-rich applicants.

- Alternative lenders are becoming more accommodating of asset-based approvals.

For borrowers aiming to maximize mortgage qualification, strategically leveraging assets can be the key to securing better terms and higher borrowing power.